China: 4.5-5.0% GDP Growth for 2026

• China announced a central government budget deficit at 4% of GDP, which is the same as last year and points to only modest fiscal stimulus. Though investment was supported, consumption trade in programs were cut from Y300bln to Yuan250 and no new structural safety net for households have yet been announced. Consumption was the 4th priority and the 4.5-5.0% growth target is an acceptance that cyclical headwinds remain (residential property investment and modest consumption growth) and structural forces are having an impact (population aging). All of this is modest support and we see no reason to change our 4.4% GDP forecast for 2026.

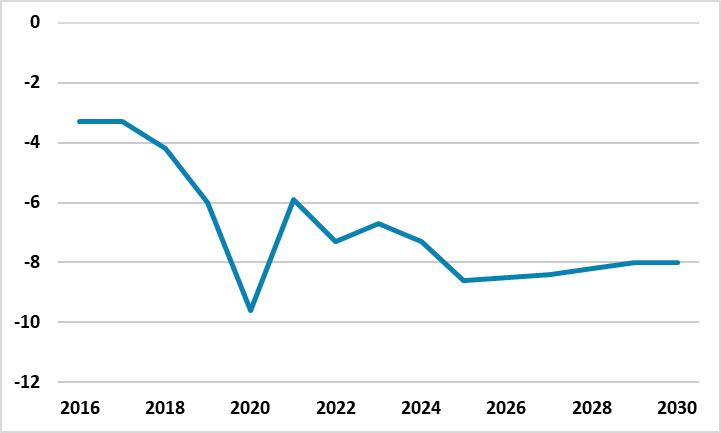

Figure 1: China General Government Budget Deficit to GDP (%)

Source: Datastream/Continuum Economics

China initial announcements at the National People Congress (NPC) show only modest fiscal stimulus. Key points to note.

• 4.5-5.0% 2026 growth target. China authorities are adjusting the growth target lower to 4.5-5.0% from 5.0% in 2025, which appears to accept that some structural forces (e.g. population aging) are slowing trend growth. Though the central government budget deficit is set to be 4% of GDP in 2025, this is the same as 2025. The fiscal stimulus details so far are similar in size to 2025 i.e. modest fiscal stimulus. Too help boost investment, Yuan800bln is allocated to new financing via the policy banks rather than the Yuan500bln last year. The slightly lower GDP targets means that the authorities do not feel the need to be undertake more than modest fiscal stimulus. Additionally, China’s authorities continue to act fiscal constrained, as they appear to place weight on the IMF general government debt/GDP that is surging sharply, as the general government deficit remains close to 8% of GDP (Figure 1) and outstripping nominal GDP. Meanwhile, though the 2% inflation target was kept, monetary policy stimulus will likely only be a 10bps cut in the 7 day reverse repo rate and 75bps in RRR in 2026. The PBOC remains concerned that rate cuts could backfire and hurt bank lending by squeezing banks profit margins too much.

• Modest cyclical consumer measures. The trade in program for 2026 will be Yuan250bln versus Yuan300bln in 2025, which is a mild disappointment. Also no fiscal handouts to cyclically boost consumption. Additionally, no new measures have yet been announced to enhance safety nets (unemployment/health and pensions), which is disappointing and no new Hukou measures (here). This all shows that consumption growth is not a real priority and in the work report came 4th behind building modern industries; technological self-reliance and boosting the digital economy. Meanwhile, no accelerated bailout for residential property as the IMF has suggested (see our view here), with the official view remaining that the housing market should be merely stabilized.

All of this is modest support and we see no reason to change our 4.4% GDP.