This week's five highlights

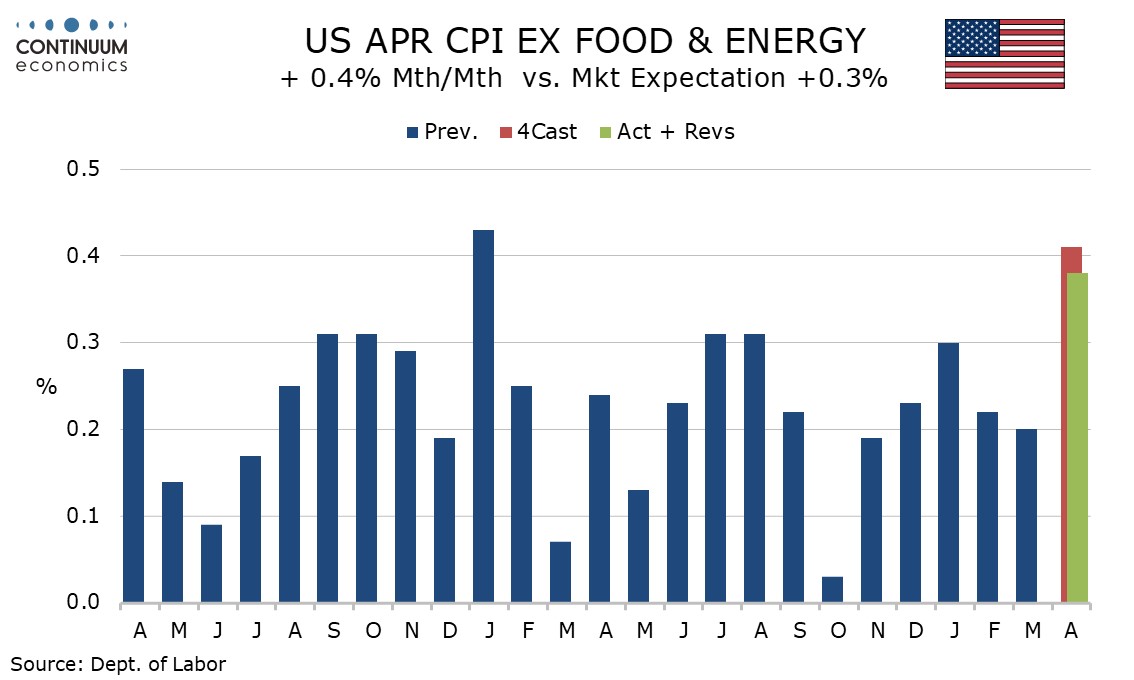

U.S. CPI Subdued and one-time strength in shelter

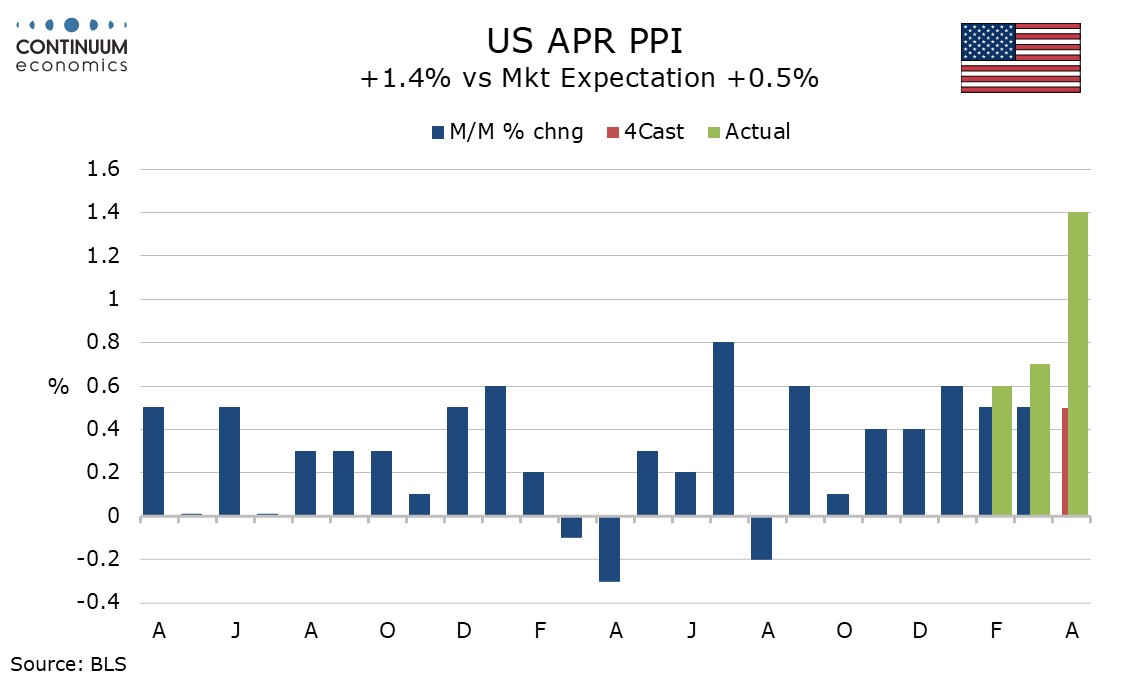

U.S. PPI Shows Strong picture restored

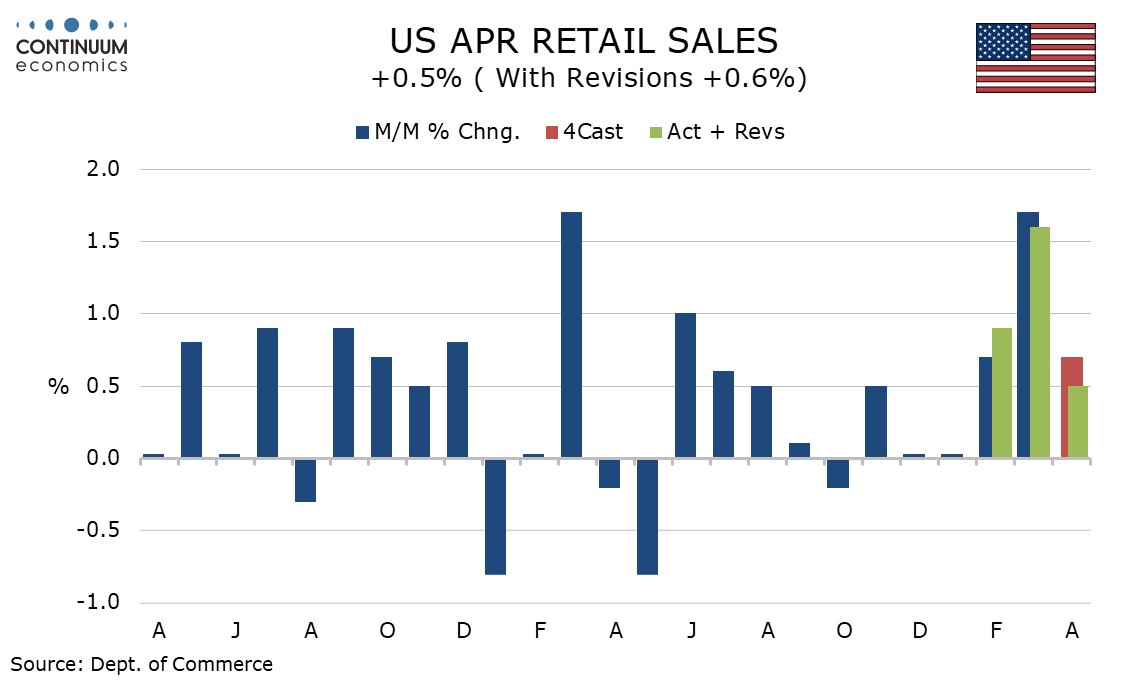

Another U.S. Data

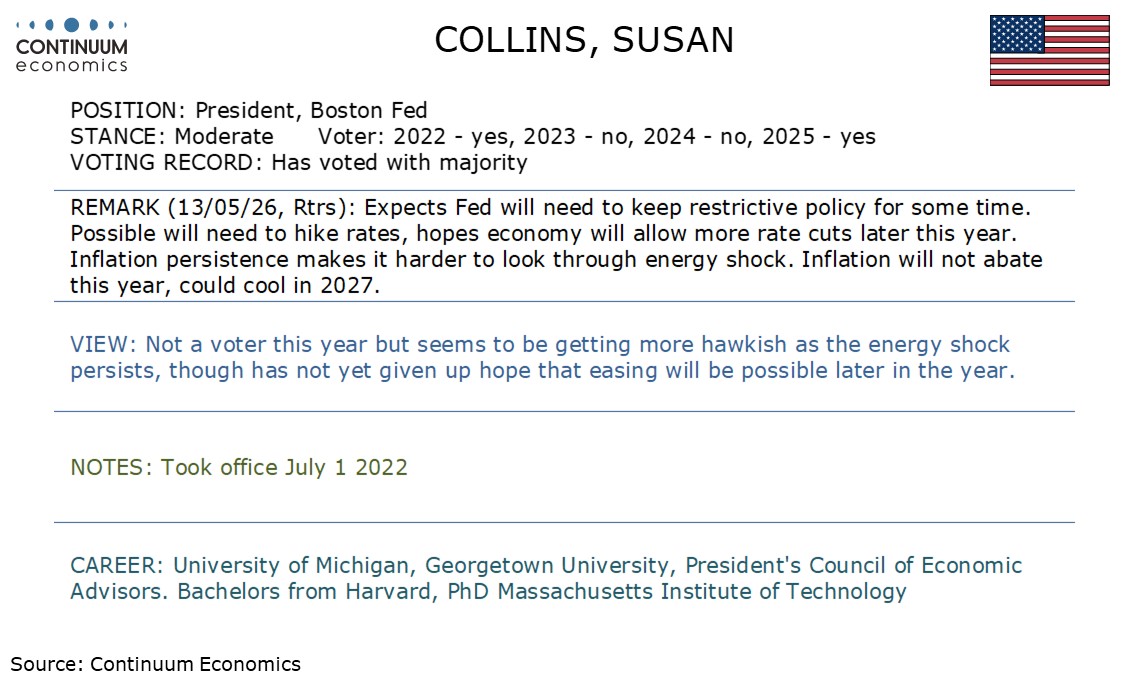

This Week's Fed Speakers

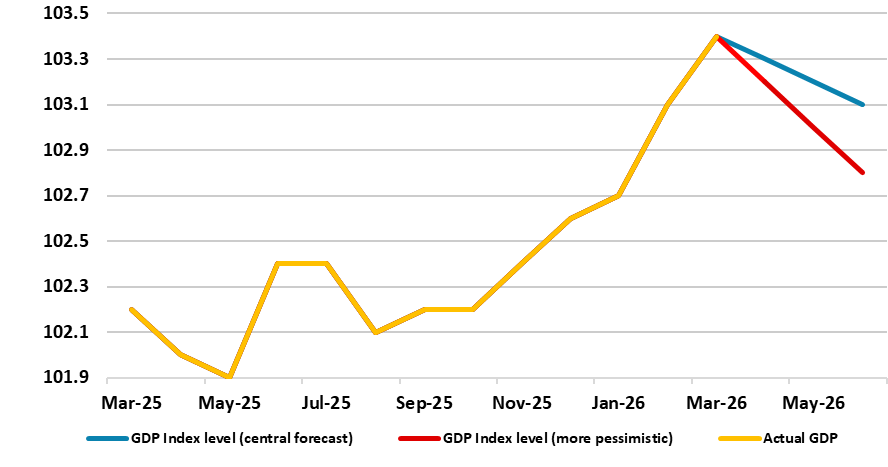

UK GDP Upside Surprises Continue

April CPI is only marginally stronger than expected on the core rate, up by 0.4%, 0.376% before rounding, and the data not alarming outside of a one-time distortion in housing. The headline gain of 0.6% was as expected, and here the rise was a little firmer at 0.64% before rounding. Shelter rose by 0.6%, double March’s pace, with owners’ equivalent rent up by 0.533%, its highest before rounding since April 2023. Here some measurements are taken every six months and with there having been no October 2025 CPI due to the government shutdown this month’s data is effectively boosted by the missing October 2025 data. Shelter got an additional boost from a 2.4% increase in lodging away from home, a volatile component.

CPI ex food, energy and shelter rose by a moderate 0.19% before rounding, in line with recent trend. Air fares rose by 2.7% after a 2.6% increase in March, implying some feed through from energy prices, but these are not exceptional gains for this volatile component. Transport services saw a moderate 0.3% increase, restrained by a fall in car and truck rental and with most subcomponents subdued.

After a surprisingly low March, which saw modest upward revisions, April PPI has rebounded above expectations, rising by 1.4% overall, 1.0% ex food and energy and 0.6% ex food, energy and trade. March and April together show the strength of January and February’s core rates persists, with energy, though not yet food, accelerating. The 1.0% rise ex food and energy and the 0.6% rise ex food, energy and trade both follow gains of 0.2% in February, with the latter having increased by 0.5% in both January and February.

April retail sales with a rise of 0.5% overall, 0.7% ex autos and 0.5% ex autos and gasoline are in line with expectations, and while likely to be marginally negative overall in real terms the ex autos and gasoline data suggests continued consumer resilience. Initial and continued claims have both picked up from two exceptionally low weeks, but remain at a low level. Auto sales fell by 0.4% after gains of 0.6% in February and 1.0% meaning the dip is not a clear sign of weakness. A 2.8% increase in gasoline sales looks like a decline in real terms, slowing more from March’s 13.7% surge than did gasoline price gains.

Figure: GDP Growth Hardly Strong and With Clear Downside Risks Ahead?

Perhaps it is a supreme irony that just as the Labour government tears itself apart after disastrous election results last week, the actual real economy continues to surprise on the upside. Notably, since taking office in July 2024, the economy has grown a cumulative 2%-plus, ie over 1% per year. Indeed, providing yet more signs of apparent economic resilience and, once again exceeding expectations, GDP grew by 0.3% m/m in March 2026, following growth of 0.4% in February and no growth in January (each revised down by 0.1 ppt). Services and construction output both grew, by 0.3% and 1.5%, respectively the later the main factor behind the overall successive upside surprise but where these growths were partially offset by a 0.2% fall in production. The question is whether this more recent growth is illusory, not chiming with business survey data and where it may reflect even further inventory building, most recently prompted by the outbreak of the Iran War.