China: GDP Beat, But Domestic Demand Weak

• Q1 GDP beat expectations helped by Industrial production, but the domestic demand picture remains weak with soft consumption and the ongoing negative drag from the residential property sector. We still feel that the economy remains too dependent on high tech manufacturing and modest consumption will act as a drag on GDP growth, while the Iran war will have an adverse impact on exports and production from Q2. Additionally, China’s authorities remain reluctant to be aggressive in policy stimulus. We stick with 4.2% GDP growth for 2026.

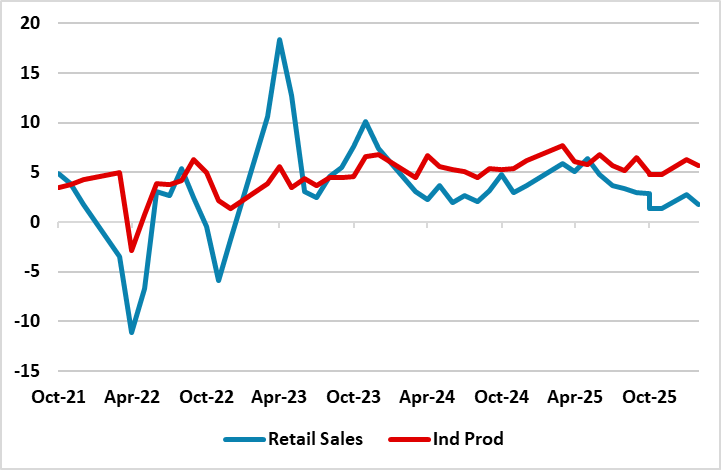

Figure 1: Industrial production and Retail Sales (Yr/Yr %)

Source: Datastream/Continuum Economics

The March China data was mixed and does not suggest the economy is picking up. Key points to note.

• GDP/IP good news. The Q1 GDP at 5.0% Yr/Yr was better than expected, which was also the case with the March Industrial production data at 5.7% v 5.3% Yr/Yr. The production side of the economy likely accounts for the GDP surprise, as other areas were soft in Q1 except government investment. However, the industrial production buoyance is ahead of domestic demand and we feel that exports are unlikely to fill the gap like 2025. Thus we see industrial production slowing through 2026. One example is automobiles, where production at +7.5% Yr/Yr is way ahead of car sales at -11.8% Yr/Yr.

• Retail sales/residential construction weak. The 1.7% Yr/Yr for March Retail sales was weaker than expected, with the breakdown showing car sales/furniture and building and decoration showing noticeable falls Yr/Yr. The key problem remains that housing wealth has been hit and is hurting consumption, but also wage and employment growth is soft and this is a drag on consumer confidence and consumption. The March budget saw less consumption stimulation than 2025 and the prospect is that retail sales will remain soft for the remainder of 2026. This is an important drag on growth. Combined with excess production, this also argues for underlying disinflation as well. However, with energy price rising feeding through, we see 2026 CPI headline inflation at 1.4% before falling in 2027 (here). Meanwhile, the residential property data shows a market that has not bottomed, with March residential property sales -18.5% YTD Yr/Yr and -11.2% for residential property investment. Home prices falls are mellowing, but this is not enough. As we highlighted in the March China Outlook (here), an excess of complete and uncomplete homes is hurting the property market. While the excess of supply v demand is now coming into balance in some tier 1 cities, it remains adverse in many tier 3 cities.

• 4.2% GDP growth for 2026. Though the data was better than expected, we expect high oil prices and an adverse effect from the Iran war to hurt China’s export growth. We still feel that the economy remains too dependent on high tech manufacturing and modest consumption will act as a drag on GDP growth. Additionally, China’s authorities remain reluctant to be aggressive, with the 4% central budget deficit for 2026 being in line with the modest 2025 fiscal stimulus. Meanwhile, PBOC remains reluctant to cut interest rates, as it could squeeze bank margins and hurt bank lending. Even so, we would still see a 10bps cut in Q3 2026 in the seven day reverse repo rate. We do see a 25bps cut in the RRR in March or April.