Third Straight Cut: CBRT Reduced the Key Rate to 42.5%

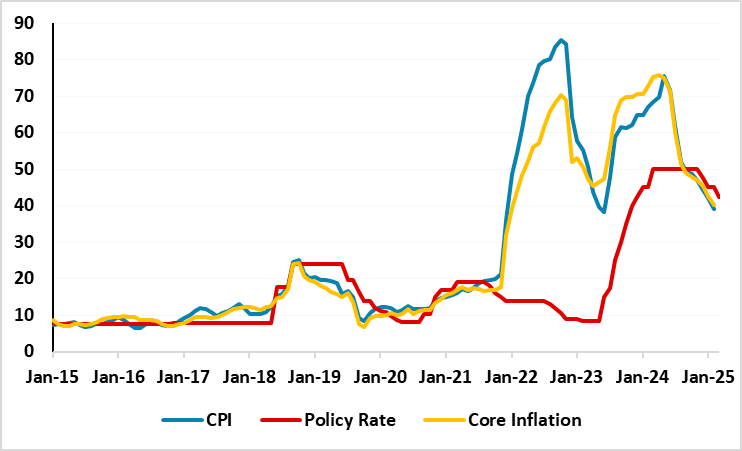

Bottom Line: After inflation softened more-than-expectations to 39.1% in February, the lowest in 20 months, the easing cycle continued on March 6 as Central Bank of Turkiye (CBRT) reduced the policy rate by 250 bps to 42.5%. The decision was supported by domestic demand remaining at disinflationary levels, and a relatively stable TRY. CBRT highlighted in its written statement on March 6 that core goods inflation remained relatively low, while services inflation slowed down (in February) after the idiosyncratic increase in January, and added that domestic demand also remained at disinflationary levels although it was above projections in Q4. Our end-year key rate prediction remains at 30.0% for 2025.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2018 – March 2025

Source: Continuum Economics

After the deceleration trend in inflation continued in February with 39.1% y/y exceeding expectations, supported by moderate slowdown in domestic demand and relative TRY stability, CBRT reduced the policy rate by 250 bps to 42.5% from 45% on March 6, which was the third rate cut in a row.

Despite MoM inflation rose by 2.27% in February, it was considerably below 5.03% MoM inflation the previous month leaving the door open for the rate cut. Annual core inflation also fell to a 37-month low of 40.2% in February, and PPI stood at 2.1% MoM demonstrating a drop to 25.2% on same month of the previous year basis.

CBRT highlighted in its written statement on March 6 that core goods inflation remained relatively low, while services inflation slowed down (in February) after the idiosyncratic increase in January, and added that domestic demand also remained at disinflationary levels although it was above projections in Q4.

CBRT emphasized that the tight monetary stance will be maintained until price stability is achieved via a sustained decline in inflation, and MPC will make its decisions prudently on a meeting-by-meeting basis with a focus on the inflation outlook.

Speaking about the course of inflation, CBRT governor Karahan said in February that backward-indexed prices such as education and rent continue to be pressure points for the inflation outlook, as they are remaining outside the influence of monetary policy. As CBRT raised the year-end inflation forecast to 24% from 21%, we continue to envisage upside risks emanating from the stickiness of services inflation, inflation expectations, deteriorated pricing behavior, and adverse geopolitical impacts will likely lead average inflation to stand at 31.9% and 20% in 2025 and 2026, respectively. A faster pace of TRY depreciation is also likely the rest of 2025 particularly given the high uncertainty governing global trade policies, which can moderately reignite inflation.

Our end-year key rate prediction remains at 30.0% for 2025, and we feel Mth/Mth inflation readings will continue to be the key as CBRT will want to avoid reigniting inflation with too aggressive rate normalization. As noted, we feel CBRT will have to proceed carefully on interest-rate adjustments given inflation expectations, pricing behavior and unpredictable outlook for the global economy continue to pose risks to the disinflation process.