U.S. Initial Claims low, Philly Fed stronger, price indices mostly firmer but not alarming

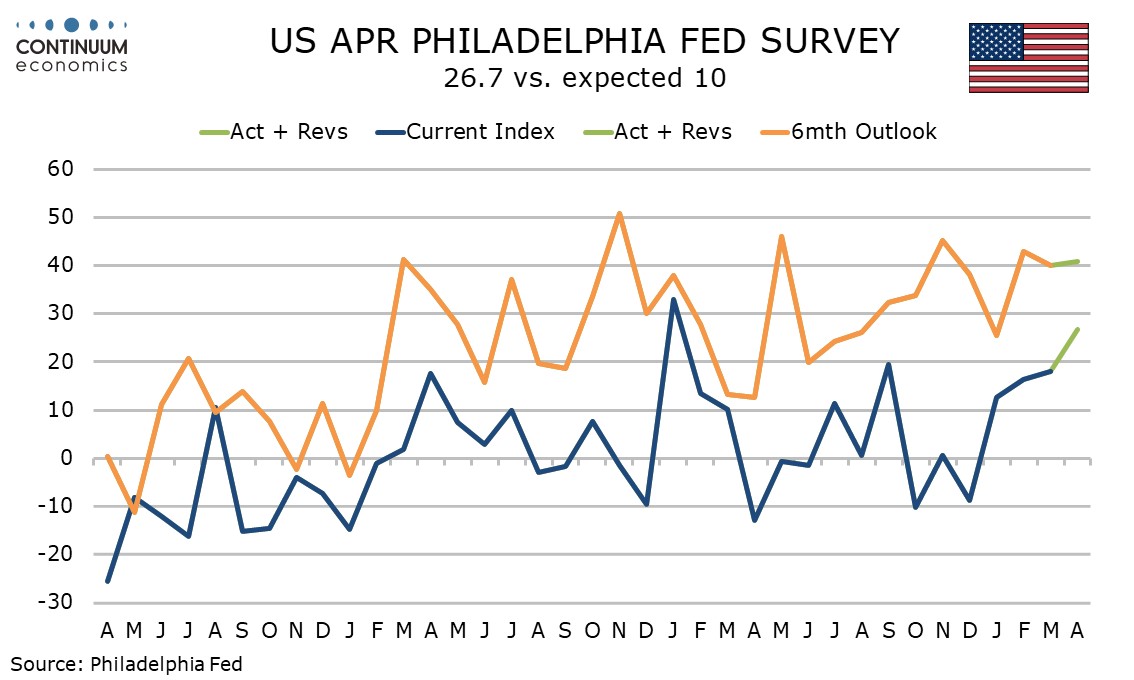

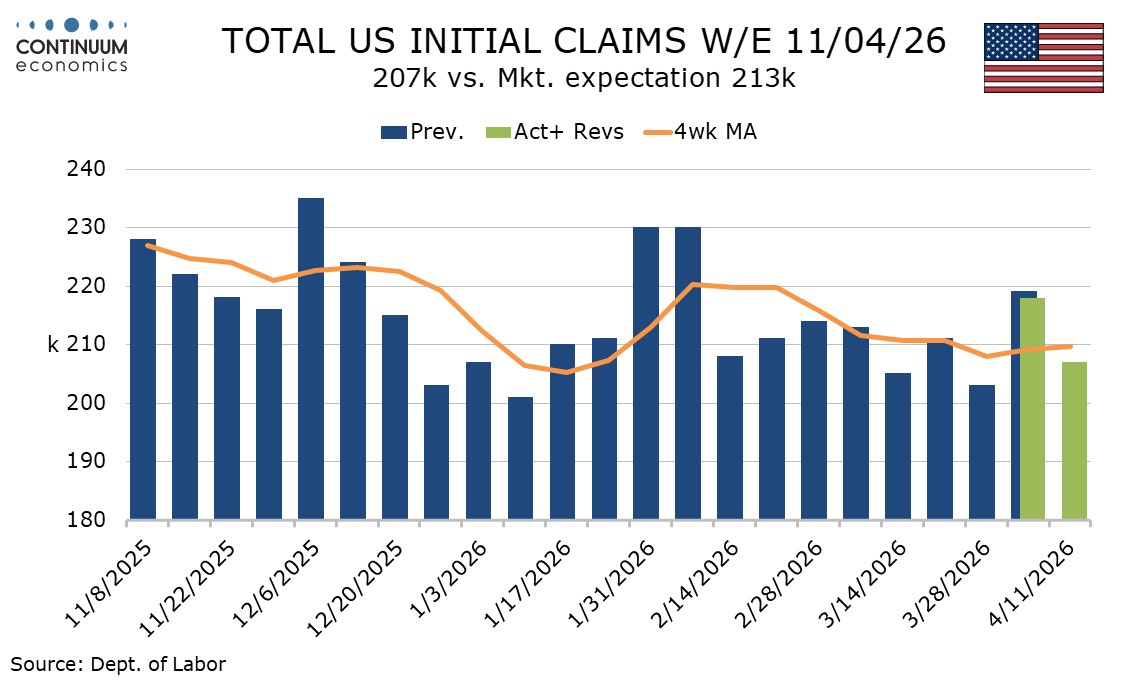

The latest US data suggests the economy so far is holding up well to the oil shock, with initial claims low at 207k from 218k and the April Philly Fed at 26.7 from 18.1, reaching its strongest since January 2025. Price data is mostly firmer, but not alarmingly so.

The stronger than expected Philly Fed reading follows a similarly improved (if less strong) Empire State manufacturing survey yesterday. In contrast to the Empire State data, Philly Feb six month expectations also held up well, at 40.8 from 40.0.

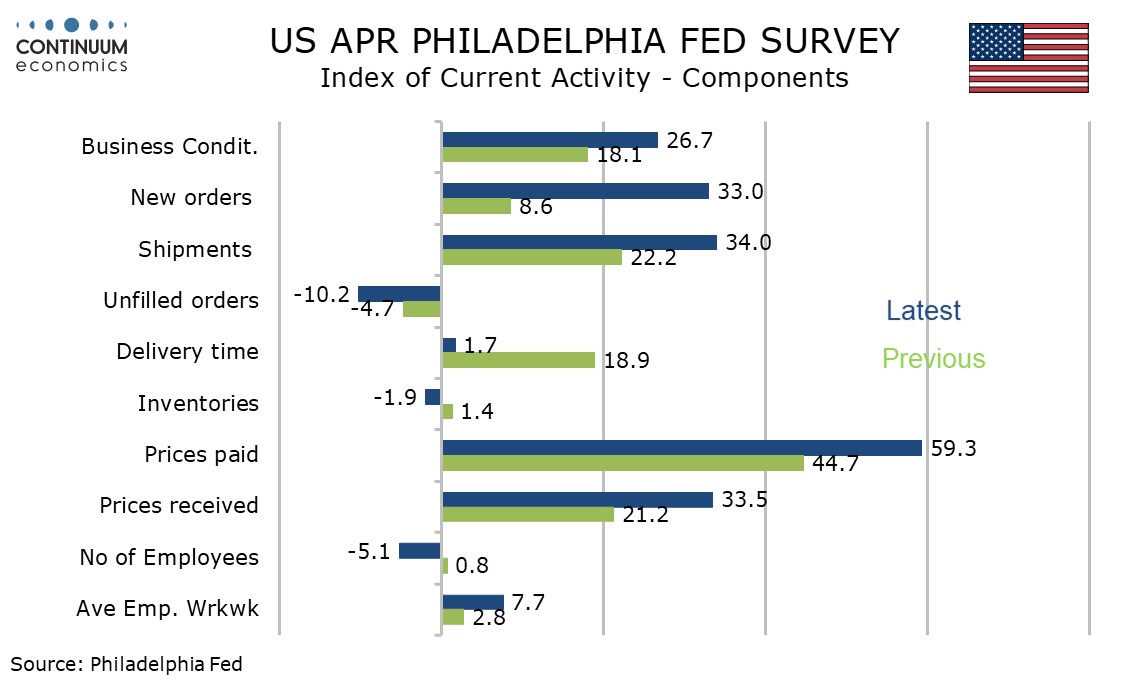

Philly Fed detail shows new orders very strong at 33.0 from 8.6, but employment slipping to -5.1 from a positive 0.8 in March.

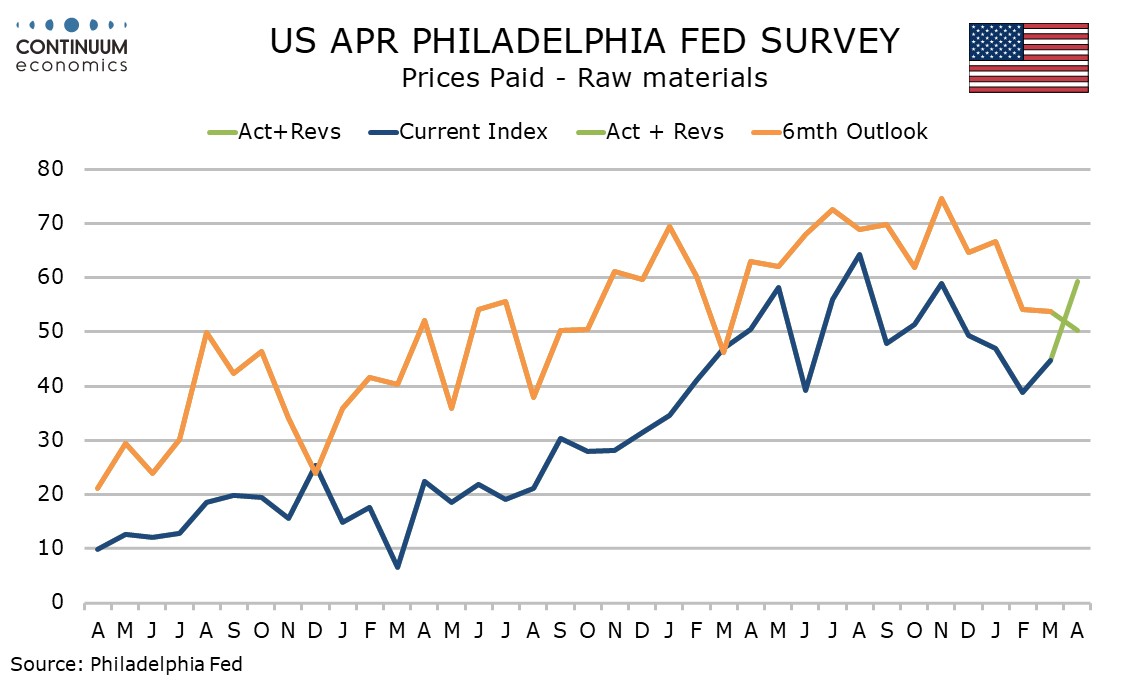

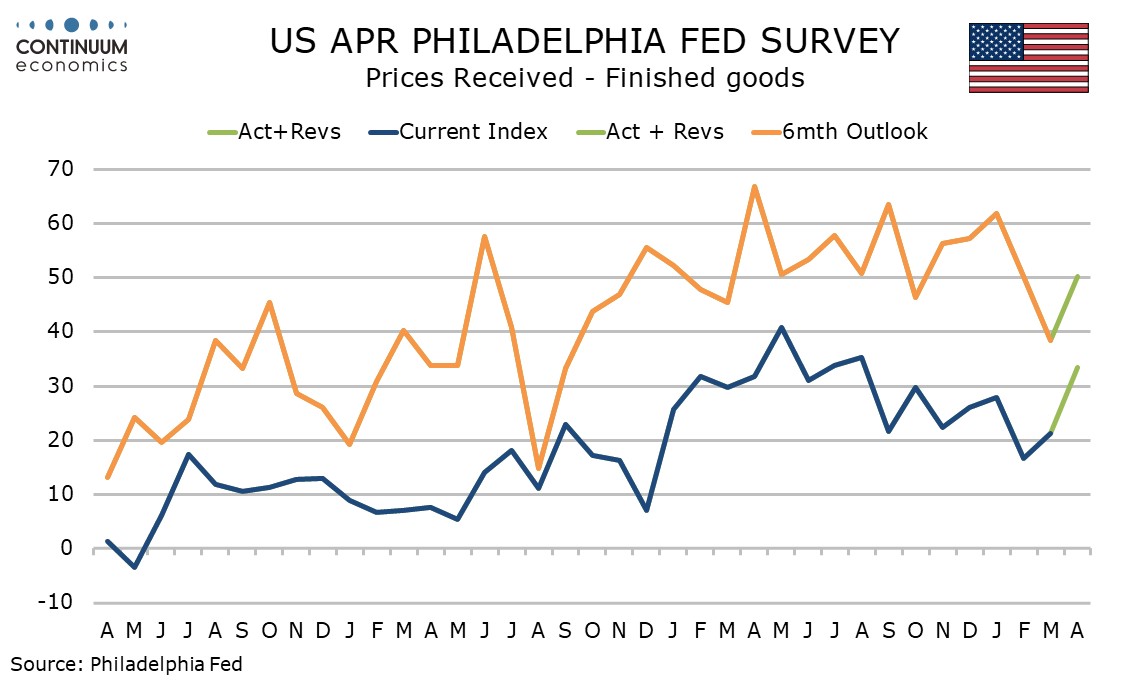

Prices have picked up, though the levels are not exceptional by recent standards, suggesting the inflationary impact from energy prices is being partly offset by a fading impact from tariffs. Current month prices paid at 59.3 from 44.7 are the highest since November, while current month prices received at 33.5 from 21.2 are the highest since August.

6-month expectations show prices paid actually slowing to 50.2 from 53.7, this the lowest since a pre-tariff reading in March 2025. 6-month prices received rose to 50.2 from 38.4, but remain just below February’s 50.2. The Philly Fed’s price indices are reasonably consistent with the Empire State’s.

Initial claims at 207k are in line with trend, after an above trend 218k last week corrected a below trend 203k two weeks ago. The survey week for April’s non-farm payroll comes next week. Healthy signals on the labor market are consistent with improving data in the weekly ADP employment data released on Tuesday.

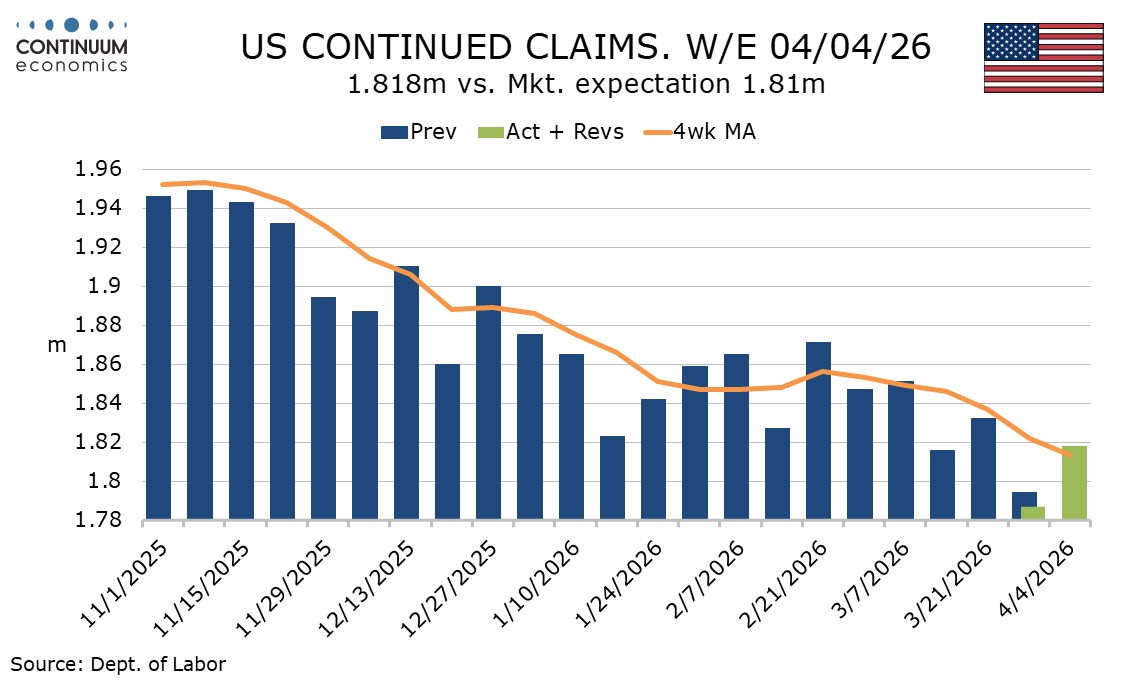

Continued claims cover the week before initial claims and like last week’s initial claims corrected from a very low preceding figure, rising by 31k to 1.818m after a preceding 45k decline. A downtrend in the 4-week average has resumed after stalling in February.