Sweden Riksbank Review: On Hold and More Likely Still For Some Time

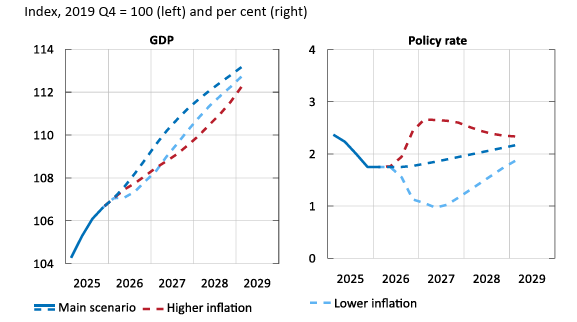

Surprising hardly anyone, the Riksbank (again) kept policy on hold with the key rate left at 1.75% it latest verdict. However, what was more important was if and how the Board changed its rhetoric. In this regard, it repeated its assertion of no change for some time to come but qualified it somewhat by noting that amid Middle East conflict making the forecast very uncertain, it would adjust monetary policy if the outlook for inflation and economic activity so requires – this presumably suggesting a move in either direction. Indeed, in its scenario analysis it has an outlook of a more significant fall-out from the war causing higher inflation requiring higher rates and an alternative in which rates need to be eased further due to lower inflation. The bottom line is it in justifiable wait and see mode with its central policy scenario unchanged from that of three months ago.

Figure 1: Riksbank Alternative Scenarios

Source; Riksbank March Monetary Policy Report

But the updated GDP and CPI outlooks by the Riksbank may need to be pruned back after what have been unexpected weak readings for both of late, some of which may be attributable to the recent appreciation of the Krona. The inflation undershoot is modest and we concur in seeing CPIF inflation staying below target for the foreseeable future – the Board seen no move above 2% until early 2028 and that will be partly a result of April’s scheduled food VAT cut being reversed.

Otherwise and as we have suggested repeatedly, the Riksbank GDP projection for this year is overly optimistic, and at 2.5% possibly by a factor of two, with the Board having revised it down a mere notch. In this regard, the real economy backdrop is still puzzling and meriting more of a reassessment. Despite an apparent 2%-plus GDP jump in the last three quarters if 2025 (twice Riksbank thinking), the economy still looks soggy, not least in the labor market. Admittedly, much of the recent rise in unemployment to around 9% of late looks to be a result of increased participation, but does this reflect a need to boost what have been damaged (real) incomes; if so then there may be little respite with the rate staying around current levels for at least the rest of this year. Moreover, business surveys are mixed to soft while the Riksbank will note the results of its own survey (taken in early February), which even then underscored that ‘Swedish companies envisage that the recovery is both slow and hesitant. The uncertain global environment has had a significant impact on household consumption and business investment, making companies cautious looking forward’. This all shows up in early year growth data (ie for the period before the war broke out) that suggests GDP will contract in the current quarter. And then there is the spill-over from the Middle East conflict.

It is against this background where we now see a GDP growth outcome nearer 1.2% for this year, with weaker exports causing clear damage that, alongside the likely Q1 drop, have warranted what is a 0.6 ppt downward revision compared to three months ago. Helped by fiscal policy and the anticipated fall back in energy prices we see GDP growth outcome nearer 1.7% next year. This very much suggests a negative output gap, at least until 2028.

As a result, the Board promise of no change for some time to come is likely to be met and maybe with a clearer downside risk that upper. More likely, we still do not see any looming policy reversal, as we see this current policy rate (1.75%) staying in place through 2027, ie a little longer than the Riksbank which envisaged the first hike probably at end 2026.

Finally, there is a saying that one should be careful about what you wish for. In this regard, the Riksbank aspiration of a strong(er) currency and low inflation is being more than met and we were surprised that the Krona did not get more of mention. The currency has risen strongly and is certainly a key factor in the current on-going disinflation, with imported consumer goods actually negative in y/y terms.