Preview: Due April 9 - U.S. January Personal Income and Spending - Core PCE Prices to outperform CPI

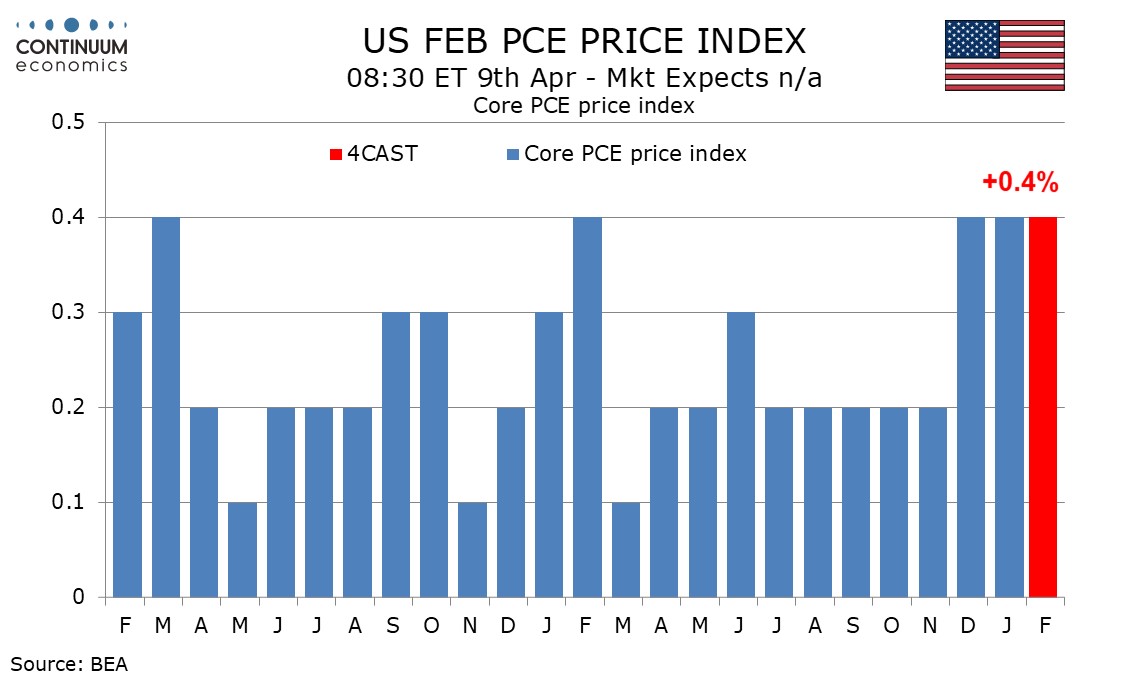

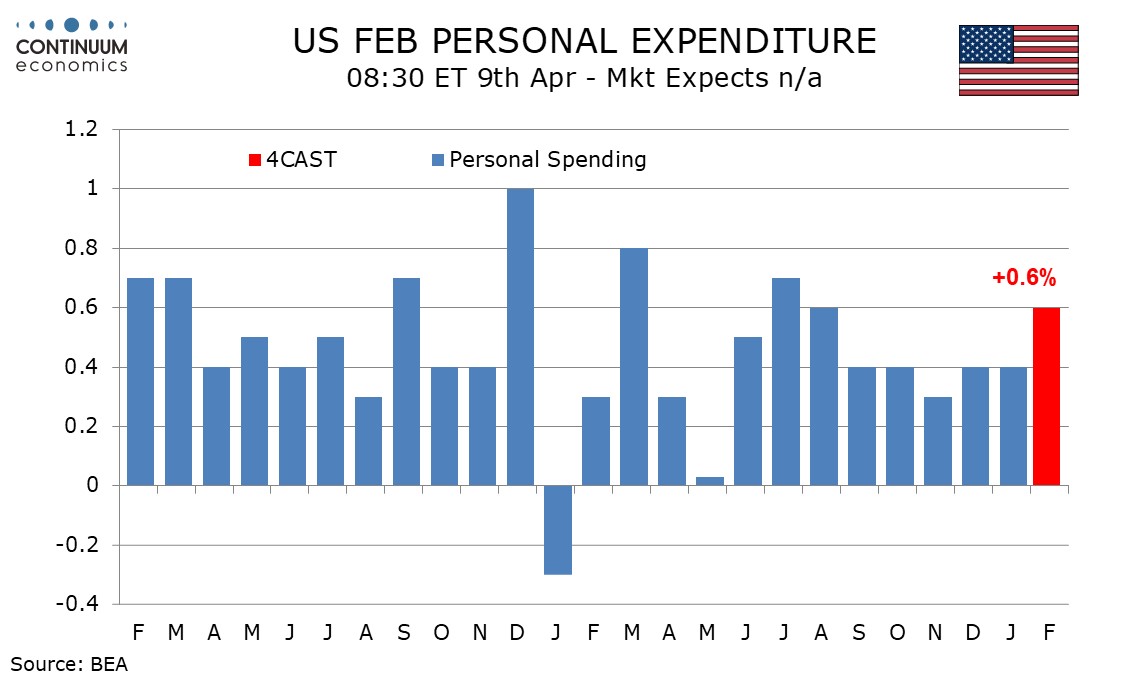

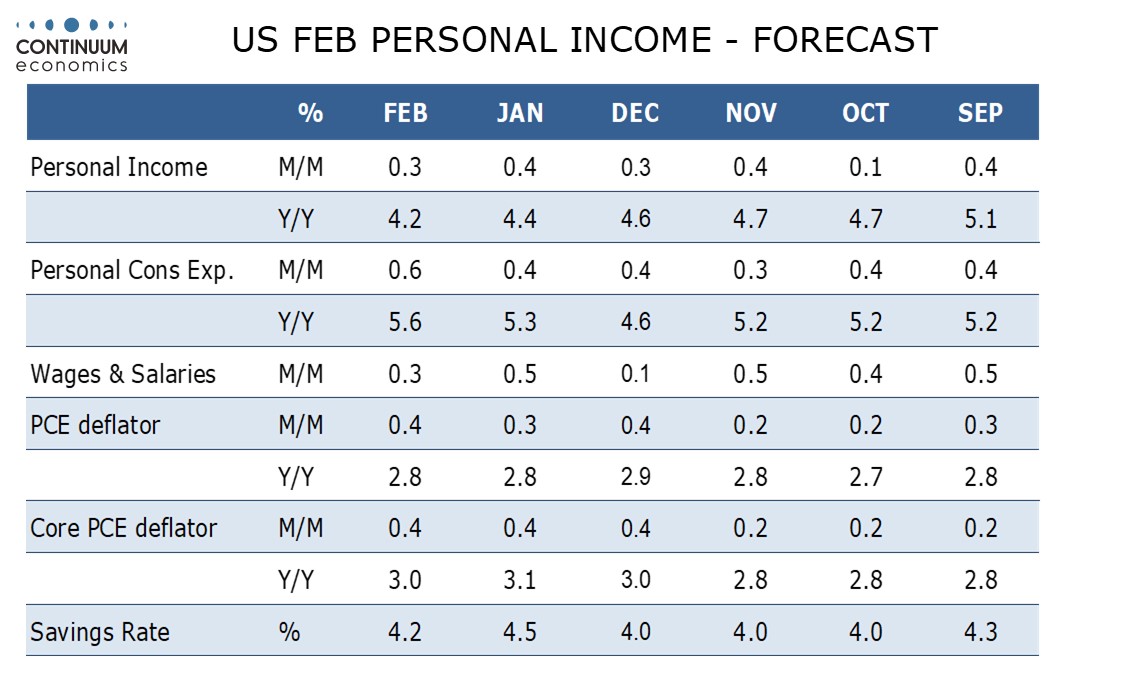

We expect February to see a third straight strong 0.4% increase in core PCE prices, while personal spending with a 0.6% increase outperforms a 0.3% rise in personal income. This will see a January bounce in savings corrected.

February CPI increased by 0.3% with the core rate ex food and energy up by only 0.2%. However the components of PPI that contribute to core PCE prices were mostly strong, and that is likely to keep core PCE prices elevated in February.

Yr/yr growth would then remain at 2.8% for overall PCE prices and slip to 3.0% from 3.1% for the core rate. This is in line with forecasts made by Fed’s Powell after the March FOMC meeting.

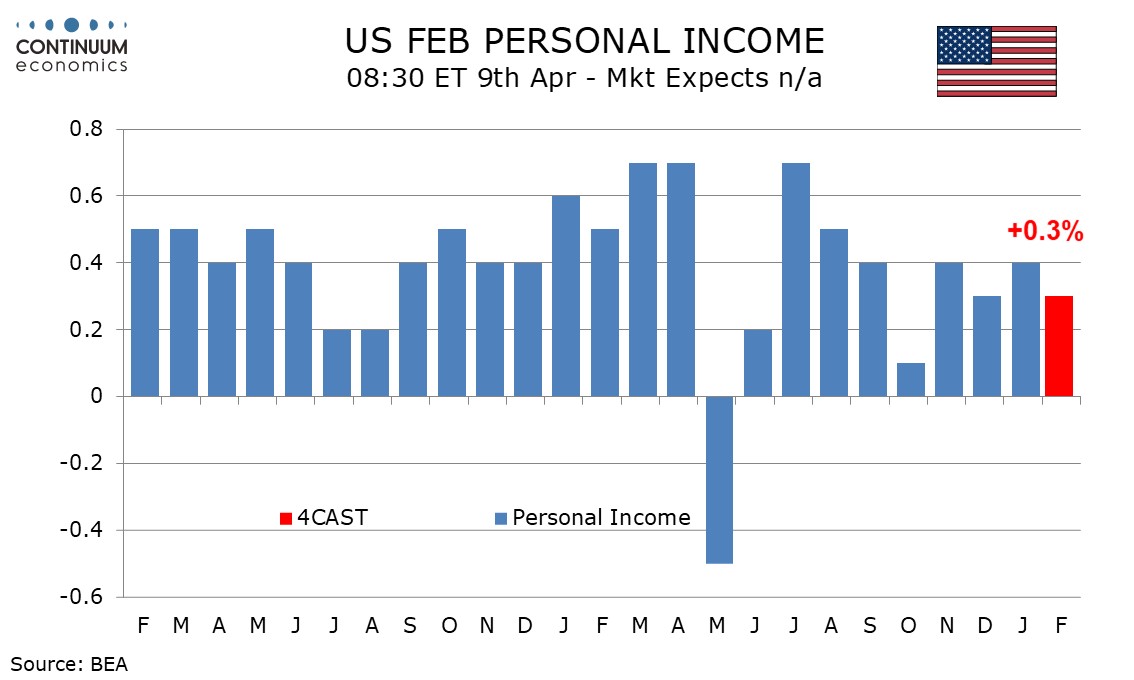

A more subdued February non-farm payroll breakdown is likely to see personal income slowing to a 0.3% increase from 0.4% in January. We expect wages and salaries to slow to 0.3% from a 0.5% increase in January, which bounced from a weak 0.1% rise in December.

We expect personal spending to match a 0.6% increase in retail sales, with services also seen increasing by 0.6%, though over half of the gain in spending will come from prices.

The savings rate would then slip to 4.2% from January’s 4.5%. January saw a bounce from 4.0% in December due to lower taxes.