Sweden: Riksbank Needs to Revise Output Gap Estimate and Reassess Policy Outlook?

We are even more convinced that the Riksbank will cut further and as soon as the next Board verdict on Jun 18. Moreover, the Board may even then suggest that further moves are possible. This may seem stretched given that the Riksbank has virtually called a halt to the easing cycle, albeit most recently (May 8) suggesting downside risks to its inflation outlook might warrant a slight easing going forward. Our thinking has hitherto reflected both below par survey data (suggesting difficulties in predicting future business conditions) and better inflation outcomes. But this view has been bolstered by fresh GDP data that not only showed a surprise drop in Q1 but hefty downgrades to the 2024 backdrop. All of which suggest that the Riksbank may have to halve what we have for some time suggested was an optimistic 2.2% 2025 growth forecast and, as a result, may have to double its estimate of an output gap, this adding to downside inflation risks.

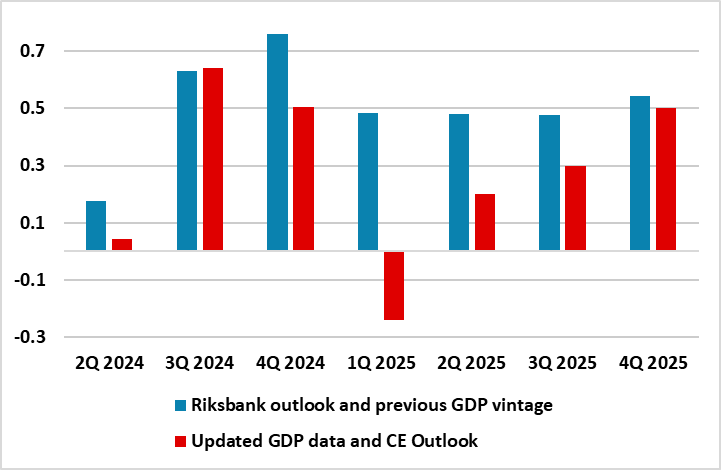

Figure 1: An Gloomier Backdrop and Outlook

Source; Stats Sweden, Riksbank and CE, figures are % chg q/q

A keynote speech next week from the Governor (Mon) and a parliamentary appearance (Tue) provide the Board with early opportunities to advertise any change in thinking. Admittedly, the Board may be coy about any such overt change of view given impending CPI data due next Thursday. There are risks that due to energy base effects the targeted CPIF measure may edge up a notch or two from April’s 2.3% but the ex-energy measure may drop decisively, albeit not fully back to the lows of late last year.

Regardless, the Riksbank bases policy on an assessment of the inflation outlook and the balance of risks associated with it. Surely an economy that may be more than a full ppt weaker than its existing thinking would suggest added downside price risks. This seems to be the case given the latest GDP update. Not only did this show an unexpected 0.2% q/q drop in Q1 but this came alongside cumulative downward revisions of around half a ppt for the previous three quarters (Figure 1). In perspective, the Riksbank had pencilled in a 0.5% Q1 rise, with this pace seen persisting for the rest of the year. But given the new base effects, even such a 0.5 q/q pace of growth would result in average 2025 growth of 1.2%, this very much at the bottom of most forecasts.

But we think an even softer profile is likely, both as trade tensions and uncertainties persist and given the manner that the jump in exports in Q1 may reverse as it was likely based on anticipating U.S tariffs being imposed from Q2 onwards. As for the tariff threat, it is noteworthy how important the U.S is to Sweden. As a Riksbank research paper notes - the Swedish economy is closely linked to the United States, both directly and through global value chains, and Swedish exports to the United States have increased in recent years. The United States is Sweden's third largest destination for exports of goods with goods export based around tariff threatened motor vehicles, pharmaceuticals and machinery

Indeed, on the basis of the updated GDP backdrop, we have revised our 2025 growth rate to just 1% (from 1.5%). The Riksbank may not follow this fully when it updates its own projections next month, but it will have to pare back significantly its above consensus and what we have form time suggested was an optimistic 2.2% projection for the current year to somewhat well below its estimate of current potential (ie 1.8%). As a result, rather than suggesting that Sweden’s output gap may shrink from 1.4% of GDP in 2024 to around 1% this year, it may have to point to a gap nearer 2%. To us, this very much necessitates a fresh assessment of the inflation outlook and risks that we think will occur next month, this justifying a fresh 25 rate cut on June 18 and the flagging of possible further moves beyond!