FX Weekly Strategy: APAC, May 18th-22nd

Dollar squeeze could continue near-term

Popular trades forced into some profit-taking

Stretched risk trades face potential increased volatility

Strategy for the week ahead

We’ve been discussing in recent outlooks how a few tensions that have been building up seem to be coming to a head, gaining some traction in FX by the end of last week. In no particular order these included:

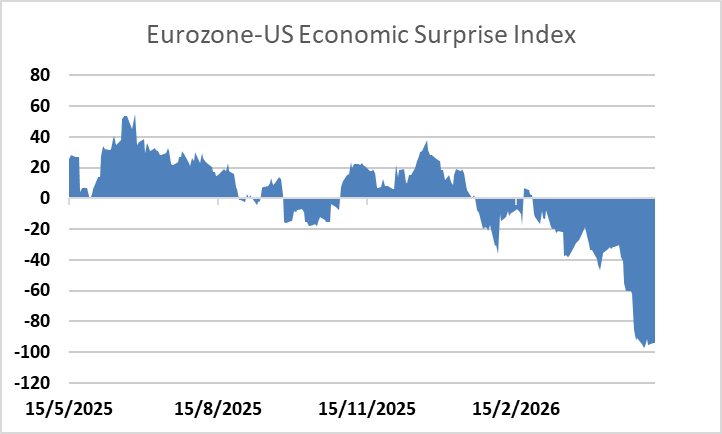

1) US outperformance versus the Europe that hadn’t been seeing much FX reflection, until now, owing to the perceived divergent central bank reaction functions (incoming “rate dove” Warsh vs ECB’s greater propensity to be inflation reactive).

That is divergence is starting to bend now, with US yields stretching through the big figure yield highs across the curve, and with spread pullbacks one factor playing to the initial dollar turn. While data is not the main focus this week, we could still see the respective PMIs reinforce this US outperformance theme. In addition, we would also keep a close eye on the MOVE index to see if the tests of critical stress levels on US (and other major) yields start to see a push higher in bond volatility, which in turn can amplify broader risk aversion.

2) Tension 2 revolved around the view that, given the unresolved geopolitical backdrop, the market was still looking quite light on dollar positioning. And more importantly, with the medium-term negative dollar narrative still prevailing, a firmer dollar was the ‘inconvenient trade’ the market was most vulnerable to near-term.

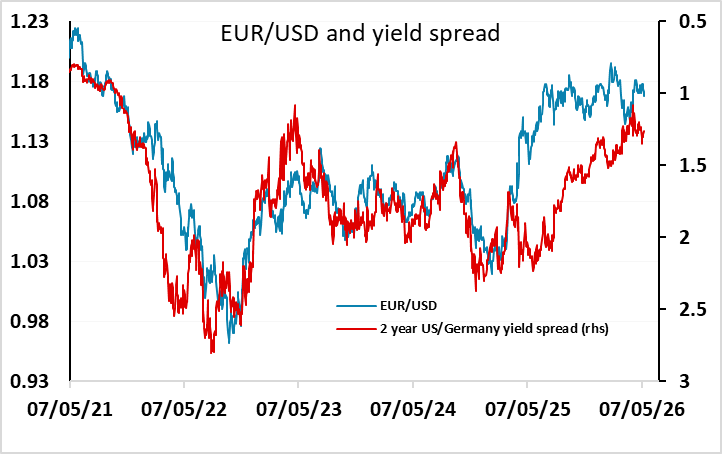

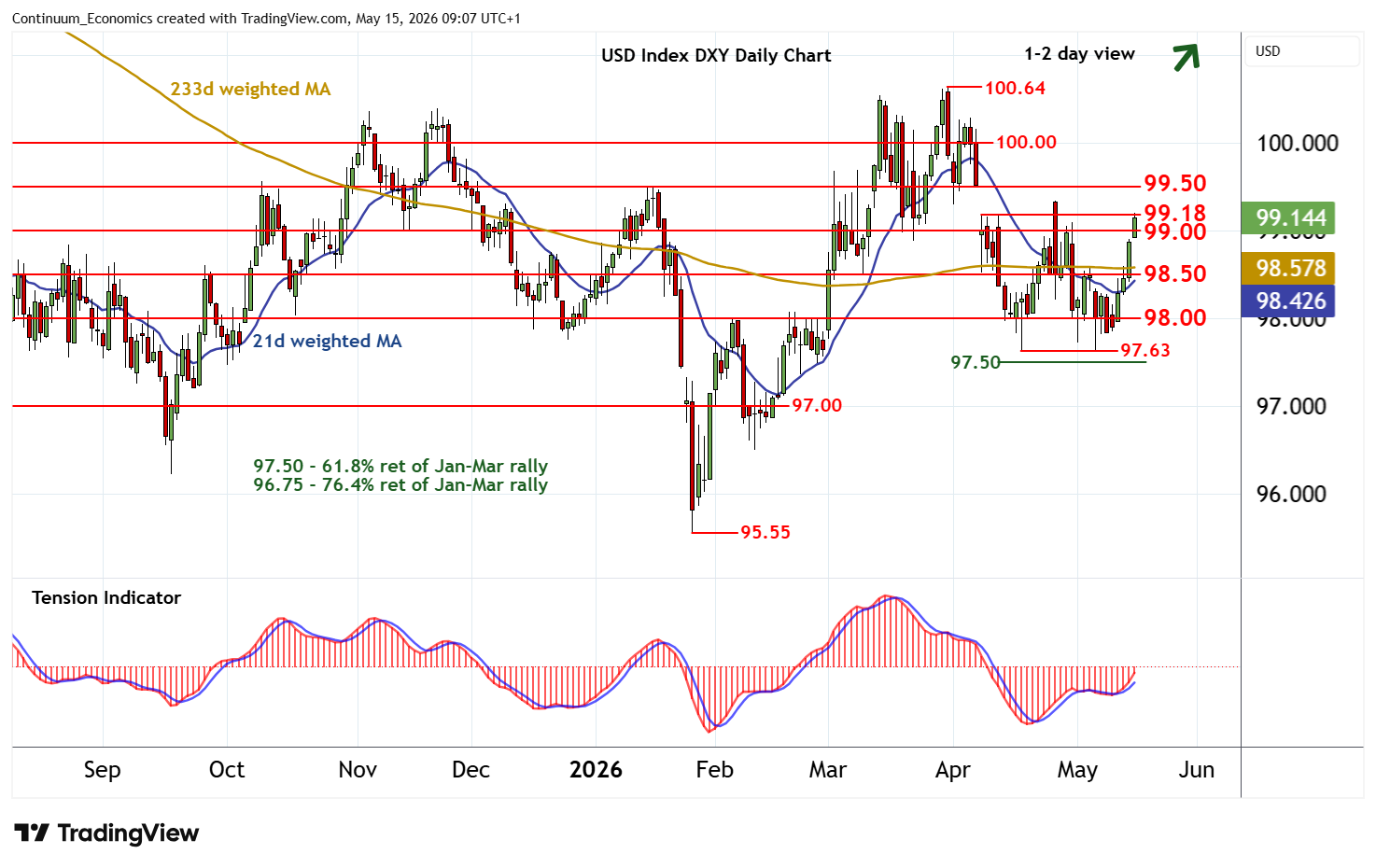

Level breaks at the end of last week could see some further follow through, with DXY potentially having scope back towards the 100~ wider range highs as a short-term move, as the market is caught the wrong way. EUR/USD has half point references down in range from here, starting with 1.16 next support reference, as the technical setup deteriorates.

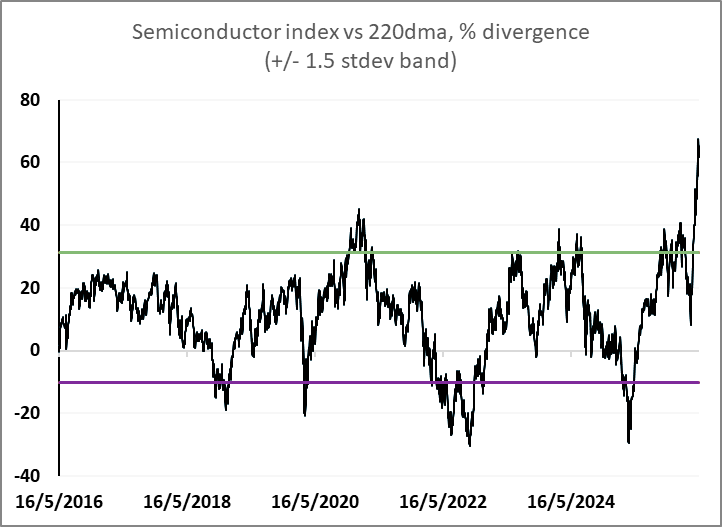

3) Tension 3 clusters around some fairly heated risk accelerations driven by the AI build out complex (metals, semiconductors and so on). While these ‘excess accelerations’ to trend were not all at maximum extreme by historical standards, many were pretty extreme and especially so when set against the broader macro and market outlook. Options dynamics fed into the suppressed volatility on these huge moves, so any turn when it comes could be sudden if that action reverses.

Nvidia are among the earnings reporters this week and will be watched closely for performance here, having caught up swiftly in recent days after underperforming the sector. Any sell the fact or spike-reversals out of the expected strong report might trigger a scramble more profit-taking, but you clearly cannot discount the possibility of another rip either in the current environment.

There remains little sign of progress on Iran. The threat remains the ever present one of erratic escalation as Trump loses patience (as per his threat that military action is ‘to be continued’), or a supply squeeze that gets too painful as it drags on (the alternative threat mooted is a sustained US Iran port blockade that turns into more of a siege and war of attrition). News here, as we know, tends to gyrate erratically by the day and by the tweet, but time keeps ticking on for global supply chains.

Given all the above, the commodity complex has to contend with conflicting pulls – medium-term thematic trades with sound rationales, running into short-term realities and positioning. Increased volatility and potential sharper corrective moves (from Kospi, to metals, the tech stocks), if seen, threaten some sharper near-term position shakeouts.

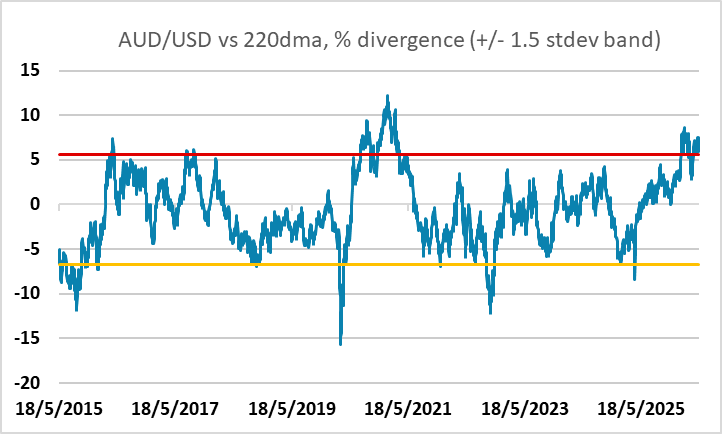

It was notable that even with the latest oil gains, USD/NOK at the time of writing was shaping up for a weekly outside reversal on NOK driven losses, with deteriorating short-term charts seen across other commodity pairs. The much-favoured AUD/USD also broke its monthly trend, albeit with 0.71/7050 congestion still in the way of a more significant, deeper retrenchment to the longer-term uptrend.

Elsewhere this week, Mon-Tue see the G7 meeting of central bankers and finance ministers, though this isn’t the truly pivotal FX event it once was.

Japan wants to talk about recent bond volatility (and no doubt orderly FX). Host France agenda includes agreement regarding global imbalances, in the context of sectoral mismatches, nodding to US fiscal excess as part of the framing (good luck with that). New oil releases said to not be on the official meeting agenda, though energy stresses clearly will be a hot topic. While not the major event of old, it's clearly worth monitoring headlines for unexpected remarks, particularly from the US.

As for the yen, it is still struggling at present to pull away from ‘dollar leadership’ and reprise its standing as a risk-off outperformer, even if the threat of intervention slows. If and when there’s a more disorderly risk-off move and a true spike in volatility (VIX is still below 20) that would be a truer test of its susceptibility to carry shakeout. Up the stairs (with BoJ standing in the way) and down the elevator risk remains the risk profile here. We do have notable data out of Japan this week though you suspect that yen and oil price action ultimately matter more for the next BoJ decision than the data (currently around 70% priced for a hike).

In the UK, it looks like most of the cards have now been played and we are waiting to see if Burnham can win the summer byelection now and set the scene for a contest to follow. If he overcomes the Reform challenge in that contest that would embellish his credentials further. EUR/GBP has 0.8743/50 now as fairly close range-resistance above the highs to date, having seen the anticipated decent rally off the range base. While cable has shown leadership, further action on the cross is also being limited by periodic EUR/USD catch up. With most of the news out now, any further action would likely have to come instead from technical driven gilt follow through (gilt future giving up on previous 90- base). While there is an argument that the ‘Burnham is the most market negative outcome’ line pervading is a bit of a caricature, for spot markets that’s an argument for another day.

Data and events for the week ahead

USA

With the data calendar limited the main item on the US calendar outside the global geopolitical situation will be FOMC minutes from the April 29 meeting on Wednesday. That meeting saw three hawkish dissents wanting to remove an easing bias and Fed’s Powell at the press conference suggested more were leaning in that direction, and that a change in the language could come as soon as the June meeting. Should the minutes show increased concern over elevated inflation it will add to doubts over whether incoming Chairman Warsh will be able to steer the Fed in a dovish direction. Moderate Fed voter Paulson is due to speak on Tuesday.

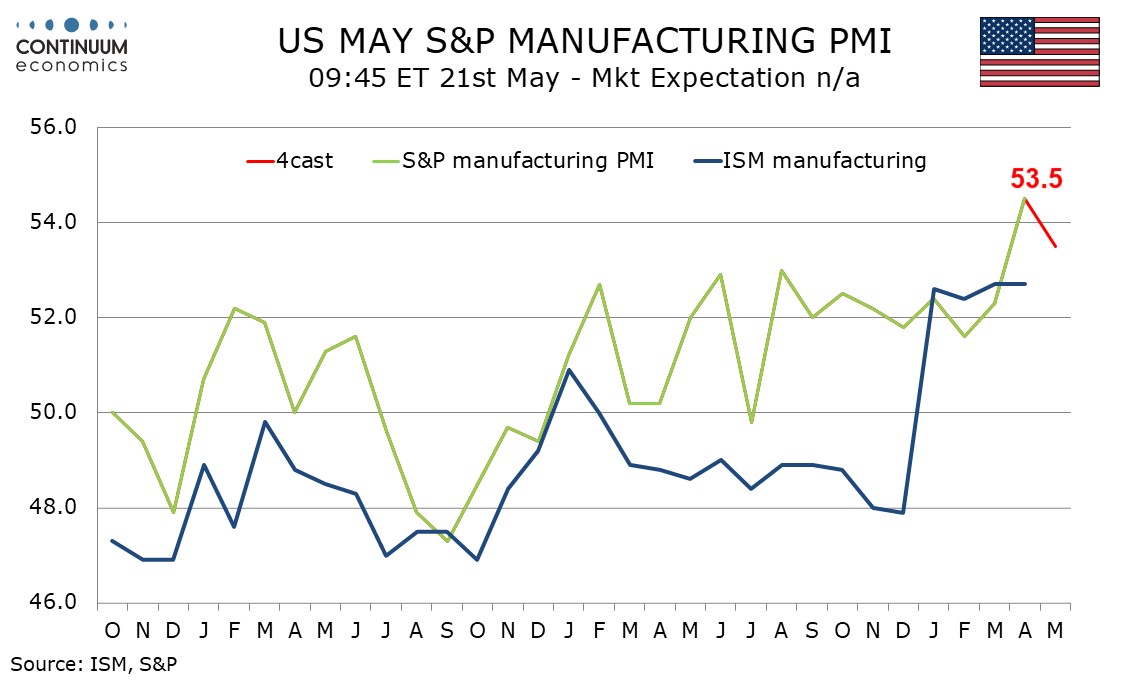

We will see some fresh signals on the housing market outlook, probably negative, from May’s NAHB homebuilders’ survey on Monday and April pending home sales on Tuesday. On Thursday we expect April housing starts and permits to both come in at 1.40m, respectively down 6.8% and up 2.7%. Thursday also sees weekly initial claims and May’s Philly Fed manufacturing survey. May S and P PMI indices follow, we expect slippage in manufacturing to a still healthy 53.5 from 54.5 while services remain unchanged at a subdued 51.0. Friday sees the final May Michigan CSI. The preliminary release saw slippage, while inflation expectations avoided further acceleration from April.

Canada

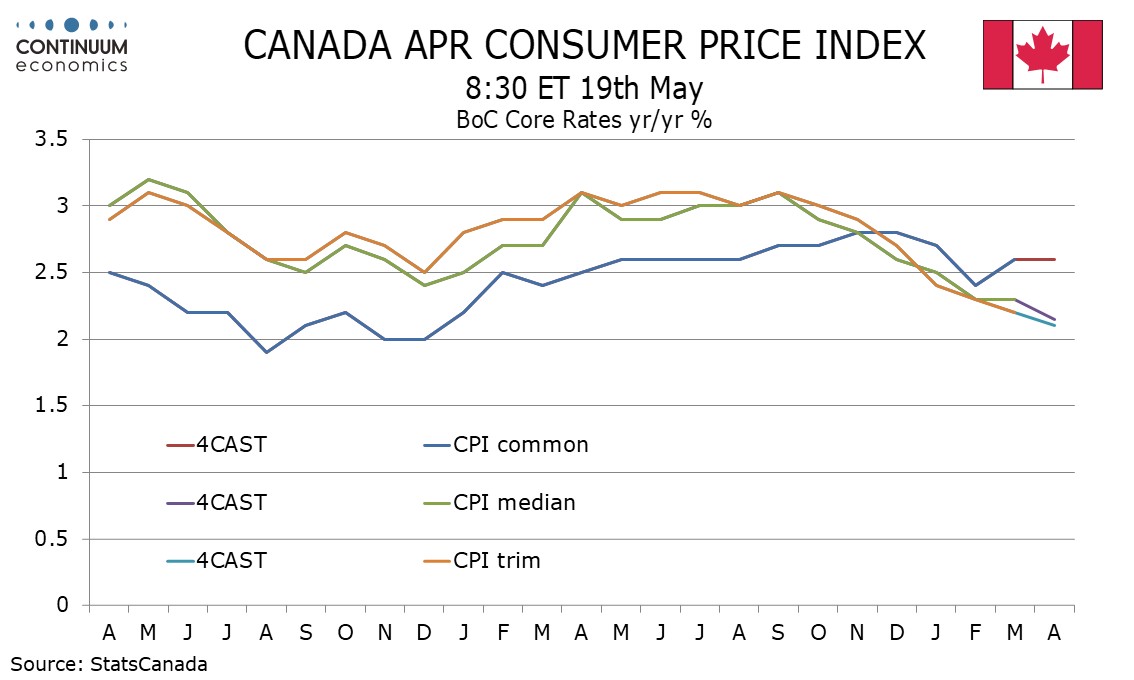

Canada’s key release is April CPI on Tuesday. We expect acceleration to 2.9% yr/yr from 2.4% in March, the bounce in part due to the April 2025 abolition of the carbon tax. We expect the BoC’s core rates on balance to continue declining. Friday sees March retail sales, for which the preliminary estimate was for a 0.6% rise, which is likely to be negative in real terms. April’s IPPI and RMPI are also due.

UK

After what may be softer Rightmove housing data (Mon), the coming week sees several important economic updates looming, most notably the CPI (Wed). The stormy weather inflation wise is now very evident, most notably in UK fuel prices surging, albeit they stabilizing more recently. Even so, softer inflation readings are seen in the April, both as Easter effects unwind and also those base effects from the array of service and utility prices rise of the year before, compounded by this April’s OFGEM-induced energy price cap cut in prices. Indeed, we see the headline down 0.2 ppt to 3.1% despite a circa 6% rise in fuel related energy, this offset by services dropping almost a full ppt, taking the core down to 2.5%.

There are also the ever-more important labor market numbers the softening in which even arch BoE hawks admit could tame second-round effects. But this data release (now partly post-Iran War), encompassing updates not just from the long-standing ONS but also real time figures from the HMRC (which we suggest are more authoritative data and are now officially accredited) is likely to see further drops in the official earnings data. lndeed, private sector regular earnings are now running at below 3%, the lowest since pandemic related pressures softened them in mid-2020 and down to a pace consistent with the 2% CPI target. Only a little further drop is seen in the looming update.

Otherwise, the HMRC numbers are likely to show that employment is continuing to contract and maybe more broadly so as far as the private sector is concerned, while its pay data may suggest a fresh slowing.

Friday sees monthly public borrowing numbers which are running slightly below year-before levels. The previous day also sees CBI industry survey numbers these being much weaker than their PMI manufacturing counterpart. But it is the May PMI flashes (Thu) that take precedence at least in market eyes, as these will show a third month’s impact from the Middle East conflict. In April, the UK PMI Composite Index rose to 52.6, up from 50.3 in March and indicative of a moderate upturn in output levels. This reflected higher levels of manufacturing production and service sector activity in April the former looking suspicious or at least unsustainable. We see a fresh clear slide in the May numbers.

Elsewhere, war-induced worries should feature again and possibly more strongly in the GfK consumer confidence numbers (Fri) arriving on the same day as we expect a similarly-driven correction in April retail sales figures, especially as the early Easter effect may go into reverse. There is plenty from the BoE in terms of MPC appearances, individually from Breeden (Tue) and arch-dove Taylor (Thu) but with the Commons Treasury Committee hearing evidence on the Bank of England Monetary Policy Report – Governor Bailey leads the BoE representatives. Otherwise, amid rising gilt yields and political uncertainty, markets may now be more alert to Moody’s updated UK credit rating decision (Fri).

Eurozone

Still suggesting weakness even before the Iran War started, visible trade data (Tue) may show further softness. But the focus will be on the flash May PMI data (Thu). The question being how much of a further correction down occurs. Indeed, the Composite PMI Index fell below the 50.0 no-change threshold that allegedly separates growth from contraction for the first time in almost a year-and-a-half in April. Other survey day appears Thursday in tern of consumer thinking and what will still be feeble IFO numbers (Fri) We see no change fir May’s numbers. But the week sees ECB Lane speak twice (Tue & Thu).

Rest of Western Europe

There are few key events in Sweden, with Riksbank Board speeches (Wed). The main focus may be on what have been volatile but trending higher jobless data (Thu). In Switzerland, there is little of note. Norway sees the Norges Bank releasing it expectation survey for Q2 (Thu).

Japan

Q1 Preliminary GDP will arrive on Tuesday and is expected to be on the soft end. Household spending has previewed a poor Q1 but business CAPEX and Government Spending could support economic growth. It is likely we will not see the impact of oil shock yet. After a slate of tier two data, we will have National CPI on Friday. With stimulus still playing, headline CPI is expected to be suppressed, along with core. Core-Core CPI could remain above 2%.

Australia

Labor Data to be released on Friday. It should continue to demonstrate the steady Australian job market but could see the initial effect of energy shock that drove a dovish turn. We also have RBA meting minutes on Tuesday yet no cues maybe limited.

NZ

Trade balance On Thursday and some tier two data throughout the week.