UK GDP Review: GDP Still Moving Sideways?

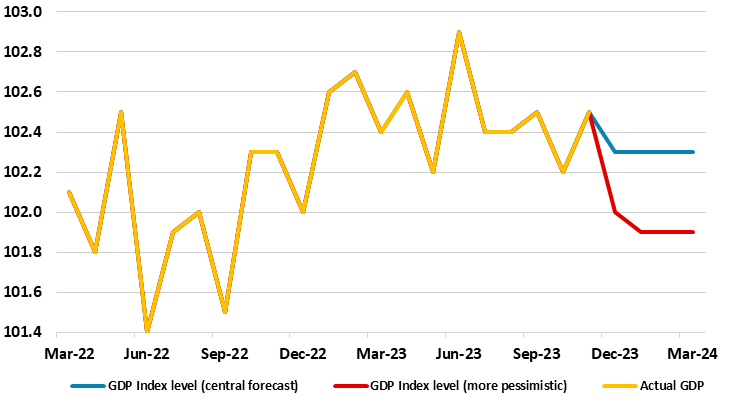

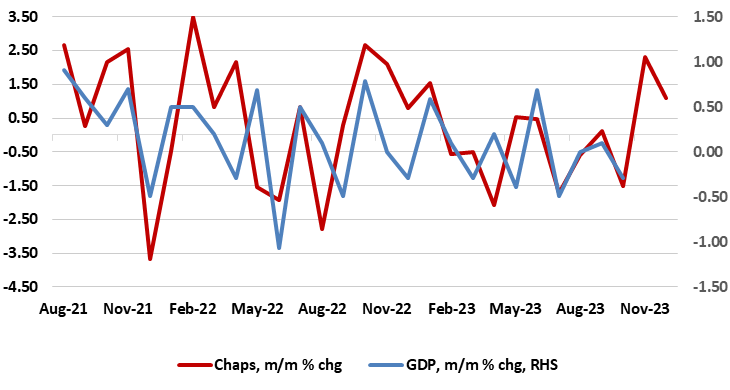

Coming in higher than expected, and probably boosted by less poor weather and a correction back in imports, GDP rose by 0.3% m/m in the November data, a result that meant that the surprise drop of the previous month was exactly reversed (Figure 1). Regardless, there may be some fresh fall in the looming December numbers, (albeit with some upside risks posed by some survey data (Figure 2), this flagged by what we think will be a fresh drop in retail sales, a result that still suggest a small contraction in Q4 GDP and thus a recession will have occurred given a second successive drop. Regardless, a better description of the economic backdrop is one of the economy moving sideways.

As for the economic outlook, the backdrop is looking softer still. Recent GDP sectorial updates suggest a much weaker growth picture for Q2 and Q3 last year, meaning that the 2023 average rate may be no higher than 0.2%, less than half the now out-of-date consensus and with this downgrade threatening an outright contraction for this year: we now see a 0.1% drop.

Figure 1: UK GDP Still Volatile but With Downside Risks…

Source: ONS, CE

Downside Risks Still Clear?

GDP is estimated to have fallen by 0.2% in the three months to November 2023, compared with the three months to August 2023. Monthly GDP is estimated to have grown by 0.3% m/m in November 2023, following an unrevised fall of 0.3% in October 2023. Services output grew by 0.4% in November 2023 and was the main contributor to the monthly growth in GDP; this follows a fall of 0.1% in October 2023 (revised up from a 0.2% fall in our previous publication). Production output grew by 0.3% in November 2023, following a fall of 1.3% in October (revised down from a 0.8% fall in our previous publication). The construction sector fell by 0.2% in November 2023 after a fall of 0.4% in October 2023 (revised up from a 0.5% fall in our previous publication). Admittedly, weather patterns have helped accentuate swings in monthly GDP numbers of late but where the essential trend remains flat and where domestic demand weakness is still being masked by softness in imports. But elsewhere the allegedly less-weak housing market is an impact via the fall in transactions.

Figure 2: But Also with Some Risks to the Upside ?

Source: ONS, CE