FX Daily Strategy: Asia, April 14th

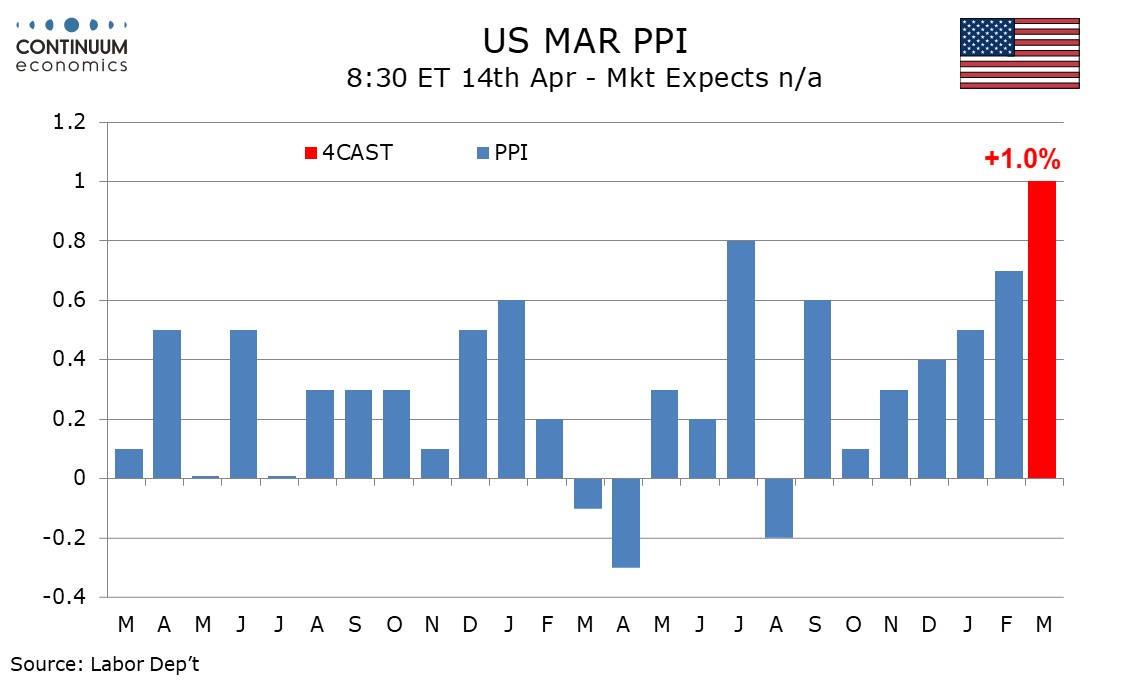

U.S. PPI Strongest since March 2022

Quiet Calendar Sees Focus Remain Geopolitical

DXY Broadly Consolidating

We expect PPI to rise by 1.0% in March, which would be the strongest rise since March 2022. The rise will be led by energy, though the core rates ex food and energy at 0.5% and ex food, energy and trade at 0.4% are likely to maintain a recent acceleration. We expect a strong 10.0% increase in energy even if price gains late in March are not fully captured. We expect a 0.8% increase in food to follow a strong 2.4% increase in February that reversed weakness seen in Q4 and January. The situation in the Middle East poses upside risks for food as fertilizer supplies are disrupted but impact in March is likely to be limited.

March 2022 after the Russian invasion of Ukraine saw some acceleration in core PPI suggesting upside risk in series that have already been showing worrying signs of acceleration in January and February. We expect PPI ex food and energy to rise by 0.5%, matching gains seen in December and February but slower than January’s 0.8%, while ex food, energy and trade rises by 0.4%, slower than February’s 0.5% but matching January. We expect goods ex food and energy to rise by 0.4% and services to rise by 0.6%, the latter led by transport and warehousing.

Figure: Core Inflation Estimates (%)

The Fed on April 29/ECB on April 30/BOE on April 30 will be of great interest for further guidance on central bank thinking. By these dates it should also be clearer whether the Iran war over or still exchanging isolated fire with Strait of Hormuz blockade.

We still pencil in 50bps of cuts from the Fed before end 2026 (though this is a close call after the good March employment report (here) and 25bps cuts from the ECB and BOE, due to the softer underlying economic conditions. Other economists are putting forward similar caution, with the OECD baseline forecasts based on March 20 oil and natural gas prices showing little to modest 2nd round effects.

The greenback will remain the backbone of FX market volatility. Geopolitical tension has driven market participant bid/offer the USD whenever the wind change. It will difficult to gauge the next leg as the fog of war persists. However, it looks to be more room for de-escalation than re-escalation in the current picture.

On the chart, prices extend cautious trade beneath resistance at congestion around 99.00 and the 99.18 high of 8 April. Intraday studies are rising and oversold daily stochastics are flattening, suggesting room for a retest of this range. But the negative daily Tension Indicator and unwinding overbought weekly stochastics should limit any break in renewed selling interest towards congestion resistance at 99.50. Following cautious trade, fresh losses are looked for. However, a close below support at the 98.70 Fibonacci retracement is needed to add weight to sentiment and extend late-March losses below 98.50 towards 98.00/10.