USD, EUR, JPY flows: USD down on tariff rise, JPY favoured

The market seems to have been unprepared for the well flagged US tariff increase, and equity weakness and bond yield declines suggest JPY gains most reliable

Despite having been repeatedly warned of the likely tariff increases ahead of the announcement, equity markets sold off heavily in response to last night’s US announcement of swingeing across the board increases. The FX response has been a response to the equity market moves, rather than any specific concerns about individual economies. It is notable that the largest declines are in the US equity markets, with the S&P down almost 3%, while European equity futures are down less than 2%. This reflects both the high valuation starting point in the US, and the fact that, in the short run at least, most of the tariff impact will fall on the US. The increase in import prices will mean an increase in US prices and a decline in real US demand as a result. The effect on other economies will initially be smaller, as reduced US demand will have an impact only proportional to each country’s exports to the US (unless they respond with immediate equivalent retaliatory tariffs). Eventually, if US importers decide to change to domestic suppliers to avoid tariffs, there could be a further impact, but this will take time and it still isn’t clear that alternative US suppliers will be cheaper.

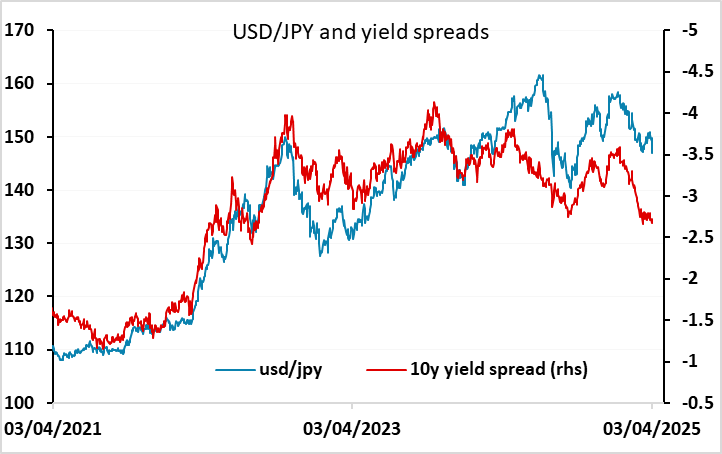

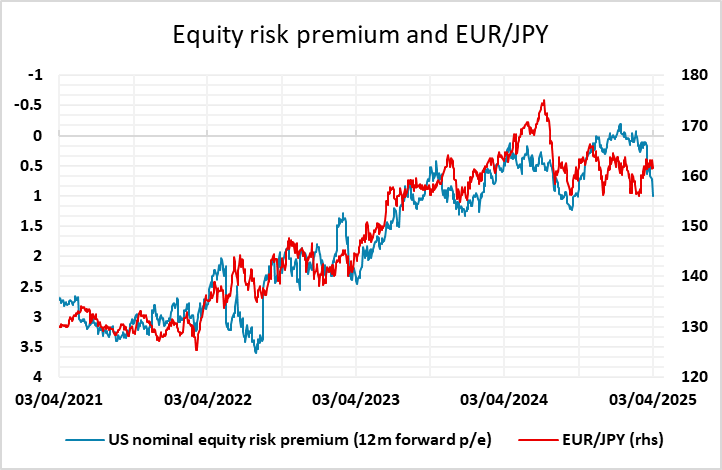

For FX markets, the JPY has been the biggest beneficiary, unsurprisingly reacting to the combination of lower global yields and lower equity markets. The JPY metrics suggests there is scope for substantial further JPY strength. Yields spreads have suggested scope for further USD/JPY declines for some time, but the low level of US equity risk premia has tended to limit the scope for JPY gains on the crosses. But equity risk premia have risen significantly with the decline in both yields and equities, and point to substantial EUR/JPY declines as well.

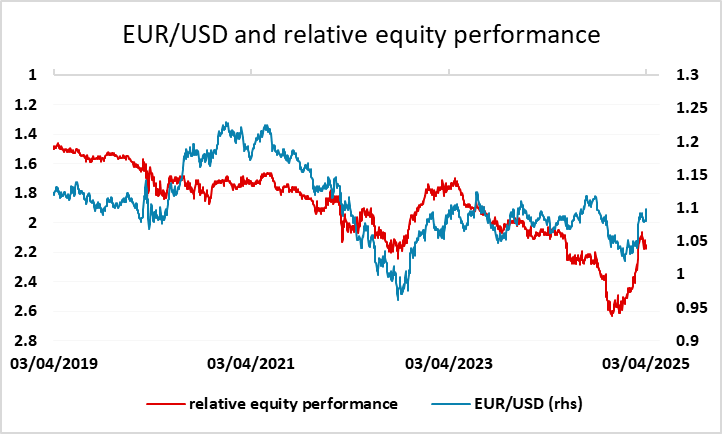

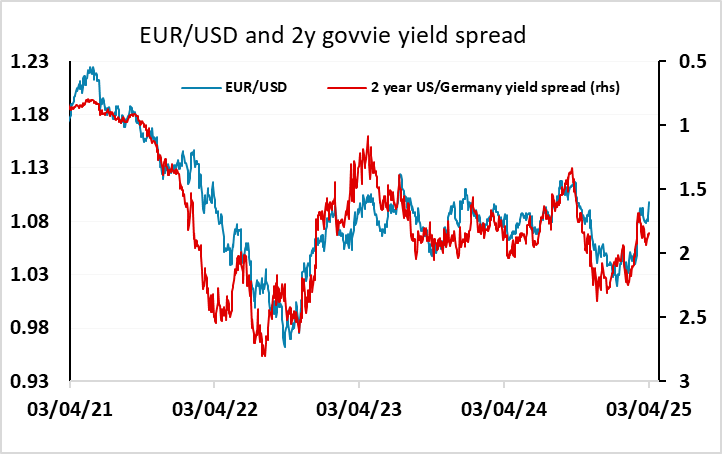

For EUR/USD, the picture is less clear. Yield spreads don’t obviously support EUR gains, and while the relatively large fall in US equities does provide some EUR support, it is minor compared to the relatively strong European equity performance seen since the start of the year. From an economic perspective, the Eurozone benefits slightly from being a relatively closed economy (as a whole), relying more on domestic demand than trade. The EUR also starts out as a relatively cheap currency - only the JPY among the G10 is cheaper relative to PPP against the USD. But the EUR gains seen so far look more based on general USD negative sentiment and the fact that the EUR is the main USD antipole and reserve currency alternative than a positive EUR view, and we would see gains above 1.10 as likely to prove hard to achieve.