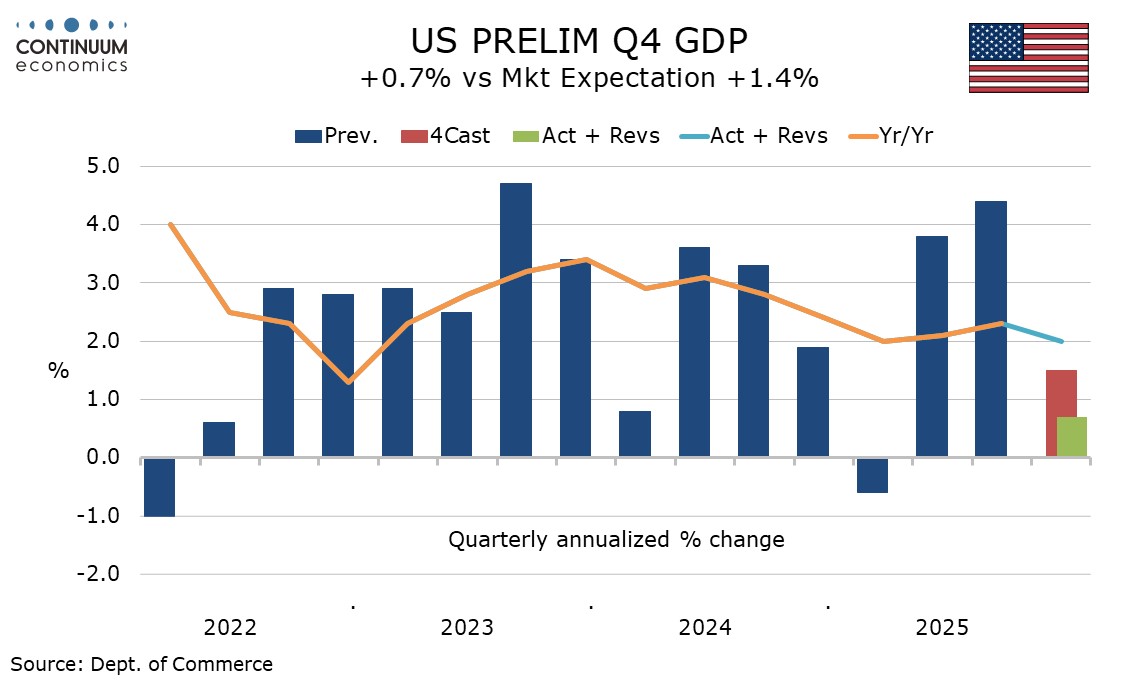

U.S. Q4 GDP revised down, Savings revised up, Core PCE Prices make a strong start to 2026

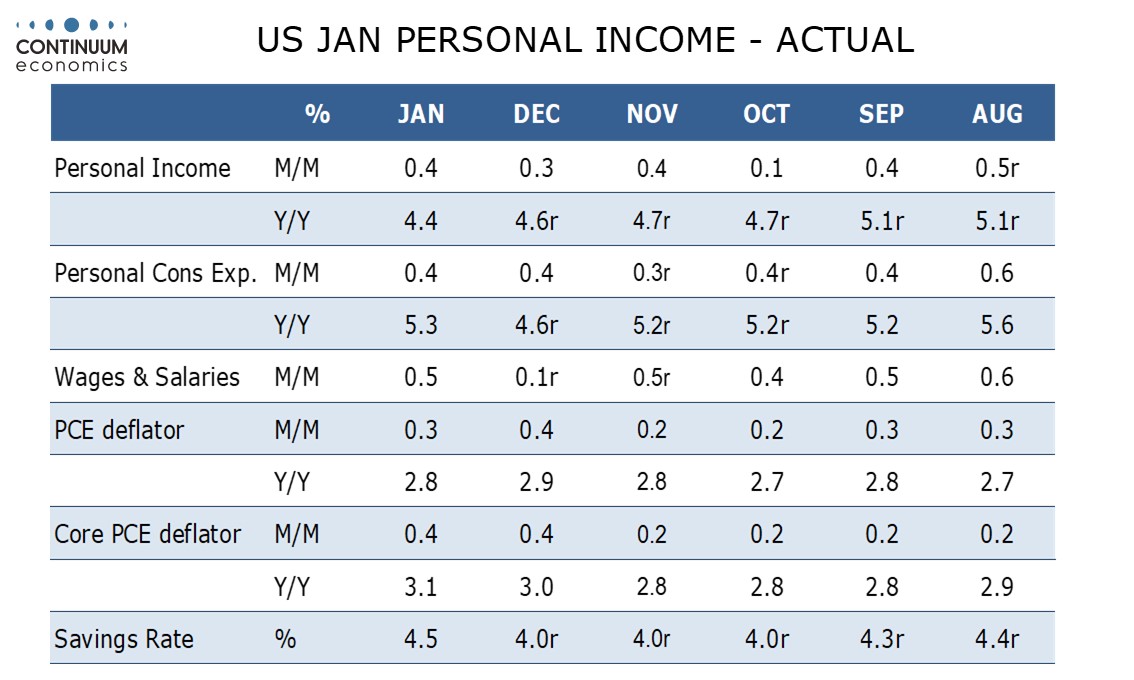

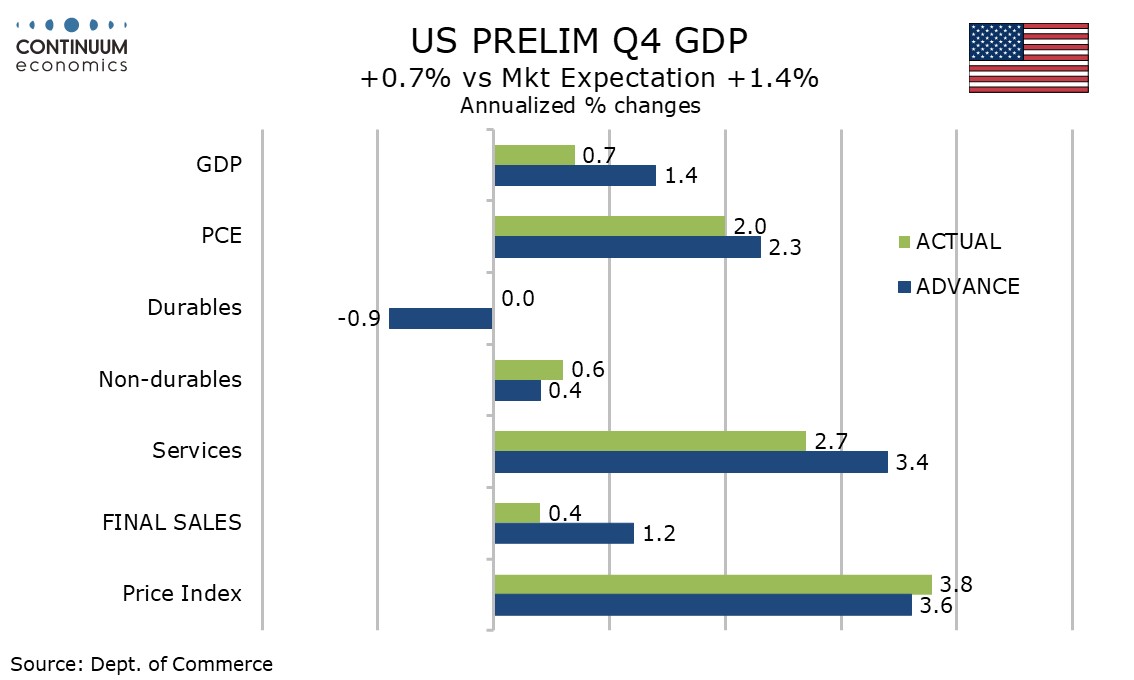

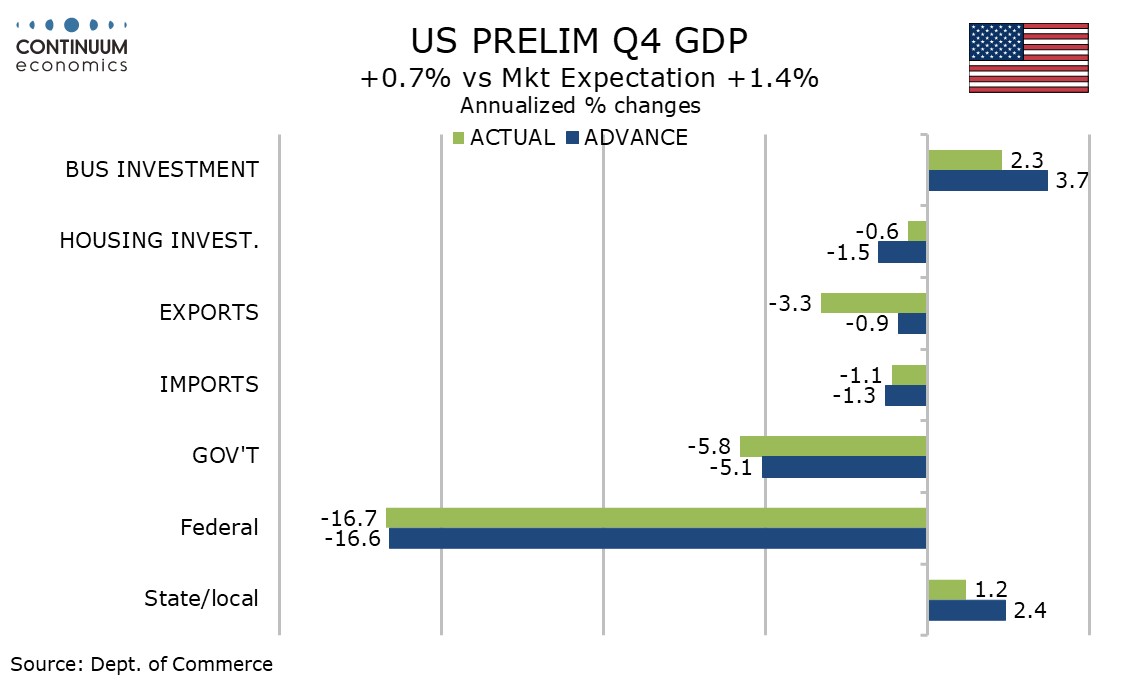

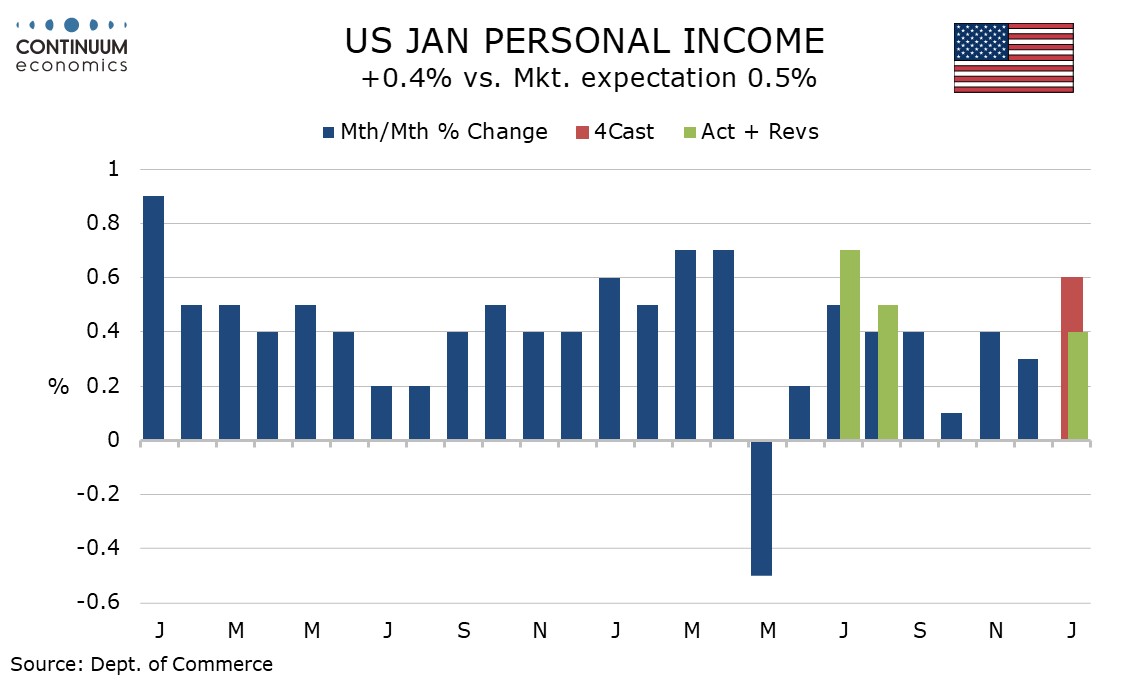

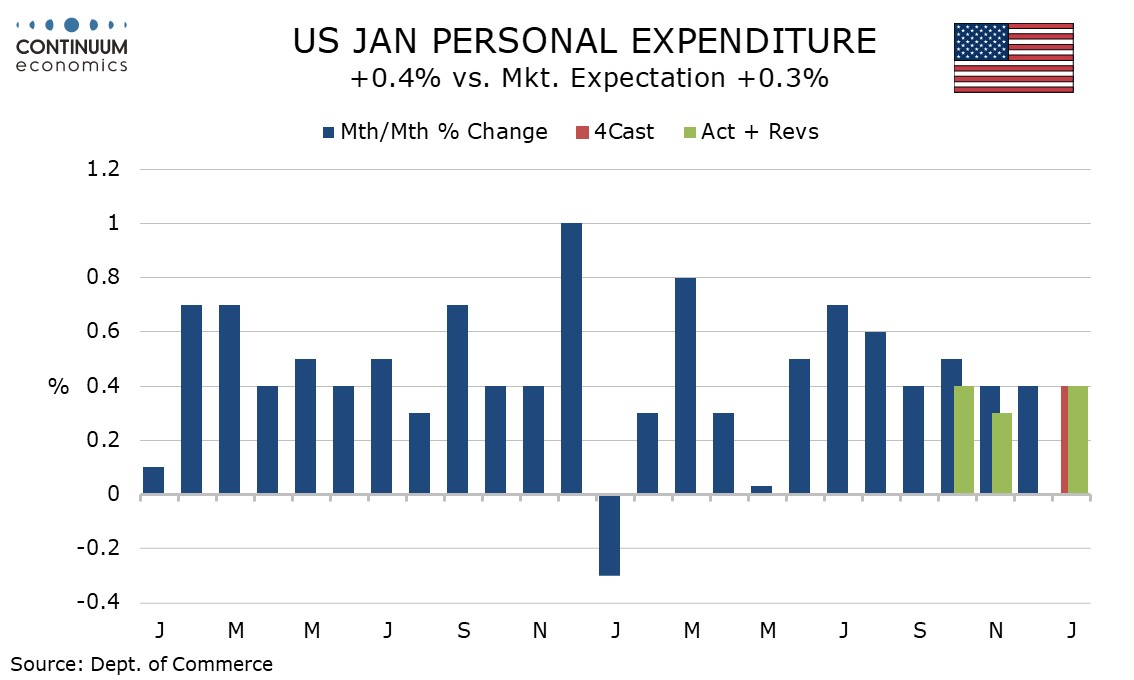

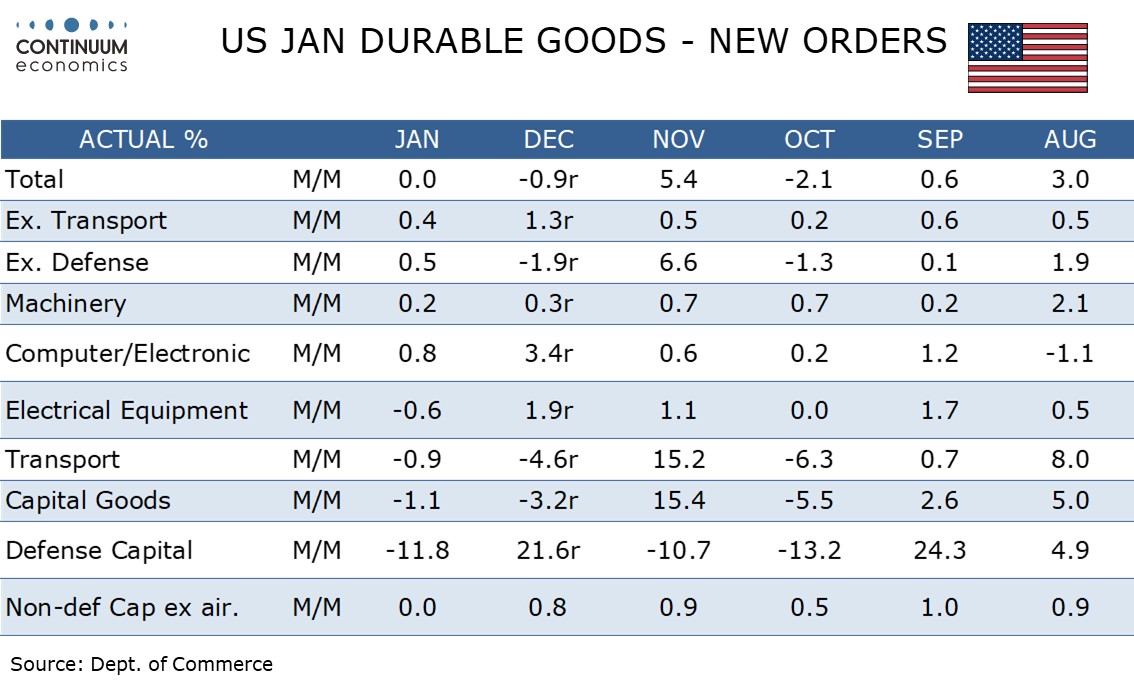

The latest US data is mostly on the weak side of expectations, most notably a broad based downward revision to Q4 GDP to 0.7% from 1.4%. January personal income, personal spending and core PCE prices all rose by 0.4%, net close to expectations, though upward revisions to savings reduce downside consumer risks somewhat. January durable goods orders were unchanged, weaker than expected, though ex transport orders continued to rise, by a moderate 0.4%.

The GDP revision totaled $45.8bn. $19.8bn of that came from services consumption, $13.2bn from business investment, led by structures, $18.6bn from net exports, almost entirely from a downward revision to service exports, and $7.3bn from government, the revision led by state and local, though Federal, hit by the government shutdown, remained weak, still taking 1.2% off from GDP. There were modest offsetting positive revisions from retail sales, housing and inventories.

When the first estimate of Q4 GDP was released, many noted that final sales to private domestic buyers (GDP less inventories, net exports and government) were relatively resilient at 2.4%. After the revision the gain stands at 1.9%, which is in line with long term GDP potential. Final sales (GDP less inventories) were revised to a weak 0.4% from 1.2%, with final sales to domestic buyers (GDP less inventories and net exports) not much better at 0.6% from 1.1%.

There was not much change to the price indices, with PCE prices and core PCE prices unrevised at 2.9% and 2.7% respectively, but the GDP price index stronger at 3.8% from 3.6%. Prices for government, the shutdown possibly a factor, and to a lesser extend investment, lifted the overall deflator.

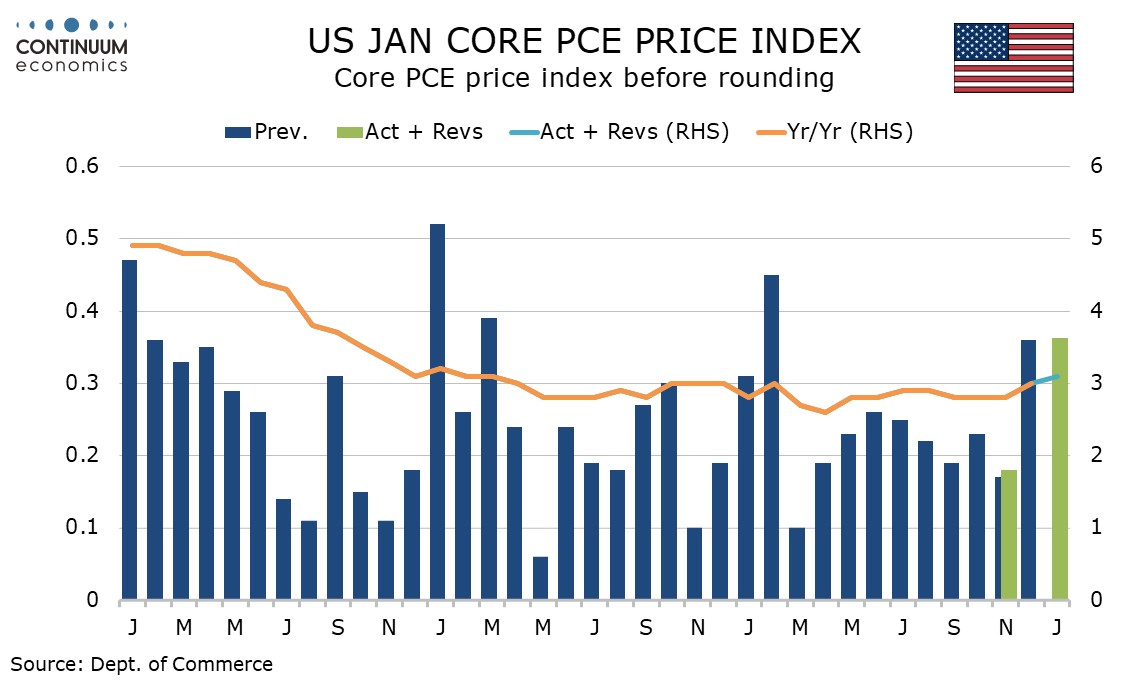

Prices made a strong start to 2026, with core PCE prices up by 0.4%, 0.36% before rounding, matching December’s gain. This was slightly stronger than a 0.3% core CPI with the components of January’s PPI that contribute to core PCE prices having been particularly firm. Overall PCE prices rise by 0.3%. The overall PCE price pace slowed to 2.8% yr/yr from 2.9% but the core rate at 3.1% from 3.0% is the highest since March 2024, and that will be worrying to the FOMC.

Personal income was slightly softer than expected at 0.4%, with wages and salaries at 0.5%, but disposable income was up by 0.9% (0.7% in real terms) as tax cuts from the One Big Beautiful Bill took effect. Revisions to personal income were positive too, Q4 marginally to 0.2% annualized from 0.1%, but Q3 more significantly to 1.0% from unchanged. Income is still underperforming spending in H2 2025 but disposable income may outperform in Q1.

A 0.4% rise in personal spending was slightly stronger than expected but Q4 was revised down to 2.0% annualized from 2.5%. The savings ratio now stands at 4.5%, its highest since July, with December revised up to 4.0% from 3.6%. Downside risks to 2026 consumer spending have been reduced.

Durable goods orders ex transport have now increased for nine straight months, and while January’s 0.4% increase is modest, December was revised up to 1.3% from 1.0%. Overall durable goods orders were unchanged, but a 0.5% increase was seen ex defense, and slippage in defense is likely to be temporary.

Transport was restrained by a fall in defense aircraft. Civil aircraft saw a marginal rise and autos a marginal fall. Non-defense capital ex aircraft orders were unchanged with shipments in the sector down by 0.1%. Not too much should be read into one subdued month here with trend still healthy.