Banxico: December In Doubt and Pause Closer

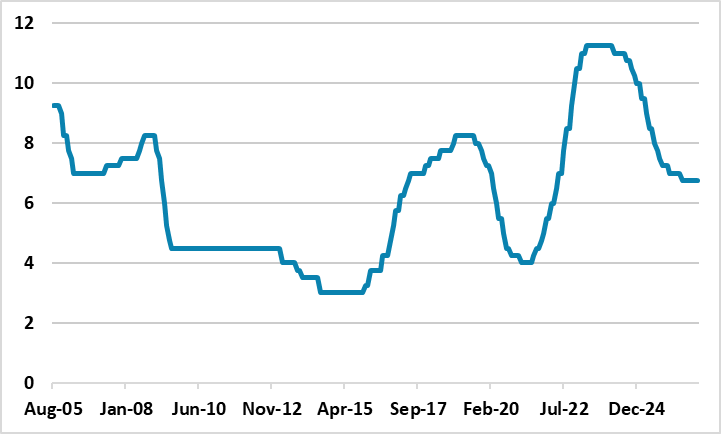

The December Banxico meeting is not guaranteed to see a further 25bps cut, with the November Banxico statement showing more caution over persistent core inflation pressures and given the cumulative easing already seen. Combined with the risk of a Fed pause in December, plus Banxico’s Mexican Peso (MXN) watchfulness, we attach a 60% probability to no cut in December. We do look for a 25bps cut in Q1 and then one final cut to 6.75% before Banxico pauses for past easing to feedthrough.

Figure 1: Banxico Policy Rate Including Forecast (%)

Source: Continuum Economics

Banxico cut the policy rate by 25bps as widely expected to 7.25%. The mood from the statement appears to leave the door open to a further 25bps cut at the December meeting, but with growing signs that the easing cycle is getting to a mature stage. Banxico slightly nudged up core inflation projections in Q4 2025 plus Q1 and Q2 2026, but still expects headline inflation to hit target in Q3. Combined with the ongoing Banxico concern over domestic economic weakness (e.g. Q3 GDP), this builds the case for a further 25bps cut at the December meeting.

However, the Banxico statement said that “looking ahead, the Board will evaluate reducing the reference rate,” replacing the strong wording of “assess further adjustments.” Additionally, global risks were overtaken by persistence of core inflation in 2nd place behind the exchange rate depreciation risk. With the Fed signaling that a December rate cut is not a done deal, Banxico are also watchful of the MXN and the 10yr bond spread versus Treasuries. Banxico meet December 18 after the Fed decision on December 10. No Fed cut would likely be followed by no cut from Banxico, while a Fed cut would give Banxico more confident and could tip the balance in favor of a 25bps December cut. Mexican real sector and inflation data are also a swing factor. We stick with a view that of no cut in December with a 60% probability, which means it is close and fluid call for the last meeting of 2025.

Nevertheless, we do see the prospect that Banxico cuts in 2026 and we are penciling in 25bps in Q1 down to 7.00%. The current economic arguments will favor ongoing easing though at a slower pace rather than every meeting. Additionally, Banxico estimate that the neutral real policy rate is 1.8-3.6%, which would mean that a decline in CPI inflation next year could allow the policy rate to be cut to stop the real policy rate rising outside of the neutral real policy rate band. However, trade tensions with the U.S. will likely resurface, as President Trump seeks to renegotiate USMCA in H1 2026. This can cause MXN volatility, which could cause Banxico to extend the pause from December or deliver one 25bps cut in Q1 and then pause. On balance, we see 25bps in Q1 to 7.00%. We still have a further 25bps to 6.75% in Q2, but this could be delayed. Thereafter we see a pause for the remainder of 2026, as Banxico waits for previous monetary easing to feedthrough.