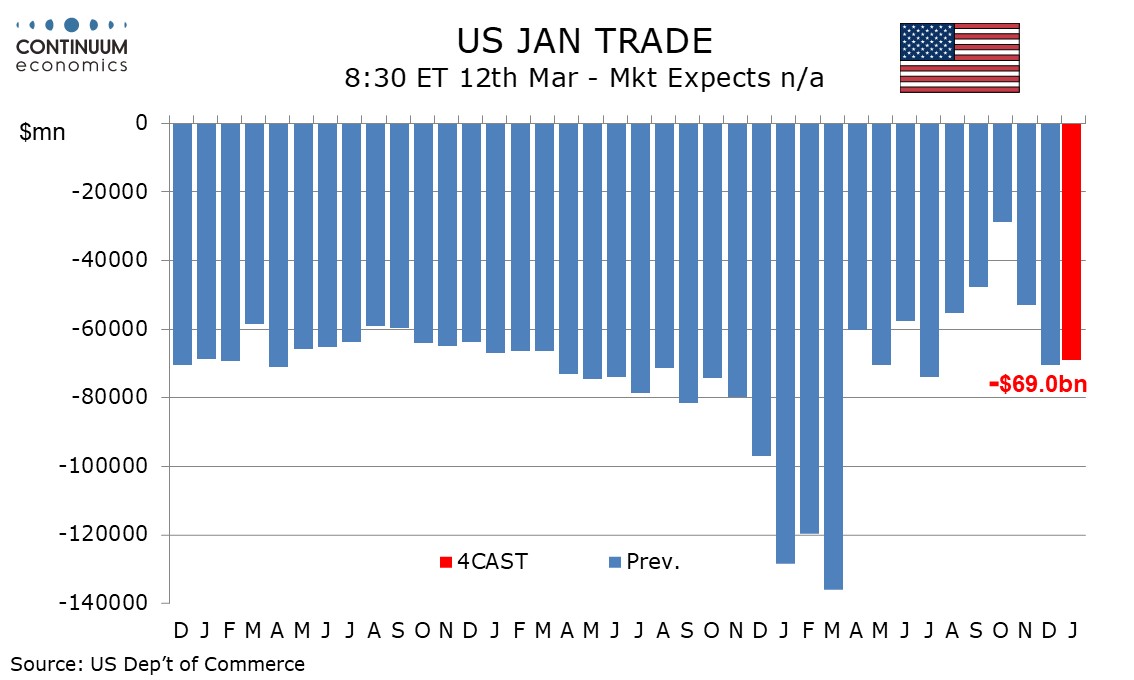

Preview: Due March 12 - U.S. January Trade Balance - May be stabilizing close to pre-tariff levels

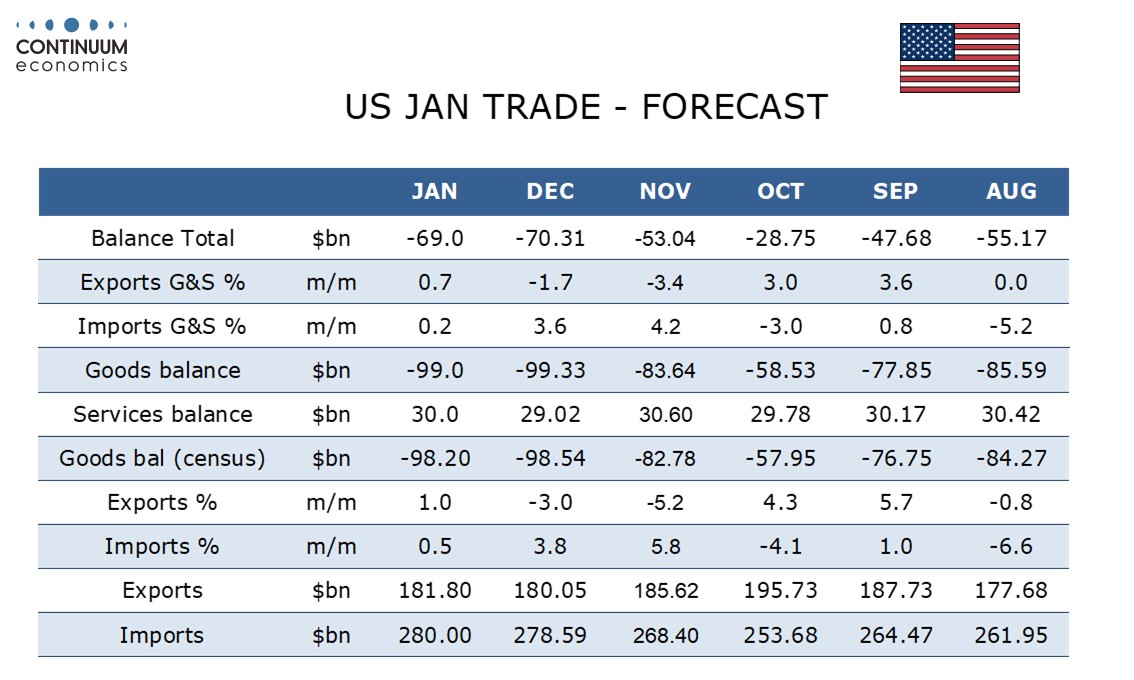

We expect a January trade deficit of $69.0bn, which would be only a marginal correction from December’s $70.3bn which was the widest since July, though still well below the record $136.0bn deficit seen in March of 2025 shortly before the tariff announcement.

Despite the huge volatility in monthly trade data caused by policy changes, the average monthly deficit in 2025 of $75.1bn was almost exactly the same as that for 2024 at $75.3bn. December’s trade deficit may represent a return to normalization, implying little change in January should be expected.

Goods exports surged in September and October largely on strength in nonmonetary gold but have since corrected back. Nonmonetary gold exports are still probably marginally above likely long-term levels but we expect a modest 1.0% in January goods exports, more on prices than volumes. Goods imports have also been volatile, plunging in October led by pharmaceutical preparations which are still quite weak and have some upside scope. However imports of computers have recently been very strong but are showing signs of peaking. We expect goods imports to rise by a modest 0.5% in January, with little contribution from prices.

We expect a rise in the services surplus as exports increase by 0.3% after a 0.4% December gain but imports fall by 0.8% after a surge of 2.7% in December. This would leave overall exports up by 0.7% and overall imports up by 0.2%. Service imports are likely to bounce in February on Winter Olympic TV payments.