Sweden – Riksbank Preview (May 8): Fresh Easing Hints?

A very likely stable policy decision next month would be the second in succession and where the Riksbank has now underscored that, with the policy rate now at 2.25%, this may be the end of the easing path. But amid the stronger currency, with real activity signs having largely disappointed even before tariff threats materialize, this time the Riksbank may be a little more open about the possibility of additional rate cuts. To some extent this is already the case but could make its forward guidance of it ‘will act if the outlook for inflation and economic activity so requires’ somewhat more biased towards easing. This would be even more likely if the April CPI data due the day before the decision add to signs that the inflation pick-up early in the year may have been a blip. Moreover, as no new forecasts are due until the June 18 Board verdict, the Riksbank can use rhetoric to hint at the policy outlook without recourse to formal projections.

We still see a further rate cut in June and also suggest that the risks of further moves both as the recent inflation scare recedes and the Riksbank takes note of the likely further rate cuts we think is in the offing from the ECB. In this regard the effective exchange rate has appreciated to five-year high and to almost what was envisaged by the Riksbank into 2026.

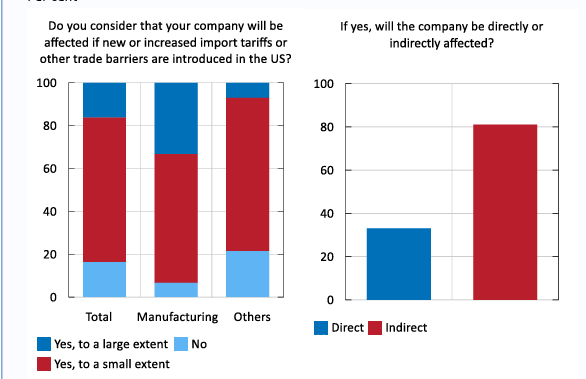

Figure 1: Swedish Companies’ Responses to Questions on Import Tariffs (%)

Source: Riksbank

Having delivered the widely-expected sixth successive rate cut in January, the Riksbank in March adhered to the assessment made in December that the easing cycle has drawn to an end with the policy rate (down to 2.25%) having dropped 1.75 ppt in eight months. Perhaps as notable last time around was that little otherwise changed with largely stable projections for growth, output gap and even inflation, save on the latter for a spike higher now factored into this year but with a return to target from early 2026.

Too Complacent?

But even with the fiscal situation likely to become somewhat easier into 2026 (an election year), we think that amid global uncertainties, and given still negative monetary dynamics (Figure 1), the Riksbank will have to make a downgrade to its real activity outlook – in due course as it still points to 2%-plus GDP growth for the next three years annually. We think that this consensus picture is too optimistic and it is noteworthy that the Riksbank has accepted a weaker consumer outlook but where the impact on GDP has been offset by a fall in import growth. Indeed, to us, that 2025 outlook of around 1.5% GDP growth also comes with downside risks which encompass a consumer recovery that may be much more feeble reflecting labor market uncertainty and what may be a sustained rise in household savings. The consumer picture is made more uncertain as an unfolding sharp rise in unemployment should mean that wage growth this and next year may fall from last year’s 3.8%.

Tariff Threat Detailed

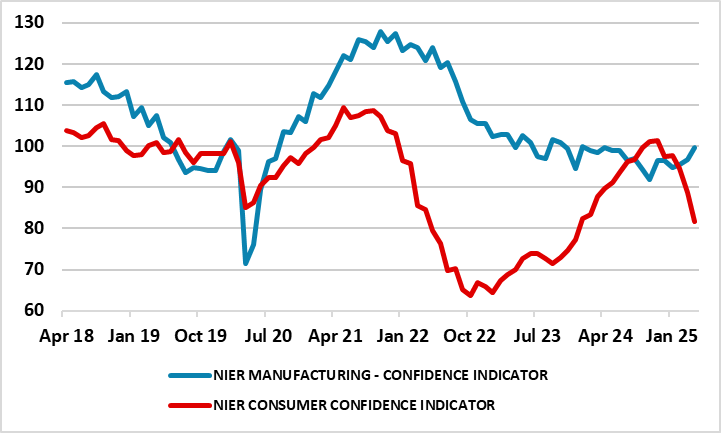

As for the threat of tariffs, for Sweden exports corresponded to around 55% of GDP with the major sales being road vehicles and machinery, pharmaceuticals, paper products and iron, steel and iron ore and where after other European countries, the U.S. is the third largest single export destination. We do not see a major direct impact, but we do note that, as with many other countries, it is the indirect impact on matters like confidence and uncertainty that may wreak the most damage. This is very much evident in a recent Riksbank survey about import tariffs and their impact on companies’ operations (Figure 1). Notably, while this line of thinking is borne out in business surveys which show resilient manufacturing thinking, the indirect impact of uncertainty is weighing very much on Swedish consumers (Figure 2).

Figure 2: Consumer Sentiment Slumping Afresh!

Source: National Institute for Economic Research – KI - % balance

While the tariff threat may dissipate somewhat, we think that uncertainty will continue to be major headwind to the Swedish economy generally and the consumer particularly – this possible helloing explain what looks to have been a weak Q1 that very much undershot Riksbank expectation of 0.5% q/q growth. All of which could mean an output gap of well over 1% having emerging through into 2025 (may persist should not get larger as we see near-trend growth of 1.7% in 2026. Allied to consumer weakness sapping pricing power, this will weigh on inflation. Already, the Riksbank (justifiably) sees the recent spike as being short-lived and due a marked change in the reweighting of the CPI basket. This will have created a marked base effect and hence why the Board sees CPIF inflation slumping back in early 2026 but it may occur a little earlier.

Alongside further rate cuts from neighbouring central banks, we think this will trigger what may be a further and possibly not a final Riksbank cut at the June meeting!