FX Daily Strategy: N America, May 12th

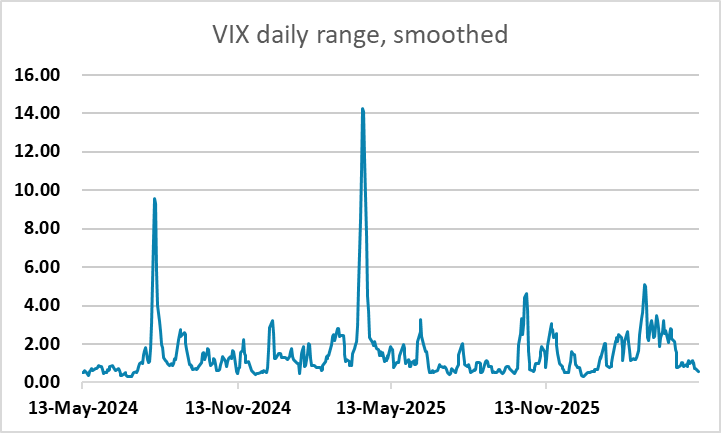

Volatility keeps compressing though maybe some tensions showing at the edges

No shift in ranges and trends yet, but if the fever breaks, USD and JPY correct

US CPI data to keep the Fed in defensive wait and see mode

GBP plays the 'political short' trade as gilts spike, though spec mkt was positioned

Focus starts to turn to US-China meetings

Another start to a week, another round of Trump comments, another oil bounce - now just managing to nudge back through $100 at the front end. The market continues to wait out the noise and trend on regardless, though some tensions are emerging at the edges it feels. It's not so much that the market has been (only) complacent it seems. It's more that it has been rather imprisoned in its state of fake calm and lack of volatility through the lack of signal to noise in the headlines, the hope that logic will dictate a resolution, and the FOMO and gamma action in the heated equity sectors. The challenge with these episodes is that these artificial compressions in volatility do eventually tend to resolve in an eventual breakout when a catalyst does appear but it can be hard to second guess as the benign action rolls on.

There are of course plenty of conceivable candidates for that, be it a harder to ignore Iran re-escalation, that anyway still seemed mired too long, or even an eventual break in the ‘dash for compute’ equity fever. The semiconductor market has been a bit of an arm wrestle between spot and options trading of late, but it is hard to not view the recent vertical acceleration as ‘stretched’ as it stands, regardless of your take the medium-term outlook after recent massive spend commits out of earnings season. In any case, the broad risk market seems priced for the most benign scenarios, which leaves the risk of surprise quite skewed. For now, there's no real damage to be seen. But with the market still making that weekly stretch outside its Bollinger band, along with RSI and stochastics right up at the range tops, how heated the move has got in the process is of course very much on show.

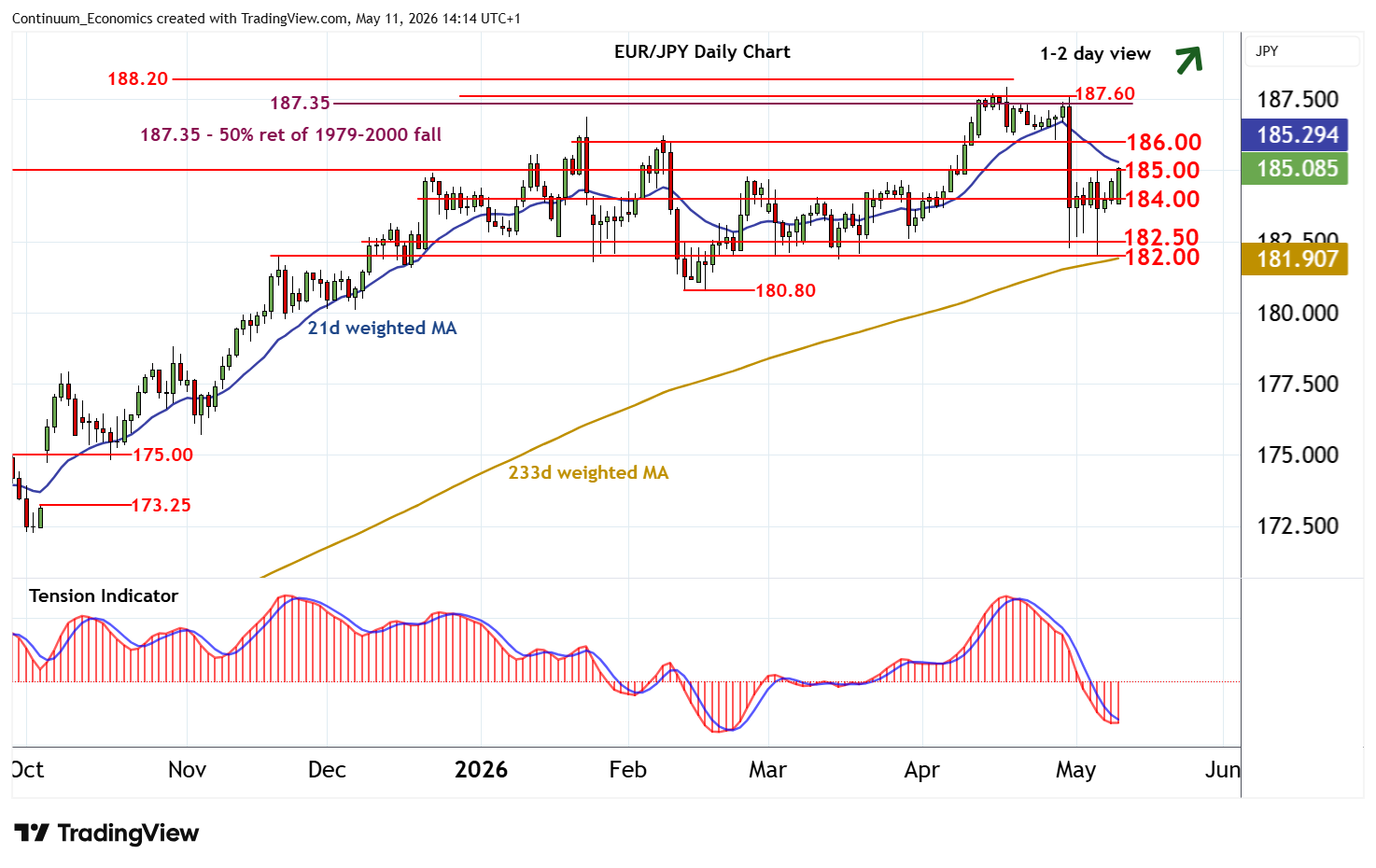

If and when the action breaks in coming days, then the dollar does likely firm against the grain. There's still that sense in the FX market that a further dollar bounce is the most unloved scenario, which is frequently the one the market somehow has a habit of delivering. The yen crosses still offer that ‘optionality’ given the BoJ desire to floor the yen downside (at least sanctioned by the US even if not joined) and the relative cheapness of the yen by recent year’s standards on any spread or risk premium benchmark. For EUR/JPY though it would need an impetus to push below 184 to look to 182, and a break below the latter to be looking more negative and encourage some follow through on the major trend break.

Elsewhere, reprising one of its favoured thematic trades, there has been some attempts to get some fresh momentum behind the political short GBP trade. Reports of more than 70 Labour MPs calling for the PM to go and an exodus of ministerial aides provides the news backdrop, but it’s more the continuation of the election fallout really. A “crunch cabinet meeting” this morning being watched for any fallout today now, with initial reports that Starmer is still resisting resignation - though for how long seems questionable.

Gilts notably saw quite a strong gap open, the future testing the contract low with 10s back clear of 5% testing the 23 Mar 5.11/2 highs. 30s also tested (just through) the recent 5.79%- highs. Cable saw the expected test back to 1.35 on this move, while EUR/GBP continued its bounce back into the April range after holding and lifting off 0.8610 lows - as favoured in the Weekly Outlook.

All that being said, it does have that slight feel of a cliché overly one-dimensional trade and we have seen speculative pre-positioning for it, that had actually been slightly out the money. Gilts might look to refill their opening gaps left behind at some point and then it’s a case of whether the major support / yield resistance areas hold. Headline focus start to shift to the background political jockeying to see who emerges as the main challenger (and from which wing of the party) - expect plenty of interest in the event betting market.

The main highlight ahead will be US CPI. We are in line with market in looking for 0.6% overall and 0.4% ex food and energy, albeit with a likely one-time boost from a distortion in owners’ equivalent rent, adding 0.1% to our forecast. This lifts the yr/yr growth to 3.7% from 3.3% overall and to 2.8% from 2.6% ex food and energy and leaves the Fed in its current defensive wait-and-see mode.

Focus will then be turning to US-China trade talks and summit Wednesday onwards, events that could distract Trump from Iran and keep the wires busy. Ordinarily, you would expect these to be pre-choregraphed but with Trump the potential for unexpected comment is always high. USD/CNH has been nudging 3 year lows into the event reflecting the trend action, tendency for CNY to firm through these meetings, as well as support from resilient domestic data and the strong commodity cycle.