UK CPI Preview (Jun 18): Services Inflation to Fall Clearly?

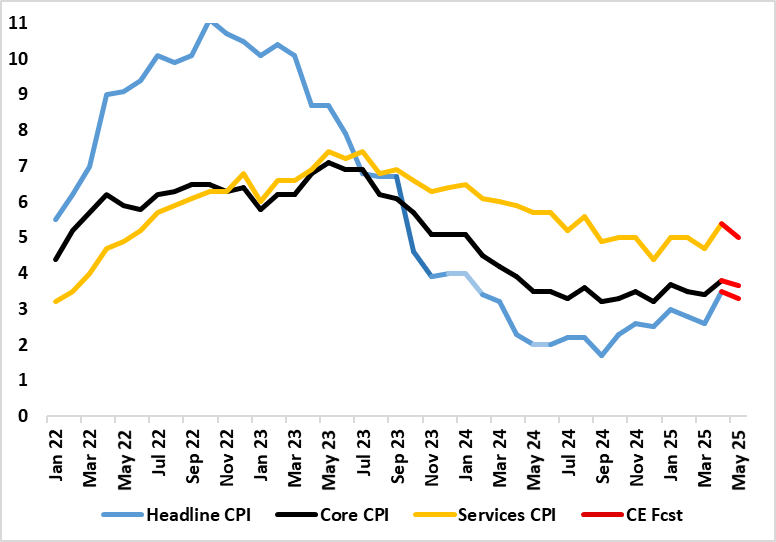

The UK and the rest of the DM world have been decoupling, at least in terms of inflation, where the UK has undergone a surge, (largely home-grown) just as W European sees their respective inflation fall back to, if not below. Regardless, as for the UK, the main near-term inflation story was (and remains) what would happen in the April data when a series of energy, utility, post office and some other regulated and service price rises are due, albeit now offset somewhat by a fall in petrol prices if the slump in energy prices persists. The result was a notch higher than the BoE expected with a jump to 3.5%, albeit since revised back a notch to 3.4%, still a rise dominated by a pick-up in services, some of which (ie airfares) may be temporary. Indeed, the timing of Easter may have been a partial factor and this should unwind in the looming May CPI. But while we see a distinct drop back in services, the headline and core rates may drop a mere 0.1 ppt, albeit a notch below BoE thinking.

Figure 1: April CPI Inflation Jumped Broadly – Albeit Temporarily?

Source: ONS, Continuum Economics

The April data may have persuaded some of the MPC not to cut last month had they been aware of the full data. But at the same time there was no clear fresh inflation spiral with six of the 12 CPI components seeing softer pressures and where consumer sensitive clothing and household equipment actually turned negative, possible a sign of reined in pricing power.

We see inflation having peaking at this April level albeit with some dip before the rate returns (briefly) to (around) 3.5% in September, this latter outcome some 0.2 ppt below BoE thinking. As for BoE rate cutting, we think upside surprises would have to dislodge the MPC from cutting at least twice more this year albeit it clear that the MPC will remain divided, if not more so, even against a backdrop where there is a general view that policy restriction needs to reduced, the difference being over how fast given worries about price persistence (see below).

As for recent trends, the April numbers were dominated by services. Airfare prices rose by 27.5% on the month, up from 6.5% a year ago. This was the second-highest monthly rise for an April since records began and very much reflects the timing of Easter which should mean airfares drop back in May. The rise in the headline rate reflected large upward effects from gas and electricity, which resulted from the raising of the Office of Gas and Electricity Markets energy price cap in April 2025. Prices of water and sewerage rose by 26.1% in the month to April 2025 compared with a rise of 8.1% a year ago. This is the largest rise since at least February 1988.

But there was a further downward contributions came from clothing fuels, household goods and restaurants and hotels, the latter often seen as a lead indicator for services inflation.

Notably, the high-profile added price pressures that hit the headline are hardly demand determined even though largely of domestic origin and may accentuate already weak growth, thereby further restraining company pricing power, but where the BoE will now be (or should be) shifting its concerns from alleged price persistence to assessing and minimising downside activity risks from the tariff (both direct and indirect).

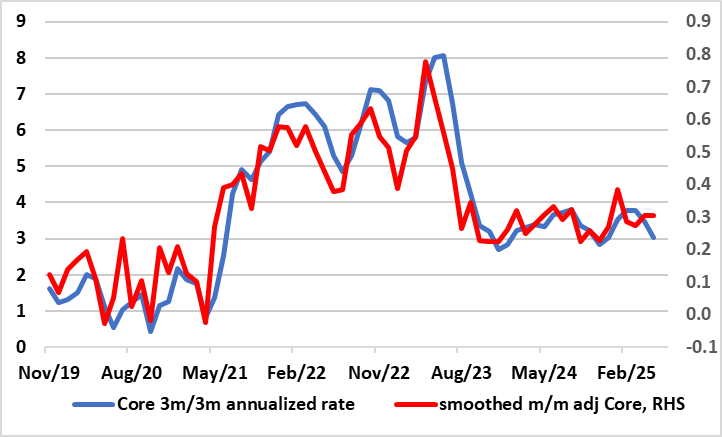

Figure 2: Clear Adjusted Core Inflation Drop Continues?

Source: ONS, Continuum Economics

One reason for this still optimistic outlook is an alternative and more reassuring assessment of the labor market and cost pressures. To suggest that the UK labor market is merely getting less tight misses the point entirely. Amid continued reservations about the accuracy of official labor market data produced by the ONS, alternative and very clearly more authoritative data on payrolls suggest that employment is continuing to contract and seemingly somewhat more significantly so. In addition, even with the April CPI surge, adjusted m/m data show a softer core picture (Figure 2).