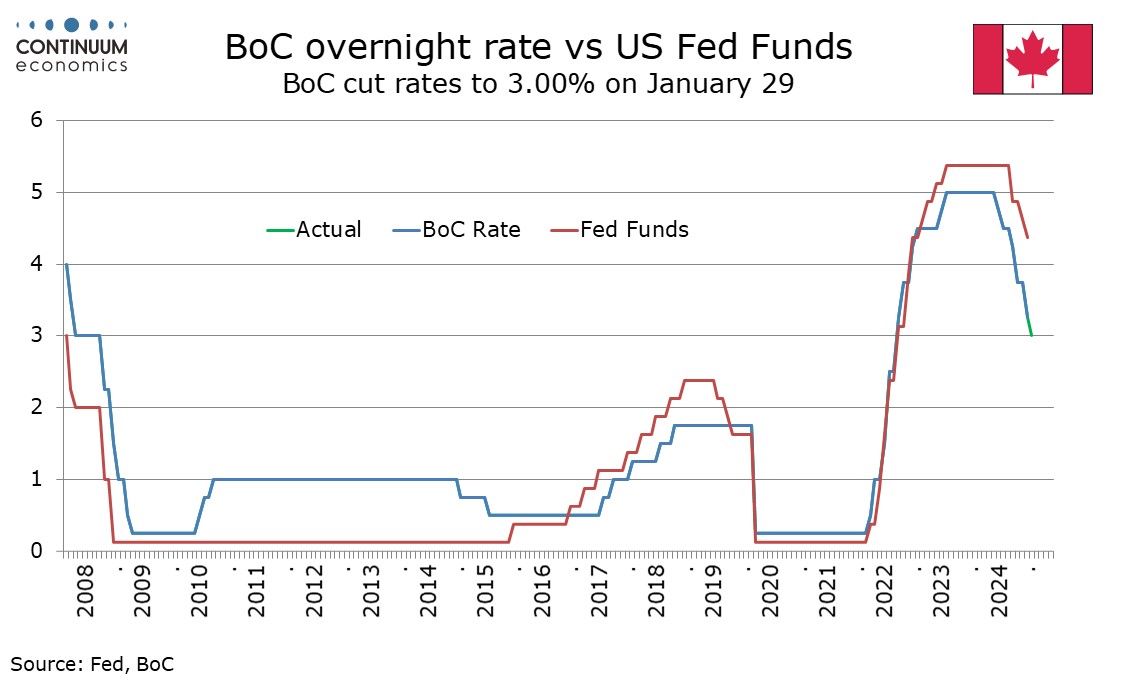

Bank of Canada eases by 25bps as expected, sees balanced risks if a trade war can be avoided

The Bank of Canada eased by 25bps to 3.0% as expected, and confirmed the ending of Quantitative Tightening, as had been outlined by Deputy Governor Toni Gravelle on January 16. The BoC has delivered some fairly optimistic forecasts, but these are made assuming an absence of tariffs, given that the BoC sees the scope and duration of a possible trade conflict as impossible to predict.

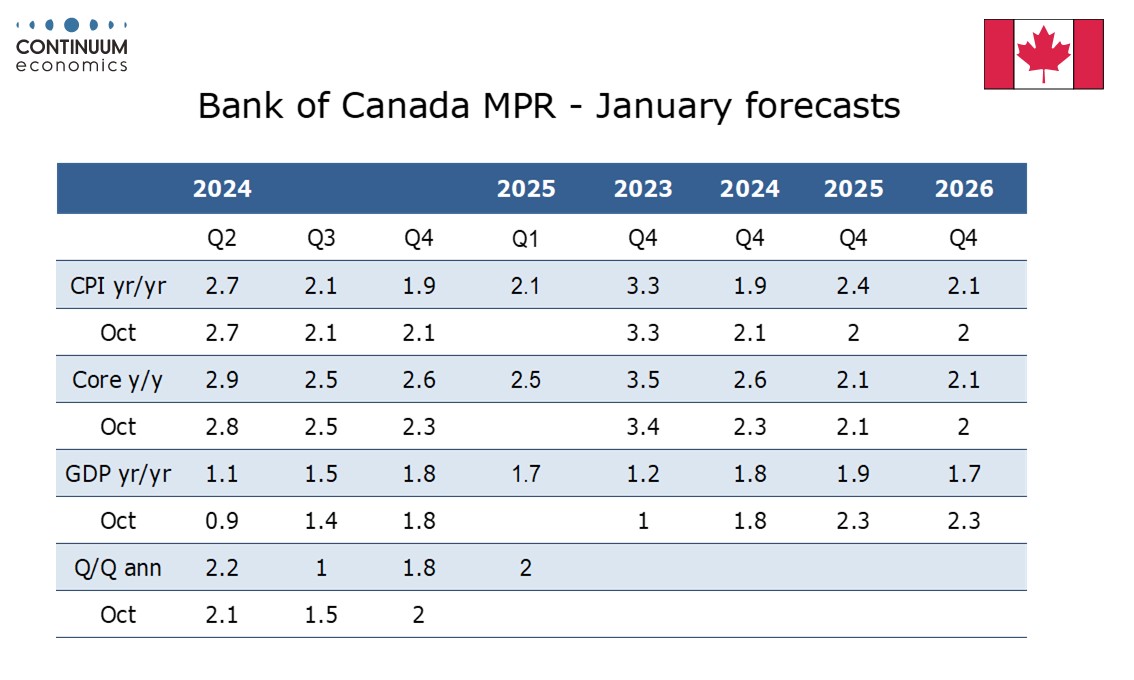

Compared to October, the Bank of Canada’s CPI forecasts have been revised marginally higher. The picture is still seen remaining close to the 2.0% target, though the core rate is seen at 2.1% in Q4 of both 2025 and 2026. Current slippage in headline CPI is exaggerated by a temporary sales tax holiday which will lift yr/yr comparisons in 12 months’ time. GDP growth for 2025 and 2026 has been revised lower, but this is based on lower expected population growth given reduced immigration. This has seen potential growth revised lower too, and excess supply is seen being gradually absorbed during the projection horizon.

Risks are seen as reasonably balanced setting aside threatened US tariffs, though a protracted trade conflict is seen as likely to lead to weaker GDP and higher prices, which Governor Tiff Macklem stated cannot both be leant against simultaneously. Macklem noted signs of past rate cuts starting to boost activity but in this he noted consumer spending and housing, while noting weakness in business investment, though that is forecast to increase gradually. Despite the threat of tariffs, new capacity for oil and gas is supportive for exports.

While balanced risk in the absence of tariffs, and risks on both sides should a protracted trade war be seen, imply a cautious approach to policy going forward, we are not ready to revise our view that the BoC will deliver two more 25bps easing this year, in March and Q2. Macklem in his press conference expressed a desire to get the economy on as solid a possible footing before it faces any tariffs. Improving activity is not going to eliminate excess supply quickly, and while employment is showing signs of picking up, the BoC’s statement also noted signs of previously sticky wage pressures showing signs of easing.

A protracted trade war would almost certainly push the Canadian economy into recession, and if so, that should ensure that the price hikes emerging from any Canadian retaliation against US imports would not become entrenched into a sustained rise in inflation. Trump backed off a threat to impose tariffs on Canada on day one of his presidency but recently threatened to impose them on February 1. We expect that he will not do so on that day, but the threat is likely to be a concern for some time, and that is likely to weigh on activity, particularly business investment.