SNB: Steady Policy With Concern on Strong CHF

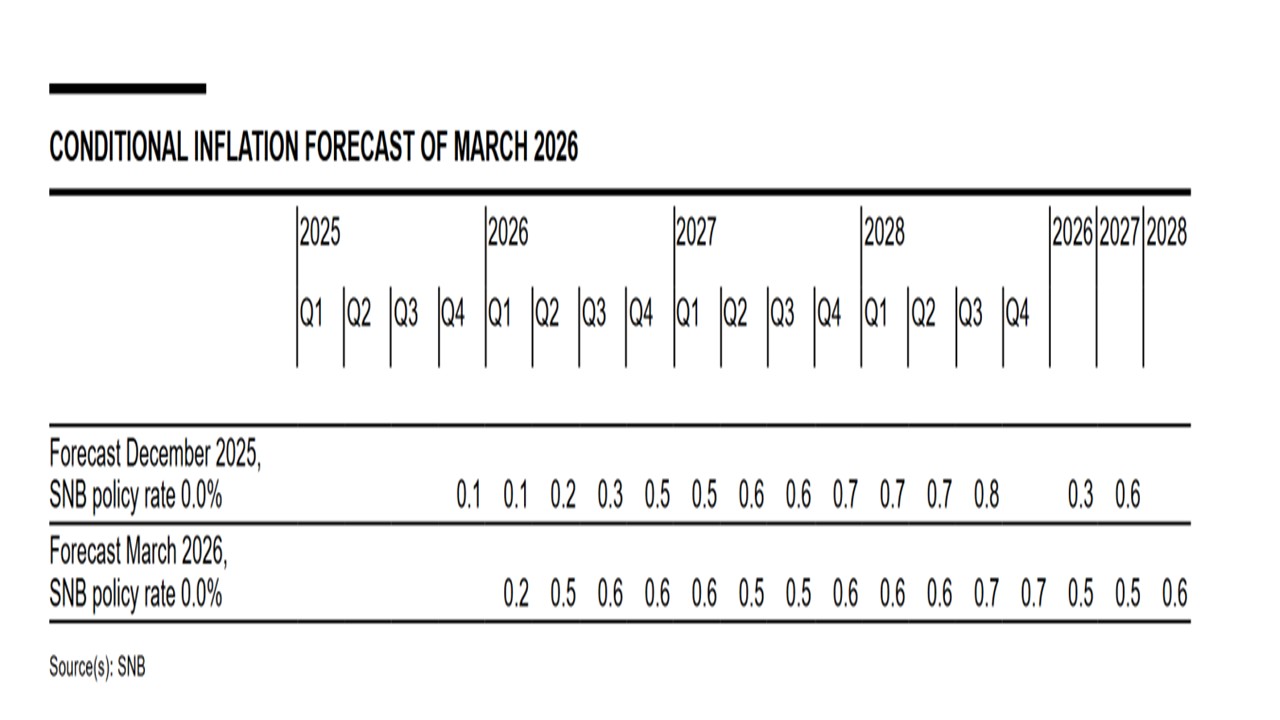

· The SNB maintained the policy rate at zero, with a 0.2% increase in 2026 CPI due to the Iran war but 2027 0.1% lower at 0.5% due to CHF strength since the December meeting (Figure 1). The emphasis in the statement on guarding against the disinflationary risk from more CHF strength suggests that the easing bias remains in place, as a tool against more substantive CHF strength. However, the bar to actually cut rates is higher given the uncertainty over the Iran war and we forecast no change in policy rates in the remainder of 2026.

Figure 1: SNB CPI Inflation Projections

Source: SNB

Key points to note from the SNB

· Domestic disinflation before oil price impact. Before the Iran war Swiss CPI had been very weak. Moreover, the near zero CPI inflation rate is as much a result of weak domestic price pressures, which are slightly negative in smoothed and adjusted m/m measures. The Iran war initial effects have prompted the SNB to increase 2026 CPI by 0.2% but still only to 0.5%, but 2027 CPI inflation is 0.1% (Figure 1) lower at 0.5% due to CHF strength since the December meeting. Though 2026 CPI could be boosted further at the June meeting, this will likely only be modest and the SNB appears equally concerned about disinflation from CHF strength. The SNB statement was clear that the Iran war boost to the CHF could increase the odds of FX intervention. On growth, the SNB are in wait and see mood, with the gloomy 2026 projected GDP growth remaining at 1% (low for a world cup year), but 2027 at 1.5%.

· CHF. The increasing strength in the CHF is causing reverberations, with the nominal trade weighted Franc hitting new highs. However, we would argue that with the strong currency also reducing import and producer prices. A real or inflation-adjusted effective exchange rate shows a far less sizeable appreciation when deflated by producer prices rather than those for the consumer. However, the SNB are concerned enough that FX intervention is a real risk, but would they cut the policy rate?

· Easing bias but high hurdle. A cut into negative territory is possible, but would require a further rapid and large CHF appreciation that would likely persist. Otherwise CHF spikes are best dealt with via FX intervention. The Iran war on balance makes it less likely that the SNB cuts and the hurdle to a cut is high. However, market expectations of a 25bps hike at the December 2026 SNB meeting look to be overdone. This is prompted by expectations that the ECB will hike twice by this period, but we would suspect that even if the ECB hiked in 2026 that the SNB will not follow due to low 2027 and 2028 inflation forecasts. Our own view remains that the ECB will not hike and will actually cut by 25bps, due to tighter financial conditions that the ECB policy rate indicates.