China: Yuan Appreciation; U.S. 301 Threat and 4.5-5.0% GDP Growth for 2026?

• The Yuan has continued to appreciate with no resistance from China authorities. Part of this is a willingness to allow a modest Yuan appreciation in the face of the huge China trade surplus and pressure from U.S./Europe/IMF and others over an undervalued Yuan, but appreciation is also designed to soften U.S. trade pressures and the risk of an aggressive section 301 action from the U.S. China also wants the trade truce to continue, but is reluctant to deliver Trump’s desired trade deal with China. This could make a 5% growth target difficult to achieve and it is possible that China goes for a 4.5-5.0% 2026 GDP target. • For the Yuan this all likely means that China is happy to allow modest further Yuan appreciation to 6.70 in 2026, but not 6.40-6.50 that would undermine the competitive edge from the decline in the real Yuan over the last few years.

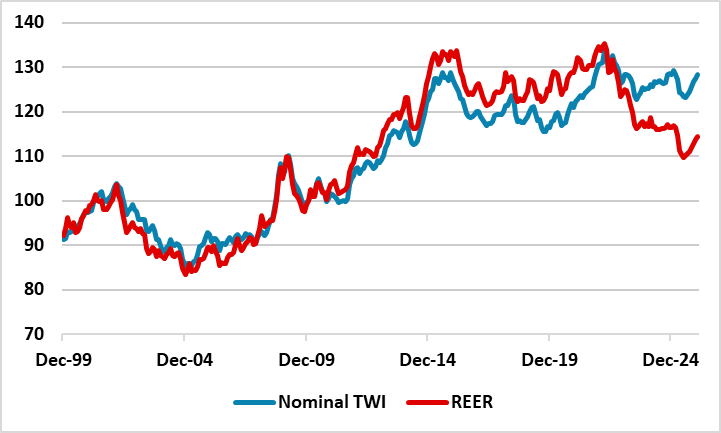

Figure 1: Yuan Nominal and Real Effective Exchange Rate (%)

Source: Datastream/Continuum Economics

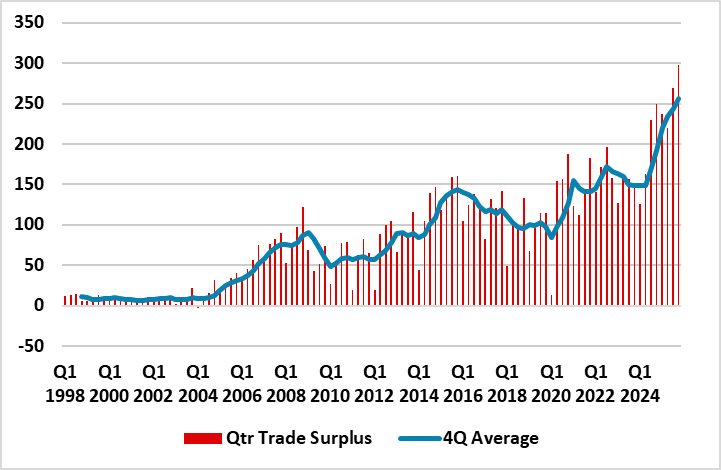

Net exports really helped China growth in 2025, but this is unlikely to be repeated on the same scale in 2026. Key points to note.

• Yuan appreciation and section 301 threat. The Yuan has continued to appreciate after the end of the China new year holidays, with little complaint yet from China’s authorities. Part of this is a willingness to allow a modest Yuan appreciation in the face of the huge China trade surplus and pressure from U.S./Europe/IMF and others over an undervalued Yuan (falling export prices means that the Yuan has depreciated in real terms in the last few years, see Figure 1). Part of this willingness to allow appreciation is also designed to soften U.S. trade pressures and the risk of an aggressive section 301 action from the U.S. The U.S. Supreme court rejection of reciprocal and fentanyl tariffs lower the effective tariff rate that China faces, even if the section 122 rate is increased from 10% to 15% for certain countries (i.e. China) as USTR Greer noted last week. The risks of permanent and higher section 301 are now higher in 5 month’s time after the Supreme court rejection, when the investigations are complete and Trump makes a decision in July. This means that China needs to give some ground to the U.S. to avoid worst case outcomes from section 301 and keep the existing trade truce.

• Trade truce continues but no U.S./China trade deal. China wants the trade truce with the U.S. reconfirmed with the President Xi and Trump summit in China on March 31. However, China is not keen on a formal trade deal that could incorporate numerical targets to reduce the bilateral trade surplus on a multi-year basis. Better to keep a semi-permanent trade truce. Thus the preference is to keep the U.S. in negotiations and hope that section 301 tariffs are not draconian. Appealing to Trump ego through the visit to China is one way, but modest Yuan appreciation is a 2nd tool for China.

Figure 2: China Quarterly Goods Surplus (USD Blns)

Source: Datastream/Continuum Economics

Source: Datastream/Continuum Economics

• 4.5-5.0% 2026 growth target. How much China is willing to allow the Yuan to appreciate against the USD is not currently clear, as the Yuan real depreciation could allow lots of room (Figure 1). Previously Yuan appreciation has occurred in a stepwise fashion. A 2.5-5% appreciation followed by smoothing FX intervention to allow the Yuan to consolidate followed by further appreciation. Some have also focused on the extra line recently added to President Xi Jinping's 2024 speech that the yuan should be widely used in global trade, investment, FX markets, and more importantly, have the status of a global reserve currency. Some argue that this could mean China authorities are happy to allow a larger and more persistent Yuan appreciation. We are less sure, as this is a long-term multi year goal rather than for 2026, as capital flow restrictions remain. Additionally, we do not feel that total fiscal stimulation to be announced at the NPC meeting starting on March 5 will be more than Yuan2.5trn for 2026, with only modest cyclical and structural measures to boost consumption (see our views here) and no accelerated bailout for residential property as the IMF has suggested (see our view here). From a growth viewpoint, this also suggest that China could struggle to hit 5% real GDP growth in 2026. One way to meet this dilemma is to accept a lower 4.5-5.0% target for 2026. We will see what is announced during the NPC starting on March 5. For the Yuan this all likely means that China is happy to allow Yuan appreciation to 6.70 in 2026, but not 6.40-6.50 that would undermine the competitive edge from the decline in the real Yuan over the last few years.