U.S. Initial Claims low, Philly Fed stronger, but full impact of energy shock still to be felt

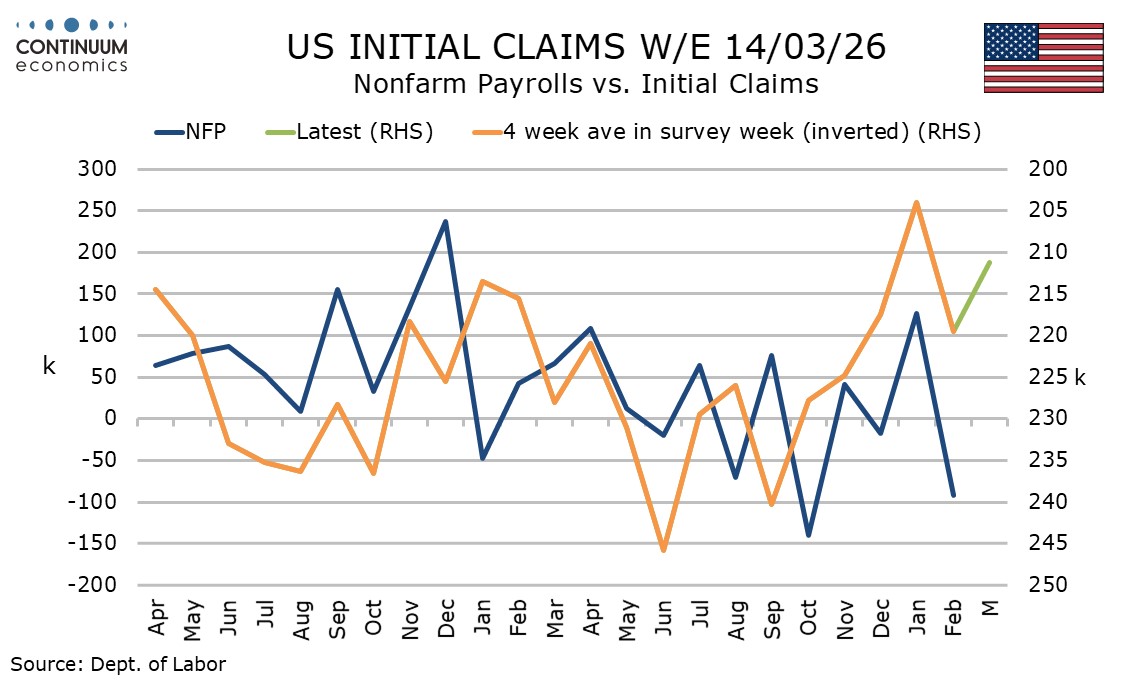

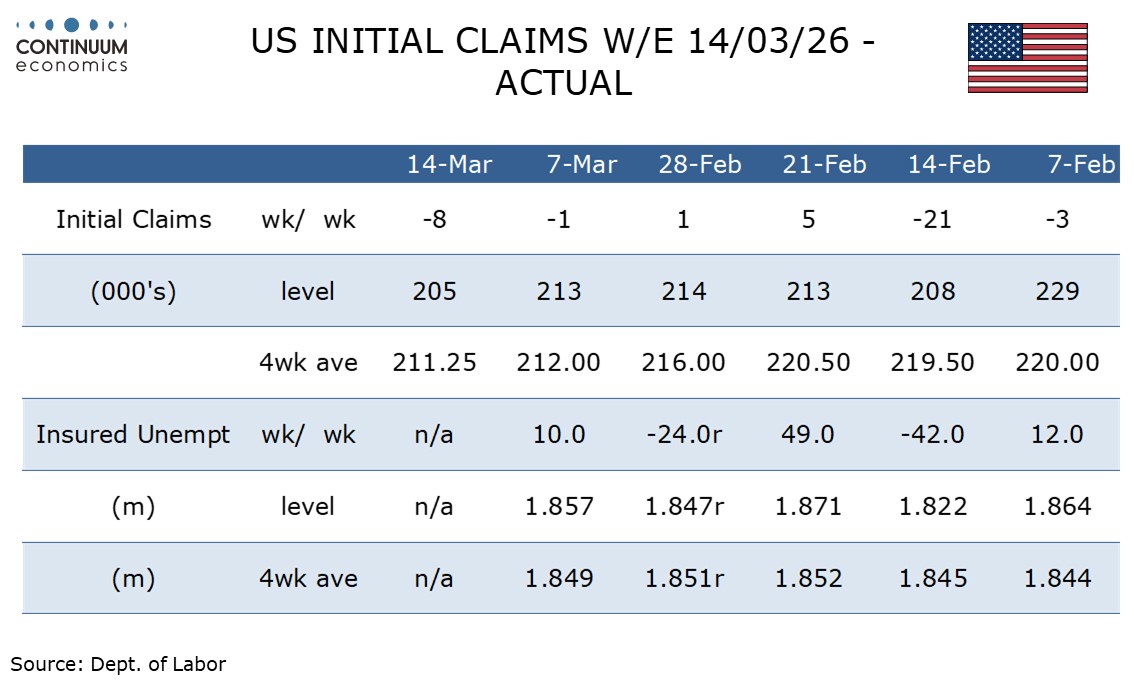

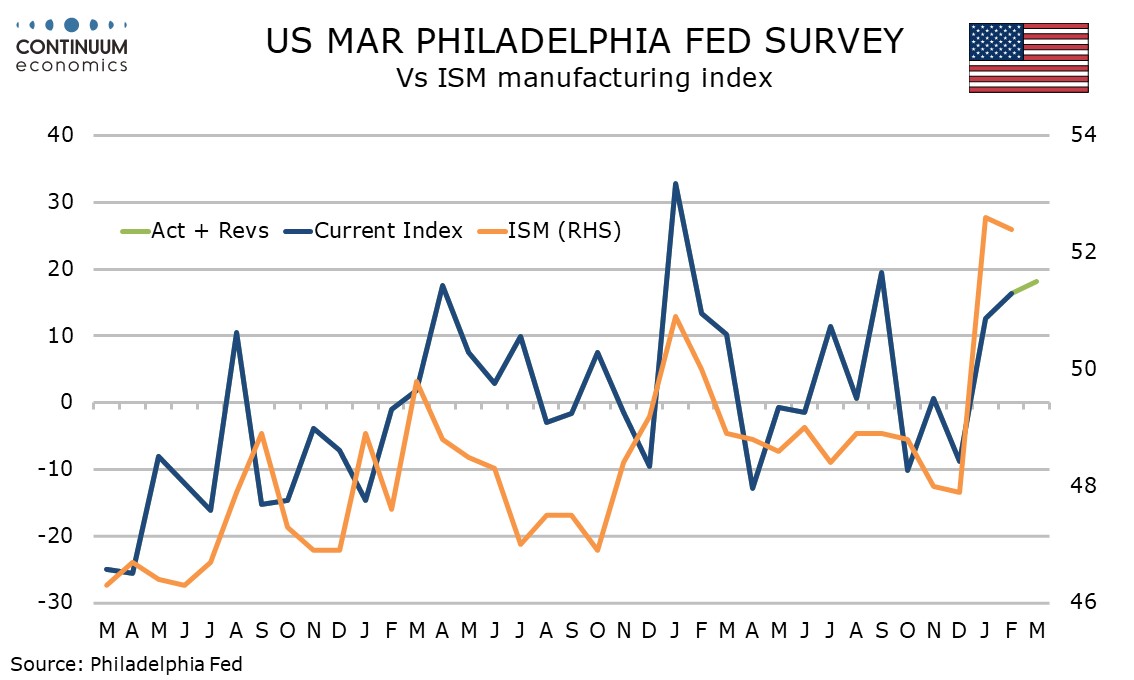

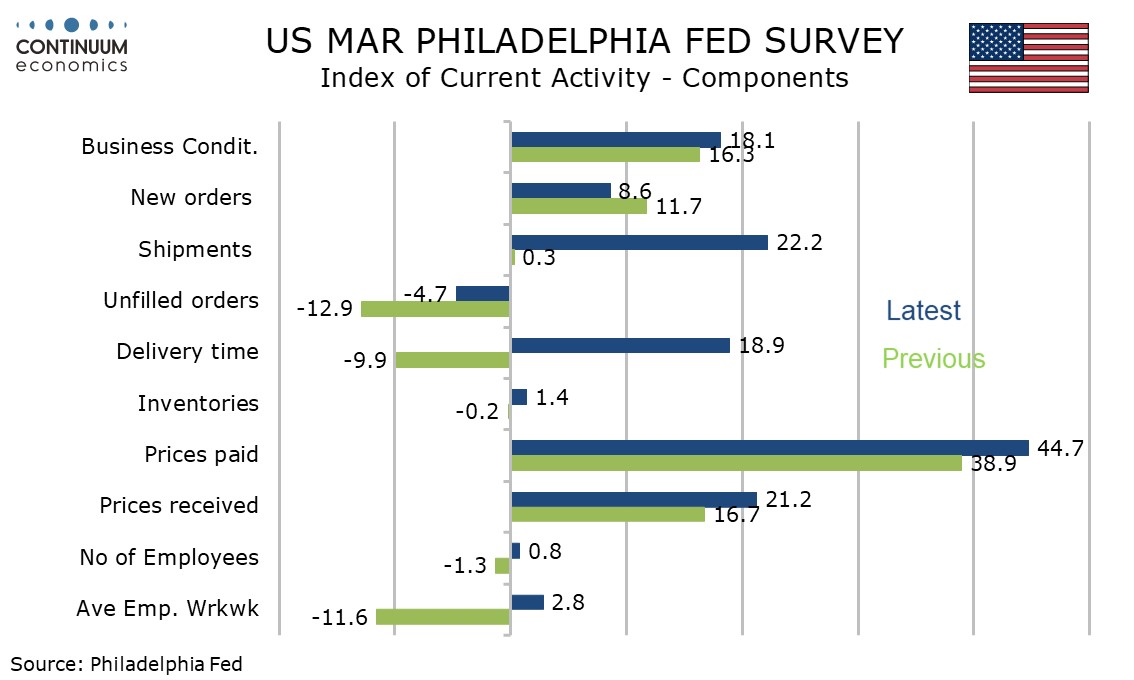

The latest US data is stronger than expected, initial claims at 205k from 213k reaching a 9-week low in the survey week for March’s non-farm payroll, and March’s Philly Fed manufacturing index of 18.1 from 16.3 at a 6-month high. The full impact of the Middle East conflict however is however yet to be felt.

The latest initial claims data puts the 4-week average at 211,25k, down from 219.5k in February’s payroll survey week but up from 204k in January’s. This suggests a stronger payroll than in February but not as strong as in January.

Continued claims cover the week before initial claims and saw a modest 10k rise to 1.857m after a preceding 24k decline. The 4-week average, which had been declining into late January, has been stable near 1.85m since then.

March’s Philly Fed index is the strongest of three straight positives and contrasts a dip below neutral in the Empire State index which came after two straight strong readings. The Philly Fed reading implies rennet strength in the ISM manufacturing index will be sustained.

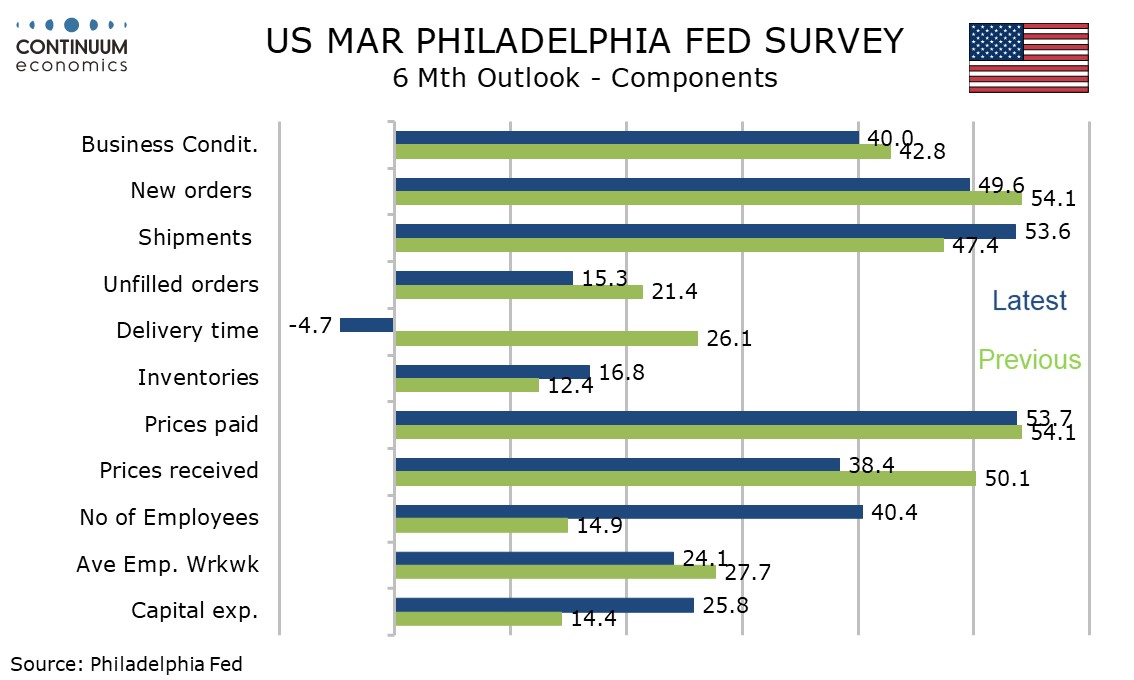

Details were mixed with new orders at 8.6 from 11.7, but employment and the workweek turning positive after negative February readings. 6-month expectations remain firm at 40.0 if down from 42.8, but this probably assumes a quick resolution to the Middle East conflict.

Price induces, both paid and received, are marginally firmer on a one month basis but remain above January levels, suggesting the impact of higher energy prices has not been captured. 6-month price expectations are actually lower, the 6-month view on prices paid at a 12-month low of 53.7 and the 6-month view of prices received at 38.4 the lowest since September 2024. This at least suggests that before the oil spike, price pressures were slowing, perhaps helped by the Supreme Court tariff ruling.