FX Daily Strategy: Asia, March 19th

BoE MPC Agree to Disagree

ECB No Longer in a Good Place

Swiss SNB Keeping a Low Profile

Sweden Riksbank On Hold and Still For Some Time Ahead

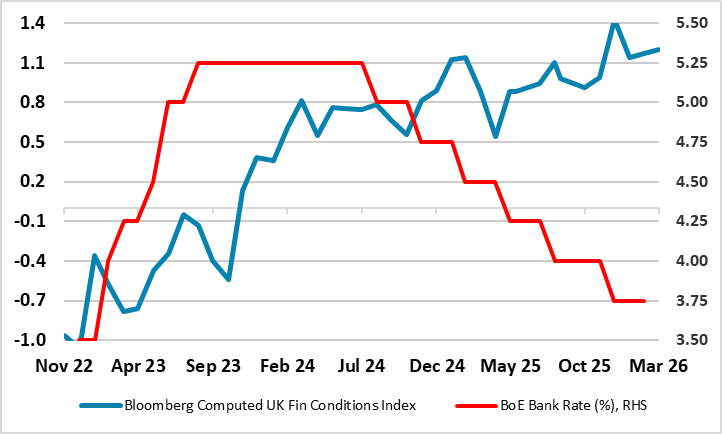

Figure: Bank Rate and Financial Conditions Diverge (% and level)

The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely this month. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a whole will not have to reveal too much about any shift in policy bias given that it does not have to provide updated forecasts until its April 30 meeting, the individual member views will show continued divides. Indeed, while February’s four dissenters will suggest they are probably deferring easing, some of the more hawkish members may be more open about considering hikes to guard against or combat any rise in inflation expectations that they think may trigger a fresh rise in wage pressures. We consider such thinking to be misplaced given the labor market is loosening and where companies face a fresh squeeze on profits. Given financial conditions, we still see at least two more 25 bp rate cuts ahead but now deferred to no sooner than late summer.

The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely this month. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a whole will not have to reveal too much about any shift in policy bias given that it does not have to provide updated forecasts until its April 30 meeting, the individual member views will show continued divides. Indeed, while February’s four dissenters will suggest they are probably deferring easing, some of the more hawkish members may be more open about considering hikes to guard against or combat any rise in inflation expectations that they think may trigger a fresh rise in wage pressures. We consider such thinking to be misplaced given the labor market is loosening and where companies face a fresh squeeze on profits. Given financial conditions, we still see at least two more 25 bp rate cuts ahead but now deferred to no sooner than late summer.

Indeed, we have long argued that the weak economy and labor market allied to tight(er) financial conditions would build the case for three 25 bp cuts in 2026 to 3.0%, the latter being a level that the dovish camp on the MPC would consider to be neutral. And a cut as soon as this month seemed very likely given that an easing was averted by just one vote within the nine-strong MPC in February, this partly reflecting downgraded GDP and inflation projections with the latter seen by the BOE falling to target by mid-year and largely staying there out to 2028.

Figure: ECB Projections in Perspective

With no change in policy expected, what the ECB says is the most important aspect of the ECB meeting next week, both explicitly and implicitly via its updated forecasts (Figure). Both are likely to underscore that rate hikes are certainly possible if the almost inevitable inflation rise proves to be either/both significant and/or persistent. But no time frames will be suggested, this papering over what are long-standing splits within the Council regrading policy. There will be some reassurance that market based inflation expectations have risen only modestly and more over the short-term than longer measures. But amid what we think has been ECB complacency and where there will be clear real economy damage from the current conflict and what we see as only a limited and temporary inflation spike, we still regard the next move in rates to be a further cut, though probably only one more 25 bp move later this year.

Like the ECB will do, we have identified four likely scenarios regarding the length and breadth of the Middle East conflict. But under our very much more likely view of limited further fighting we see oil and gas prices largely falling back to the pre-war levels within a year. This will still lead to a clear and fresh rise in inflation, mainly via the direct effects of the HICP measure having a 10% energy weighting but with some second round effects that will affect rates into 2027 (though where actual inflation at the end of next year may be lower than previously thought). This will be on account of the likely real economy damage from the conflict but also reflects our long-standing view that the Council has been complacent, downplaying what we regard are downside risks which may be materialising.

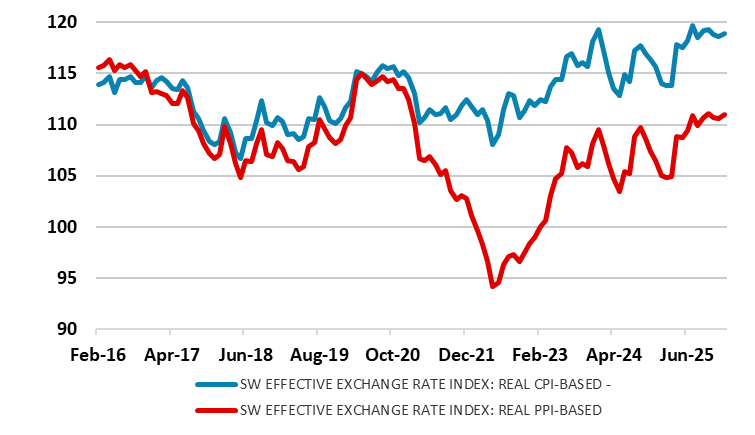

Figure: Two Alternative Impressions of Competitiveness?

Once again and in line with consensus thinking we see SNB policy being unchanged when it gives its next quarterly assessment with little shift in the forecast for either growth or inflation. Admittedly, the tone of the economic outlook will be more guarded but where it will be underscored that it is too soon to make material changes to the outlook given current heightened uncertainties. The strong Swiss Franc will be mentioned but its current strength needs context (Figure). Indeed, it will adhere to a medium-term inflation at 0.6% and a gloomy 2026 activity picture with projected GDP growth of around 1% masking the fact that the underlying picture is more sobering given the circa-0.25 ppt boost sports events will provide this year. But with inflation forecast to be within the confines of its target range of less than 2%, this will be enough to justify stable policy. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur.

Regardless, the increasing strength in the Swiss France is causing reverberations. More a reflection of U.S. dollar weakness than that of the euro, the nominal trade weighted Franc is hitting new highs. But while this strength in impairing competitiveness – vital to an economy where exports account for 75% of GDP – this is not the whole story despite what are increasing complaints from high profile Swiss companies. Instead we would argue that with the strong currency also reducing import and producer prices, Swiss companies are enjoying a clear reduction in their cost bases. Moreover, this is even allowing a rise in profit margins as falling costs contrast with CPI inflation currently around zero. This is important in assessing competitiveness too as compiling a real or inflation-adjusted effective exchange rate shows a far less sizeable appreciation when deflated by producer prices rather than those for the consumer (Figure).

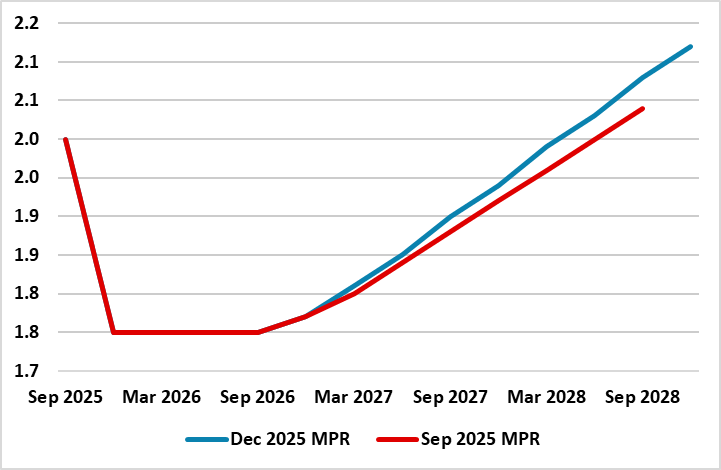

Figure: Riksbank Policy Outlook

It is highly likely that the Riksbank will (again) keep policy on hold with the key rate left at 1.75% when it gives its next verdict. However, what will be more important is what the Board says; explicitly in terms of the recent (less pleasing to it) data flow and, implicitly in terms of updated forecasts in the Monetary Policy Report (MPR). The latter may try and assess the impact of Middle East conflict, but tentatively. But the GDP and CPI outlooks may need to be pruned back after what have been unexpected weak readings for both of late, some of which may be attributable to the recent appreciation of the Krona. The inflation undershoot is modest but as we have suggested repeatedly, the 2.6% Riksbank GDP projection for the year is overly optimistic, possibly by a factor of two. As a result, the Board promise of no change for some time to come is likely to be repeated but with more discernible risks attached in both directions. Regardless, we still do not see any looming policy reversal, as we see this current policy rate (1.75%) staying in place through 2027, ie a little longer than the Riksbank.

There is a saying that one should be careful about what you wish for. In this regard, the Riksbank aspiration of a strong(er) currency and low inflation is being more than met. The currency has risen strongly and is certainly a key factor in the current on-going disinflation, with imported consumer goods actually negative in y/y terms (Figure 1). Regardless, the underlying picture is still very soft as smoothed adjusted m/m figures (not as prone to volatility via base effects) show most measures of core inflation are consistent with the inflation target or below. Even so, the inflation undershoot (relative to Riksbank thinking rather than the 2% target) is modest, with CPI-ATE ex energy at 1.4% in February, 0.3 ppt below the December Board projections.

But the real economy backdrop is still puzzling and meriting more of a reassessment for the Board. Despite an apparent 2%-plus GDP jump in the last three quarters if 2005 (twice Riksbank thinking), the economy still looks soggy, not least in the labor market and perhaps increasingly so. Moreover, business surveys are mixed to soft while the Riksbank will note the results of its own survey, which underscores that Swedish companies describe the economic situation as a long and protracted slump that has not improved since the spring and where industrial activity has weakened. In addition, many respondents wonder whether households will continue to be cautious about consumption for a longer period.