UK Spring Fiscal Statement – A Patch-up Not a Repair Job?

Chancellor Reeves never wanted a fiscal event at this juncture. But market pressure and economic weakness have forced her into a series of government spending cuts designed to shore up her recently revised fiscal goals via this so-call spring statement. The problem here is twofold. Firstly, the repair of the current budget surplus goal looks insubstantial (Figure 1) and thus may lack credibility as it merely restores the flimsy headroom projected last October. As such this poses the threat that the Chancellor will have to make more fiscal adjustments – all to the detriment of the economy in the rest of the year, at either/both the June Spending Review or the Autumn Budget. But this highlights the second problem in that that Autumn Budget the Chancellor may have to find cover for even more fiscal slippage, with the clear threat being that the Office for Budget Responsibility (OBR) may then pare back what we regard are still optimistic growth and particularly productivity assumptions (Figure 2) – something that need much more fiscal tightening than seen at this juncture!

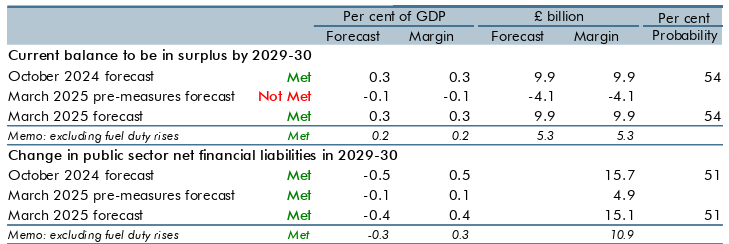

Figure 1: Fiscal Headroom Repaired – But Only Just!

Source: OBR - Performance against the Government’s fiscal targets

The Word Has Changed

Her aspiration as Chancellor was to have just one fiscal ’event’ per year, namely a full Budget every Autumn. But the law dictates that the government must update economy forecasts twice a year, so she always knew she would have to make some presentation probably in the spring – but merely to reveal changes in the economic picture as seen by the OBR. But ever since the Budget last October the likelihood of an actual spring fiscal ‘event’ has been growing steadily. Indeed, a rise in market interest so far this year has boosted estimated debt servicing costs while continued weakness in the real economy has seen current year public borrowing increasingly exceed target. And further overshoots were looking more likely, as the anticipated positive impact of her large fiscal stimulus last October has been offset by a combination of damage to sentiment from the tax changes highlighted alongside while a new U.S. administration has set the scene for a possible trade war that would only accentuate already clear fragility in the global and particularly European economy.

Risks are Still Marked

In this regard, the Chancellor is right to suggest she has to act now as time have changed, although this misses the point that much of what has transpired was hardly a ‘bolt from the blue’. Moreover, it does seem as if the Chancellor is still willing to take risks. She may have restored the headroom on her current budget fiscal rule but only to what it was estimated last October (Figure 1). Then it was historically small (ie a third of the historic average) and hence fragile and must be considered to be so still. This is even more so given it is based on what we think are optimistic growth assumptions. It also is partly an accounting tweak caused by the shift in defense spending from overseas aid encompasses les current spending. Finally, it still assumes a sizeable (and politically difficult) rise in fuel duties in the next fiscal year, without which the fiscal headroom more then almost halves. In regard to meeting this current budget rule fiscal rule, the OBR itself notes’ there is significant risk around the central forecast for the current budget. Based on stochastic simulations, the probability of meeting the fiscal mandate is 54 per cent’.

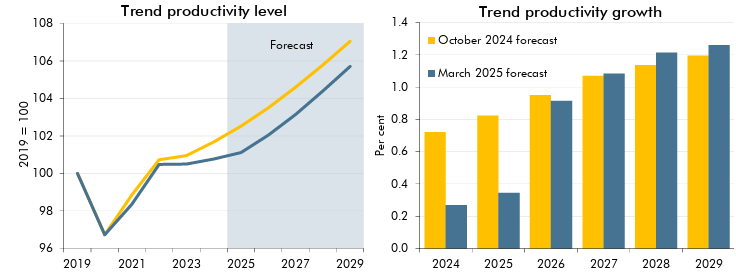

Figure 2: OBR Productivity Outlook Still Too Optimistic?

Source: OBR, annual trend productivity level and growth

Productivity Issues

But over and above the issue of repairing the current budget rule, the risk is that a fresh and possibly more sizeable fiscal overhaul may be needed possibly before year end. This is unlikely to be at the likely June Spending Review, but instead may occur at the autumn annual Budget. This could be in reaction to continued economic stagnation as opposed to what we regard is still an optimistic 1% GDP forecast for the year, even though it has been halved by the OBR today. But the other and possibly larger risk (both in terms of likelihood and possible implied fiscal tightening) would be if the OBR pared back further (and more sizeably its assumption) regarding productivity. As Figure 2 shows, while having revised down the near-term picture, the OBR still assumes a steady recovery in productivity in coming year to twice the 0.5% average in the decade prior to the pandemic. But if the OBR decides that a continued undershoot of productivity forecast warrant a significant reassessment this it has major implications for the fiscal finances. Indeed, halving back projected productivity growth in 2029-30 from 1%-plus could damage the budget outlook by over £ 40 bln, something that would also flout the budget rules. If so, then the fiscal adjustment announced to today would be modest in comparison.

With this statement today a Spending Review in the summer and then the Autumn Budget, the Chancellor may not agree with the old adage that ‘good things come in threes’!