UK Political Risk – Bad Things Come in Threes?

The biggest set of elections since the 2024 general election takes place on 7 May in the UK. Already, UK markets are fretting about the possible outcome, in particular that serious electoral damage to the Labour Party currently running the government could make it swing more to left and dilute fiscal prudence with or without a change in PM. This is a clear risk, but it is not the only one. The likely damage that Labour will face has already been dealt to the Conservative Party two years ago, to a degree that the familiar UK two-party system that has run the country since 1922 is in tatters. Already a series of previously fringe parties have come to the fore led by Reform and the Greens so that the UK now has five parties (seven to eight including the devolved parties) realistically vying for electoral attention. Given the UK’s electoral system, this points to little chance of any party getting enough votes in the next general election that must be held by 2029 – all pointing to even greater, if not unprecedented, political instability looming.

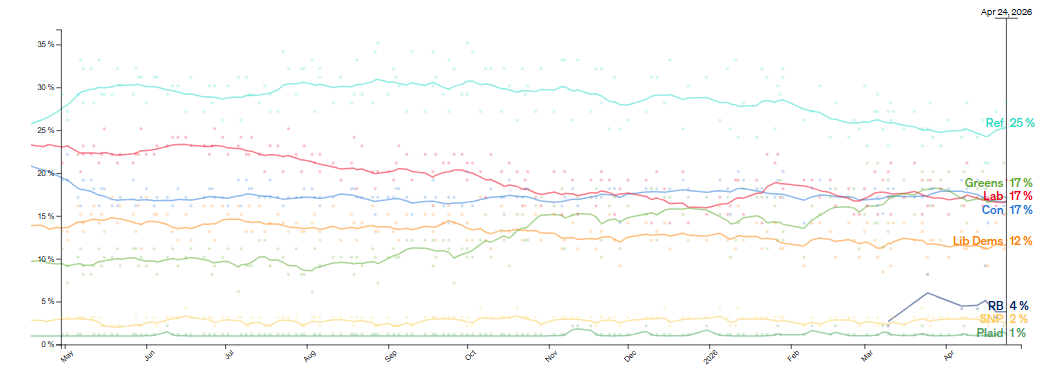

Figure 1: UK Opinion Polls Suggest Two-Party System Already Dead

Source: Politico, Voting intentions, poll of polls

The biggest set of elections since the 2024 general election will see millions of UK voters head to the polls on 7 May. Voters in Scotland and Wales will elect representatives to their two respective national parliaments, while a wide number of local council and mayoral polls will take place in England, with major ones occurring in Greater London. But especially with voter turnout likely to be an issue, the results look to be inconclusive, if not very much so. As Figure 1 shows, there are four parties now running close together at under 20% in opinion polls, albeit running a little behind the right-wing Reform Party, but where the latter has lost much support given its previous very explicit support for the U.S president who is increasingly unpopular in the UK.

As for unpopularity, this is just as much a problem for the current Labour government and especially its leader (and thus PM) Keir Starmer. Labour was the clear beneficiary of the electoral system when it won power in July 2024, with just 33% of the popular vote, but still amassed a commanding parliamentary majority of 174 seats. The clear losers then were the previous Conservative administration which lost almost 20% of the voters that it won in the 2029 general election. And a similar fate seems to be looming for Labour given the opinion polls. The question is how severe the damage would need to be in order for Labour to either/both change leader and veer more to left and dilute the fiscal produce priority of the current Chancellor Reeves. This is clearly worrying markets, already troubled by the current UK political scandal regarding the choice of UK ambassador to the U.S. which are making markets think twice about the current administration’s ability to run government anything like smoothly. This risk cannot be downplayed, but while more immediate, it is not the only one markets may have to consider.

The local elections to be held in England will be run on the usual first-past-the post system, which disproportionally rewards whoever wins the most votes – NB the 2024 Labour election victory was achieved with the lowest vote share of any governing party in UK history winning 63% if seats with 33% vote share. But given the low poll ratings of the all the parties, this points to a high likelihood that many of the local authorities up for re-election may see no overall majority for any party, thereby making coalition forming vital. This is nothing new to English local authorities, but the question is very wide differences on policies, coalition forming may be very difficult with so many disparate parties involved rather than the usual 2-3. But to markets it maybe a worrying foretaste of what is to come when the next general election occurs, with it likely that a) no one party comes anywhere near winning a parliamentary majority; b) politics and proposed policies become both polarized and over-promised and c) voter dissatisfaction may be evident in a clear drop in turnout All which points to what may be unprecedented policy instability after the next general election, as coalition forming will be difficult both in terms of form and duration, meaning policy making will hit a marled impasse. This deadlock made all the more undesirable as current fiscal problems are unlikely to be resolved – NB the ONS has just pared back population estimates that will worsen the fiscal picture.

But there is further risk to consider which, while possibly effectively small, is far from miniscule. The issue of independence for Scotland and even Wales may resurface as both countries face elections to their respective devolved parliaments on May 7. Indeed, polls see the Scottish National Party, in power since 2007, winning a fifth consecutive term while, in Wales, Plaid Cymru is vying with Reform to become the biggest party in the Welsh Senedd, which would break Labour’s control for the first time since devolution in 1999. Admittedly, while the SNP may win a fresh majority it may lose enough seats so as to garner no added momentum for the independence referendum is trying to justify which is in any case hardly popular among the electorate. Meanwhile in Wales Plaid promises no referendum on independence during any first four-year term it wins, but instead will set up committees to bring such a referendum nearer than otherwise.

There is a saying that good things come in threes. That is the absolute opposite of the current UK political outlook!