Japan Outlook: A Perfect Window

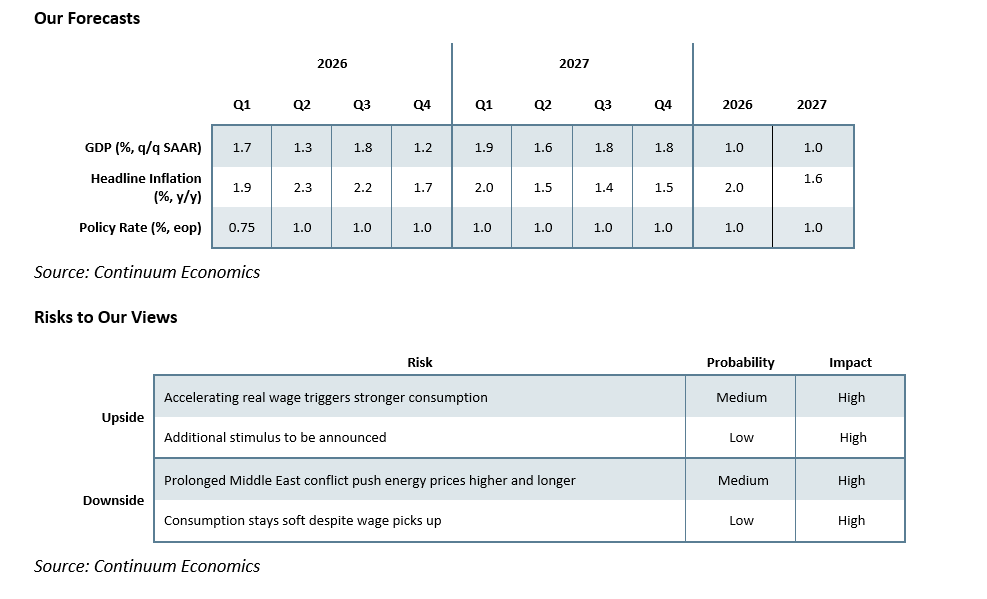

• Private consumption is supported by real wage turning positive in 2026. The trend is solidified by early spring wage negotiation results, which major firms agree to hike stronger than 2025 levels. We revised 2026/27 GDP to +1% as wage gains likely to accelerate. We expect 2026 CPI to be slightly higher at 2% due to oil volatility with the Iran war, before treading lower to 1.6% in 2027 – our baseline is a 4-6 week war, with energy prices coming back down over 3-4 quarters.

• PM Takaichi’s JPY 21.3 trillion stimulus is in full execution. Energy rebates introduced in Q1 2026 are providing a necessary buffer against record gasoline prices. The 10-year strategic fund for shipbuilding, AI & chips is also active. This industrial support underpins our 2026/27 growth forecast of 1.0%.

• The BoJ kept the 0.75% rate unchanged in March. With the inflationary backdrop supporting a hike in H1 2026, the BoJ is patiently waiting for clarity in Middle East and final result of wage negotiation to assess their pace. Our central forecast sees the BoJ to hike rates by 25bps to 1% in the April meeting as they believe the sustainable inflation target will be reached. However, we then see the BOJ pausing, both as QT causes JGB yields to spike further and as 2027 inflation turns out to be lower than BOJ estimates.

Forecast changes: 2026 CPI forecast has been revised higher to 2% from +1.9% on geopolitical driven high energy prices, as government energy subsides temper the impact from higher raw material prices.

Macroeconomic and Policy Dynamics

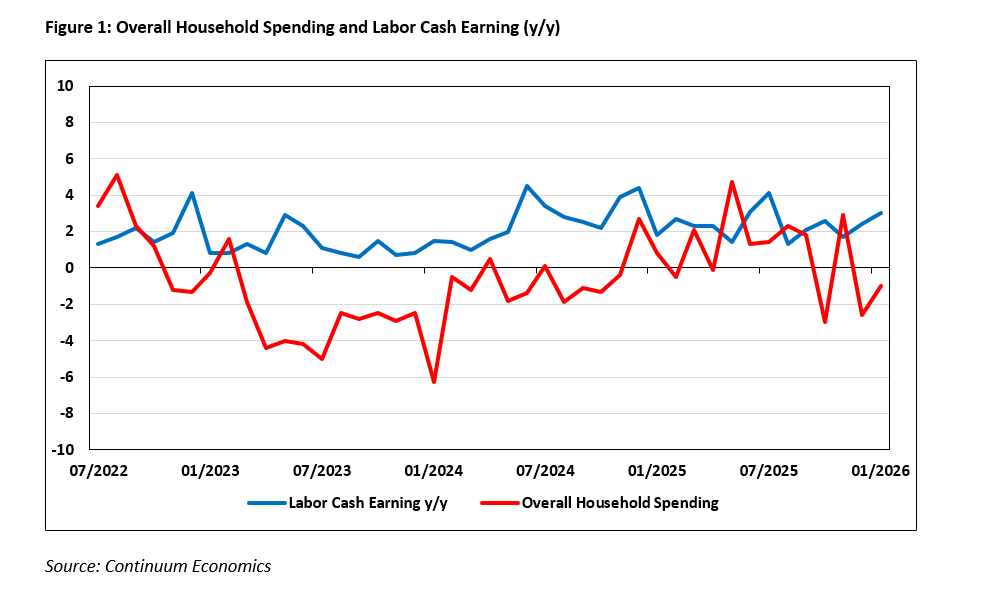

Private consumption growth steadies as real wages turned positive since the beginning of 2026, ending the prolonged choppy period. After the initial shock of U.S. trade tariffs fades, the early Shunto (spring wage) negotiations are yielding positive result. This momentum confirms that the cycle of higher business price/wage setting is resilient, providing the necessary floor for steady consumer behavior throughout 2026.

PM Takaichi’s JPY 21.3 trillion stimulus is fully in motion. One-time measures, including the energy subsidies (JPY 7,000/household) and rice coupons, are currently active in Q1 2026. The measures have been extended throughout Q2 to offset the living cost pressure from high global oil prices. The 10-year strategic fund for A.I. and chips has also been officially integrated into the FY2026 budget, reinforcing Japan’s long-term industrial competitiveness and hoping to attract more business investment. Takaichi's fiscal policy remains pro-spending but so far seems disciplined. Our projection of a 0.9% increase in government spending for 2026 sees Takaichi balancing strategic investment & cost relief with the need to secure market confidence.

The trade balance remains under pressure from U.S. tariffs but the diversification strategy is yielding results. The stable growth in exports to Asia and the EU since late 2025 is helping to cushion the manufacturing sector. While the weak JPY keeps Japanese exports attractive, we expect net exports to moderate in 2026/27 as strengthening domestic demand and higher energy costs drive imports higher. The soft JPY maybe here to stay a bit longer unless we see strong commitment from the BoJ or USD haven bids fade on geopolitical tension easing.

Our forecast for 2026/27 GDP is revised to +1.0% as wage/price setting and consumption behavior are firmly in motion with private consumption the cornerstone. The "Takaichi stimulus" has been partially neutralized by high energy prices and will be contributing less towards previously anticipated economic growth. The 2026 preliminary "Shunto" results have passed even the most optimistic expectation. Major firms (including Nissan and Mitsubishi Motors) have fully accepted union demands, with average hikes landing between 5.5% and 5.9%. In the BoJ’s eyes, these consecutive years of 5%+ hikes confirms that the structural change in wage-setting is now a permanent feature of the Japanese macro-landscape, anchoring inflation sustainably toward the 2% target. With average household spending in 2025 at +1.5% y/y, we are forecasting solid consumption growth in 2026 when real wage accelerates.

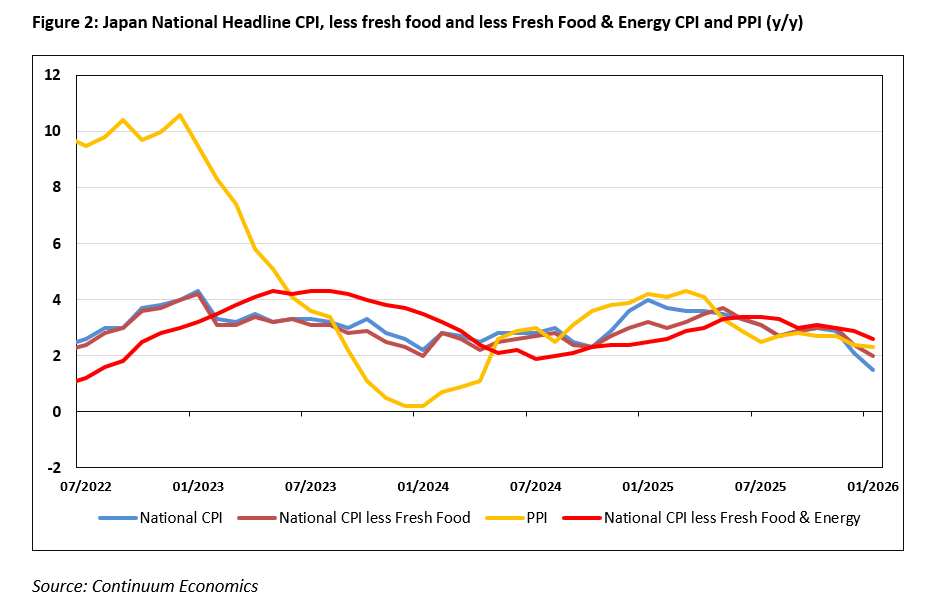

Although rice prices have mostly stabilized due to the 2025 harvest, the less fresh food & energy CPI has remain a tough nut to crack. We have further revised 2026 CPI to 2% to account for the recent energy price volatility driven by Middle East tensions. For 2027, our central forecast is 1.6% to address the fade out of cost-push element and demand-pull inflation takes over.

Policy Outlook

The BoJ’s rhetoric remain committed to further tightening if the 2% sustainable inflation outlook holds. Following the March 19 hold at 0.75%, we still anticipate a 25bps hike to 1% in April. The Middle East conflict may give BoJ second though yet the current adverse GDP impact is not sufficient to stall their hike. While PM Takaichi’s pro-spending stance creates political obstacle, the strong wage growth gives the BoJ enough cover to ignore political headwinds for one hike. However, moving beyond 1% remains outside our central scenario, as SMEs still struggle to pass on the full weight of higher borrowing costs and 2027 inflation will likely come in below BOJ forecasts.

10-year yields have been on a "one-way traffic" since PM Takaichi took office, recently testing 2.24%. Fiscal concerns regarding the JPY 21.3 trillion stimulus is the primary driver alongside QT at close to 6% of GDP. We maintain that the BoJ will allow yields to grind higher but view 2.5% as the "line in the sand”. If yields jump too fast toward this level, we expect the BoJ to deploy emergency bond-buying operations to intervene and also scale down QT by stopping the reduction in monthly bond buying or actual increasing.

We maintain our forecast for no change in the BoJ policy rate in 2027. Once the 1% terminal rate is reached in April 2026, the BoJ will likely enter a prolonged "hawkish hold" to allow the economy to digest the higher interest rate environment, to balance between domestic demand and QT.