Norges Bank Preview (Mar 26): How Hawkish Will the Board Sound?

While no change in policy is expected from the Norges Bank’s verdict due on Mar 26, a clear shift in rhetoric is almost inevitable. It may very well drop its recently repeated assertion that ‘the policy rate will be reduced further in the course of the coming year’. The question is whether it will suggest that the next policy move may be in either direction or even suggest a hike is now more likely, though being deliberately vague as to any possible timeframe. Such vagueness would be understandable but any clear warning of hiking would be premature to say the least – NB the softening in house prices now emerging is very probably a reaction by households to the reining in of rate cut expectations in recent months, ie prior to the outbreak of the war in Iran.

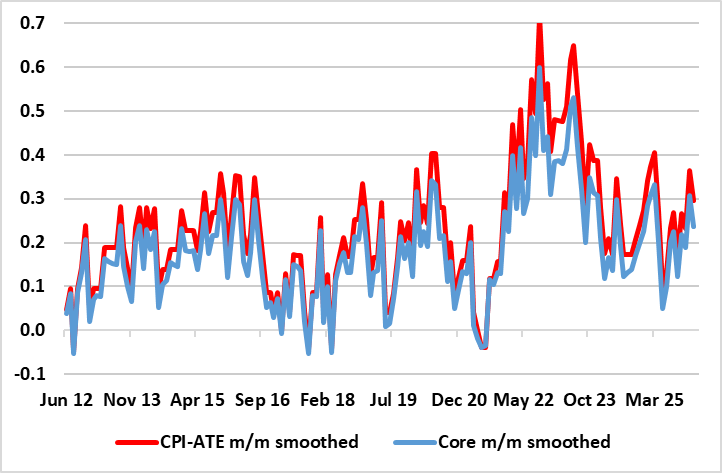

Figure 1: Underlying CPI Inflation Actually Well Behaved

Source: Stats Norway and CE – Core is ex food and energy, % chg y/y

Regardless with underlying inflation dynamics being far from unfriendly (Figure 1) and seemingly downside economy risks materialising, we still think that the Norges Bank has already been far too cautious as its existing plans point to keeping policy very restrictive through the projected timeframe out to 2028, ie the policy rate stays above 3%. For some time, we have argued that Norges Bank’s fixation with apparently resilient inflation was overdone, resulting in overly cautious policy-making, the latter also fixated by the exchange rate. This inflation caution has intensified of late both by what have been some upside CPI surprises and of course by the likely impact of the Middle East conflict.

Given Norges Bank caution, we remain far less confident about the extent of easing into 2026 and have scaled back our projections at least for the current year. Any hike of the ilk markets have factored in the course of next few months is likely to be short-lived both as disinflation resumes and the real economy toll becomes more evident. More likely, we envisage two further 25 bp cuts in H2 and then 100 bp of cuts through next year. At 2.5%, that would still leave the policy rate still within the neutral rate range estimated by the Norges Bank. In other words, the Norges Bank will be merely taking its foot of the brake, rather than pressing on the accelerator.