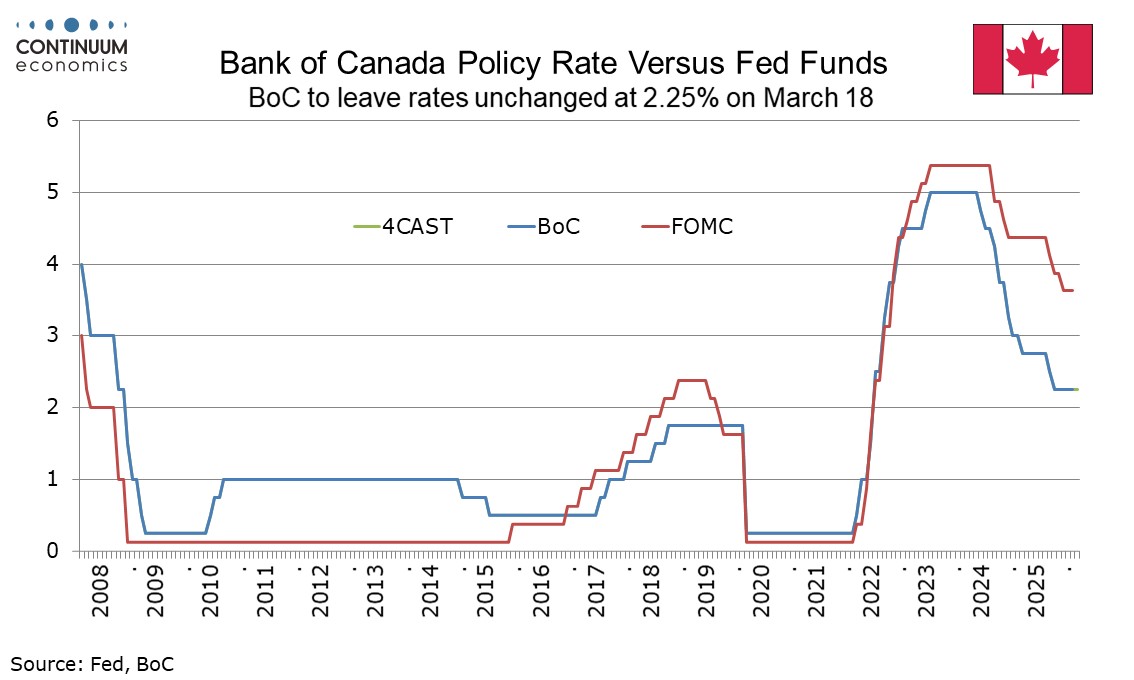

Bank of Canada Preview for March 18: No change in rates or from January's message

The Bank of Canada meets on March 18 and looks highly likely to leave rates unchanged at 2.25%. The statement is likely to reiterate the message given at the last meeting on January 28, that the policy rate is appropriate conditional on the economy evolving in line with expectations, but uncertainty is heightened and if the outlook changes the BoC is prepared to respond.

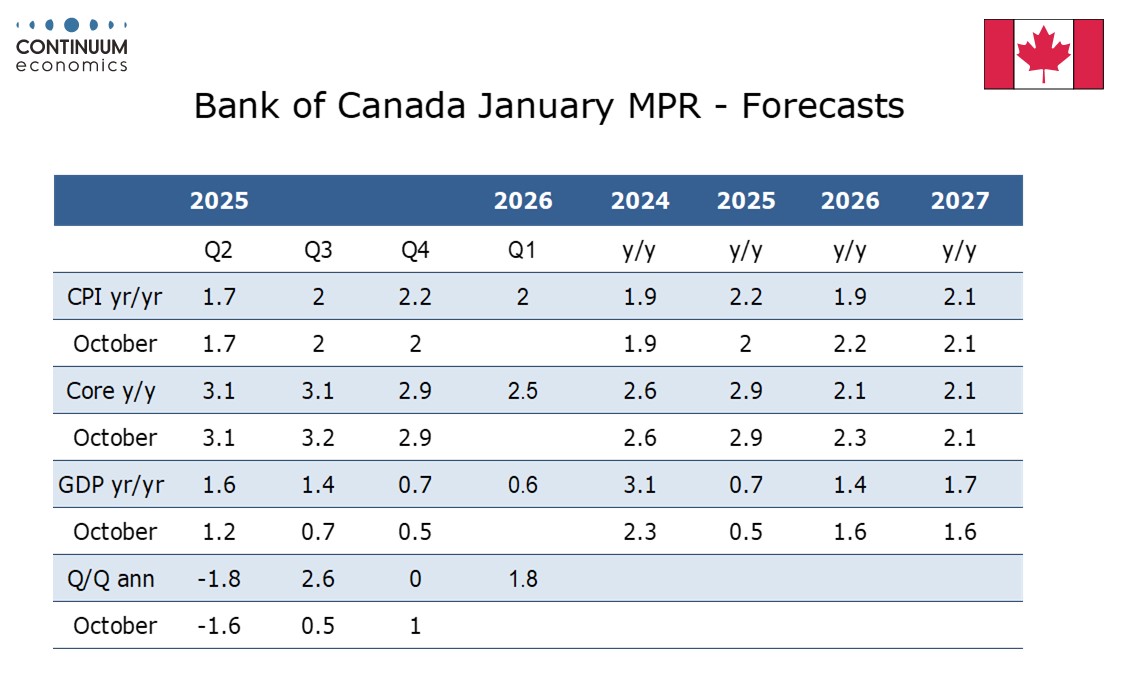

This meeting will not see a quarterly Monetary Policy Report so the forecasts made with the last MPR on January 28 will not be updated. Since the last meeting Q4 Canadian GDP came in weaker than expected at -0.6% annualized, but with domestic demand up by 2.4%, albeit with significant support from government stimulus, the data is unlikely to change the BoC outlook significantly. Underlying inflation appears to be slowing though strength in oil prices is likely to mean Q1 CPI comes in a little stronger than the 2.0% projected by the BoC in January.

Canada’s economy will be more resilient overall than most to any sustained boost to oil prices, though outside the oil-rich province of Alberta the economy would be likely to weaken. The extra near term inflationary risk reduces what were already quite slim chances of a BoC easing, while tightening still looks some way off. Minutes from the last meeting show that Iran was one of a number of risks discussed, including Venezuela and Greenland, where risks have faded since January. Other risks discussed were threats to the independence of the Federal Reserve, and the upcoming review of the Canada-US-Mexico trade agreement, which persist. The US Supreme Court ruling against some of Trump’s tariffs is a positive development, but uncertainty overall has increased since January, due to the Middle East situation.

The Bank of Canada will be able to give limited forward guidance given the heightened uncertainty. January saw the BoC state that it expects GDP to increase by 1.1% in 2026 and 1.5% in 2027 with inflation remaining close to the 2.0% target over the projection period. We see risk to growth being marginally to the upside of the BoC’s projection, though inflation is likely to be well contained outside a potential boost from oil. We continue to expect the BoC to tighten once this year, in Q4, and once in 2027, in Q2, with each move by 25bps. That would take rates to the middle of the 2.25%-3.25% rage the BoC sees as neutral. Currently rates are at the bottom of that range.