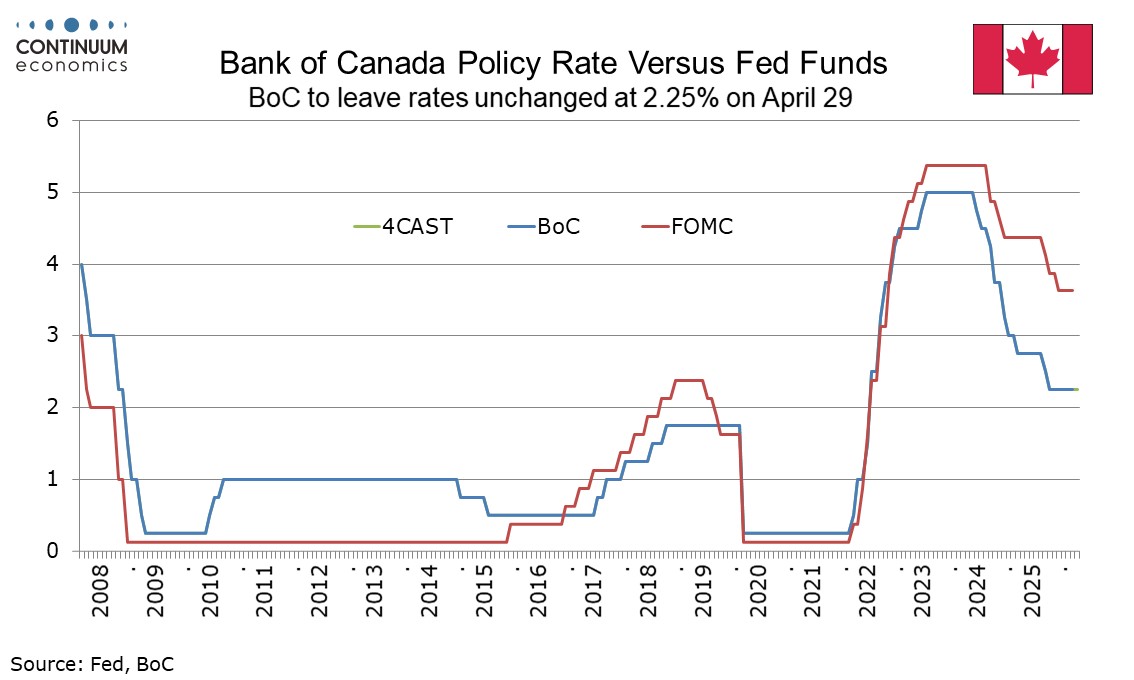

Bank of Canada Preview for April 29: No hawkish shift from energy price shock

The Bank of Canada meets on April 29 and looks set to leave rates unchanged at 2.25%. A quarterly Monetary Policy Report is due but given uncertainty the BoC may deliver a range of scenarios rather than an updated forecast. Despite the upside risks to overall inflation, recent subdued economic activity and core inflation data suggests the BoC will not delver a more hawkish tone.

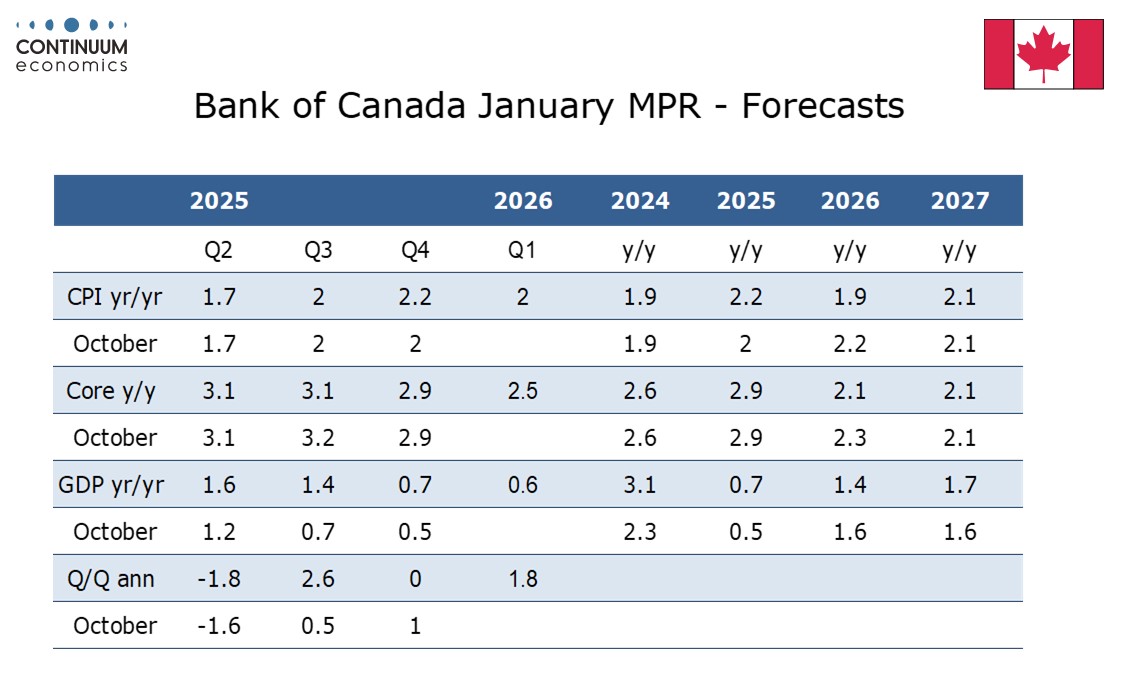

In its last Monetary Policy Report in January the BoC looked for 1.8% annualized GDP growth in Q1. The statement at the last meeting on March 18 suggested near term growth would be weaker than expected in January, though we do not expect a sharp underperformance of the BoC’s forecast. Q4 GDP at -0.6% annualized was weaker than a flat BoC projection but the BoC in March noted this was largely on an inventory drawdown. The March statement also noted weak January and February employment data, which was followed by only a marginal correction higher in March. We expect the BoC will look for a subdued Q2 GDP gain of around 1.0% but its January forecast of 1.4% Q4/Q4 does not appear to require a significant downgrade. The growth implications of the energy shock are mixed for Canada, with the energy sector likely to see a boost.

CPI in Q1 averaged 2.2% yr/yr, above a 2.0% January projection, but core inflation, measured by the average of CPI-Median and CPI-Trim, at 2.3% was softer than a 2.5% January projection and recent monthly data is consistent with a return to the 2.0% target. Overall CPI will get a lift in Q2, both from the recent rise in energy prices and the abolition of a carbon tax in April 2025 lowering the base. CPI is likely to rise to around 2.6% in Q2 and may well remain above target through 2026.

Still, falling core inflation and a subdued GDP and employment picture does not suggest any need for the BoC to make a hawkish shift in response to the energy shock. They will monitor inflation expectations for signs that the energy shock will feed into broader inflation but the subdued economic picture is likely to keep this limited. The upcoming review of the Canada-US-Mexico trade agreement is a further major source of uncertainty. The BoC statement is likely to reiterate that they are ready to respond as needed, without giving any signals on the timing and direction of the next move. We expect policy to be left unchanged through 2026, before being nudged up to 2.75%, the midpoint of the BoC’s 2.25-3.25% neutral range, in 2027.