Sweden Riksbank Review: Nearing the End?

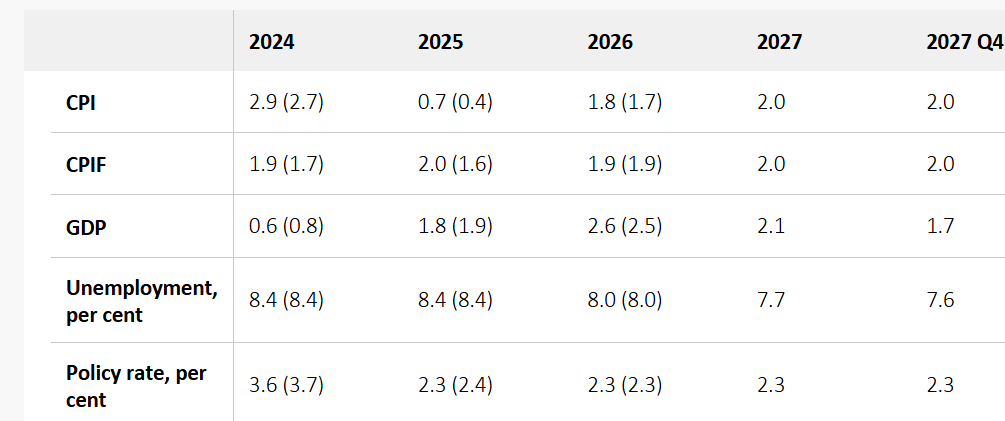

As widely expected, a fifth successive rate cut was seen at this December Riksbank meeting, but back to a 25 bp move rather than the 50 bp cut last time around (to 2.5% vs the 4% peak seen up until last May). But it was the updated projections (Figure 1) that was be the main news, not least given data of late that has been on the high side of expectations, including a small recovery in GDP and CPIF data well above Riksbank thinking. In this regard, the Riksbank did revise down its slightly above-consensus GDP outlook out to 2027, whilst still suggesting inflation will settle around target. Perhaps the question was whether a lower terminal policy rate was considered, but this does not seem to be the case with one more 25 bp reduction penciled in for H1 next year and then with the ensuing policy rate staying there out to 2027.

Figure 1: Inflation to Settle Around Target?

Source: Riksbank forecasts from Dec 24 Monetary Policy Report

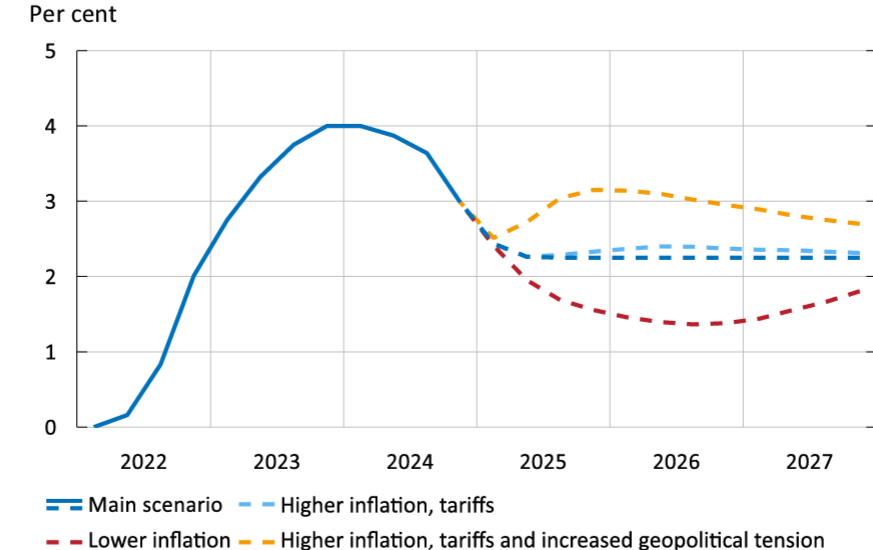

But amid downside growth risks and realties through Europe, we still see the policy rate troughing at 2.0% by mid-2025, but still well within the range that the Riksbank has for its’s terminal rate estimate. But deeper cuts are possible as even the Riksbank acknowledges (Figure 2), albeit with policy reverting back to the baseline ultimately.

Riksbank thinking is very much affected by uncertainty, both regarding the outlook for inflation and economic activity. There are several factors that could lead to a different economic development and monetary policy than those reflected in the Riksbank’s forecast. There is particular uncertainty regarding developments abroad, for instance with regard to the geopolitical tensions, lack of clarity regarding trade policy and the governmental crises arising in Europe. There are also risks linked to the recovery in the Swedish economy and the krona exchange rate. New information, and how it is expected to affect the outlook for the economy and inflation, will be decisive in determining how monetary policy is formulated.

Admittedly, the inflation surprises have been concentrated in energy and result of the EU’s new electricity directive which has caused a sharp increase in electricity prices in Sweden since its introduction in late October, this probably explaining the upgrade to the 2025 CPIF outlook. But even inflation ex energy has started to flatten out although the CPI measures on the basis is still consistent with target having already been met. Even so, the prices outlook inflation certainly for the next year has become a little more uncertain.

Policy Front-Loading?

Since the spring, it has been very much a question of how fast, not if, as far as policy easing was concerned for the Riksbank, with policy thinking having been markedly reshaped this year. From the Board’s perspective, by initiating easing relatively early in May, it was both reacting to weak data (both real and price wise), but more notably in giving itself flexibility to pursue what it then thought needed to be a gradualist approach to further easing. That now has changed and increasingly radically with policy put into a faster gear to front-load, both a result of an undershoot of inflation (partly energy related but ever clearer in terms of short-run dynamics) but as suggested above increasingly due to a still weak economy which has failed to grow on balance since end-2021, albeit with clear quarter-to-quarter volatility.

But policy has been eased rapidly and monetary policy affects the economy with a lag. From the Riksbank’s perspective, this argues for a more tentative approach when monetary policy is formulated going forward. The Riksbank will therefore carefully evaluate the need for future interest rate adjustments; if the outlook remains unchanged, the policy rate may be cut once again during the first half of 2025.

Figure 2: Alternative Official Policy Outlooks

Source: Riksbank

Terminal Rate Scenarios

The question is, if growth disappoints into 2025, will the Riksbank ease further than this final 25 bp move it is now flagging. This is entirely possible and is now a view we encompass to some degree – indeed, the Riksbank scenario analysis suggests that the policy rate could drop below 2%, at least temporarily (Figure 2). Supposedly, this would have to be a result of the weaker growth backdrop accentuating disinflation, this all the more likely given that we think is an optimistic 1.8% 2025 GDP outlook, turning out nearer 1%.

But other factors may come into play, not least policy moves elsewhere which may result in a greater and unwanted appreciation of the currency than currently envisaged by the Riksbank. A further factor may be the Riksbank’s view of neutral rates. Recent analysis from Deputy Governor Seim suggested that the long-term neutral interest rate, and thus the long-term normal policy rate, is probably between 1.5% and 3%, ie a full one percentage point lower than the range the Riksbank published in 2017 and view endorses by this updated Monetary Policy Report. All of which very much suggests downside risk to the Riksbank baseline policy outlook!