Sweden Riksbank Review: Everything Unchanged?

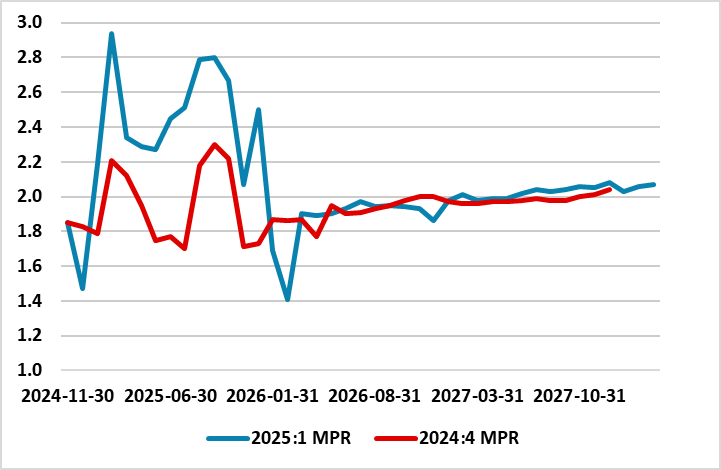

Having delivered in January, the widely-expected sixth successive rate cut, the Riksbank adhered to the assessment made in December that the easing cycle has drawn to an end with the policy rate (down to 2.25%) having dropped 1.75 ppt in eight months. Especially given the recent upside CPI surprises, this very much pointed to no move at today’s (March 20) decision and with a stable policy outlook likely to be reinforced by updated projections that may continue to point to above-consensus growth this year and next. This is what occurred, again surprising few, if any. Perhaps as notable was that little otherwise changed with largely stable projections for growth, output gap and even inflation, save on the latter for a spike higher now factored into this year but with a return to target from early 2026 (Figure 2).

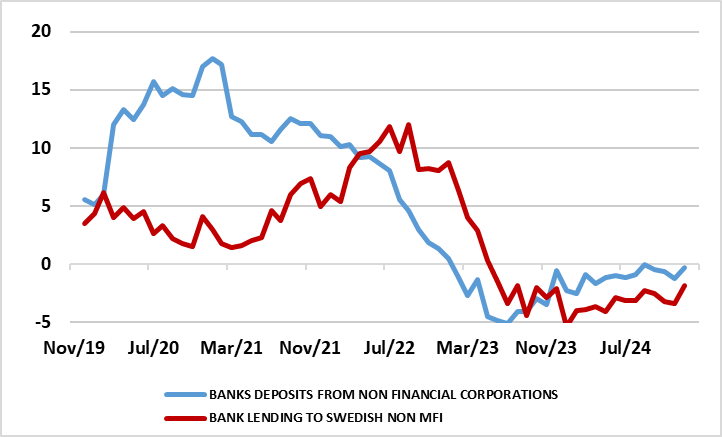

Figure 1: Bank Lending and Deposit Growth Still Negative – Even Nominally

Source: Riksbank

But even with the fiscal situation likely to become somewhat easier into 2026, we continue to think that amid global uncertainties, and given still negative monetary dynamics (Figure 1), the Riksbank will have to make a downgrade to its real activity outlook. This is largely unchanged from the December Monetary Policy Outlook and still points to 2%-plus GDP growth for the next three years annually. We think that this above-consensus picture is too optimistic and it is noteworthy that the Riksbank has accepted a weaker consumer outlook but where the impact on GDP has been offset by a fall in import growth. Indeed, to us that 2025 outlook also comes with downside risks which encompass a consumer recovery that may be much more feeble reflecting labor market uncertainty and what may be a sustained rise in household savings. The consumer picture is made more uncertain as an unfolding sharp rise in unemployment should mean that wage growth this and next year may fall from last year’s 3.8%.

There is also the fact that 2022-23 Riksbank tightening still seems to be biting given the continued marked and nominal fall in bank lending (Figure 1) evident in much shorter periods than just y/y rates too. Indeed, we think that the latter is a reflection of Riksbank policy also biting unconventionally as its balance sheet reduction, which had caused a marked drop in bank deposits (now only partly repaired) and where this weakness is affecting banks willingness/ability to lend.

Figure 2: Volatile but Still Backing Toward Target

Source: Riksbank – CPIF % chg y/y

As telling is the likelihood that housing construction (which has already fallen steeply due to lower house prices, higher construction costs and expensive financing) continues to contract into next year with an added negative now emerging in terms of much softer population growth. All of which could mean an output gap of over 1% having emerging through into 2025 (as the Riksbank accepts) may persist should not get larger as we see near-trend growth of 1.5% in 2026. As for inflation, the Board (justifiably) sees the recent spike as being short-lived and due a marked change in the reweighting of the CPI basket. This will have created a marked base effect and hence why the Board sees inflation slum ping back in early 2026 (Figure 2).

Alongside further rate cuts from neighbouring central banks, we think this will trigger what may be a final Riksbank cut, not least if the current surge in the exchange rate persists. But any such further 25 bp may be deferred until the June meeting, if not later!