FX Weekly Strategy: Asia, March 16th-20th

BoE MPC Agree to Disagree

ECB No Longer in a Good Place

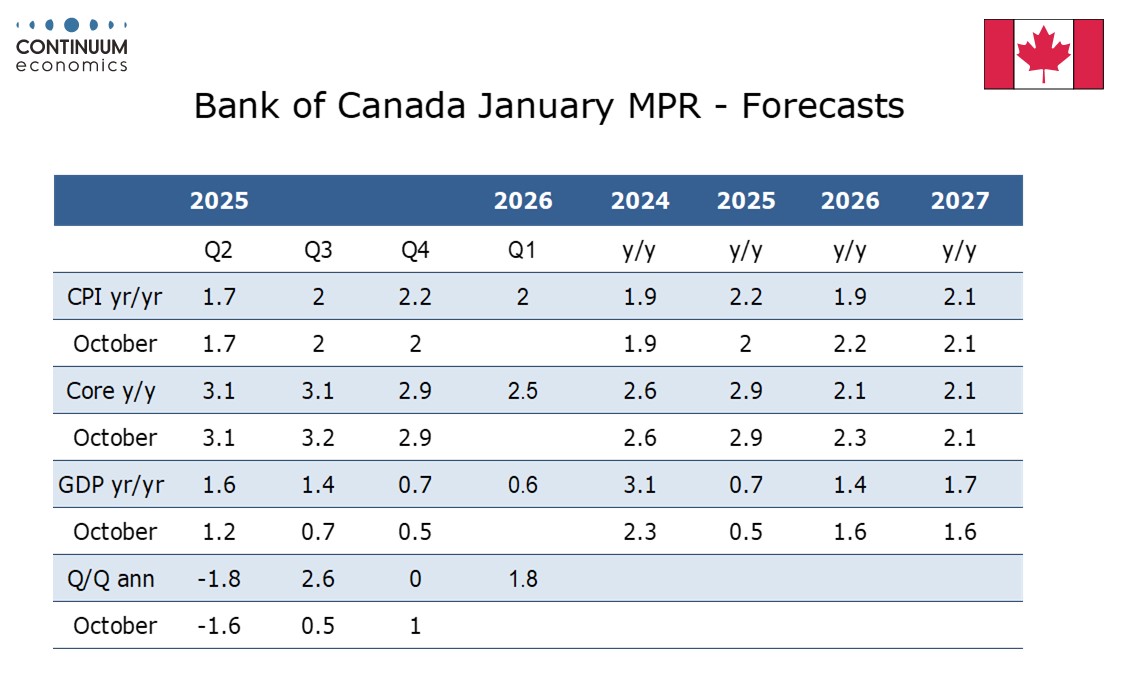

Bank of Canada No change in rates or from January's message

Swiss SNB Keeping a Low Profile

Sweden Riksbank On Hold and Still For Some Time Ahead?

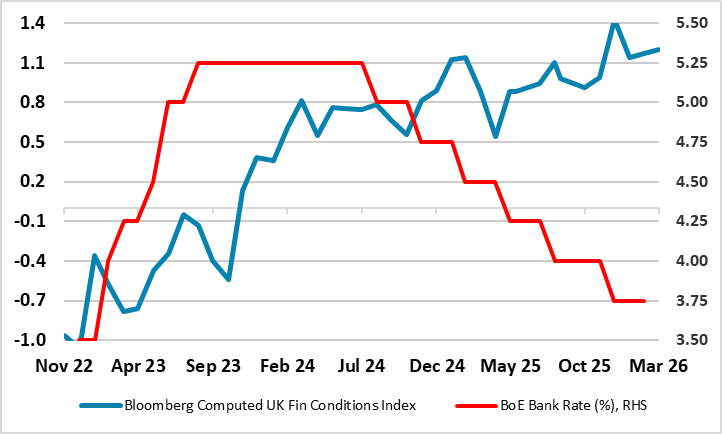

Figure: Bank Rate and Financial Conditions Diverge (% and level)

The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely this month. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a whole will not have to reveal too much about any shift in policy bias given that it does not have to provide updated forecasts until its April 30 meeting, the individual member views will show continued divides. Indeed, while February’s four dissenters will suggest they are probably deferring easing, some of the more hawkish members may be more open about considering hikes to guard against or combat any rise in inflation expectations that they think may trigger a fresh rise in wage pressures. We consider such thinking to be misplaced given the labor market is loosening and where companies face a fresh squeeze on profits. Given financial conditions, we still see at least two more 25 bp rate cuts ahead but now deferred to no sooner than late summer.

Indeed, we have long argued that the weak economy and labor market allied to tight(er) financial conditions would build the case for three 25 bp cuts in 2026 to 3.0%, the latter being a level that the dovish camp on the MPC would consider to be neutral. And a cut as soon as this month seemed very likely given that an easing was averted by just one vote within the nine-strong MPC in February, this partly reflecting downgraded GDP and inflation projections with the latter seen by the BOE falling to target by mid-year and largely staying there out to 2028.

Figure: ECB Projections in Perspective

With no change in policy expected, what the ECB says is the most important aspect of the ECB meeting next week, both explicitly and implicitly via its updated forecasts (Figure). Both are likely to underscore that rate hikes are certainly possible if the almost inevitable inflation rise proves to be either/both significant and/or persistent. But no time frames will be suggested, this papering over what are long-standing splits within the Council regrading policy. There will be some reassurance that market based inflation expectations have risen only modestly and more over the short-term than longer measures. But amid what we think has been ECB complacency and where there will be clear real economy damage from the current conflict and what we see as only a limited and temporary inflation spike, we still regard the next move in rates to be a further cut, though probably only one more 25 bp move later this year.

Like the ECB will do, we have identified four likely scenarios regarding the length and breadth of the Middle East conflict. But under our very much more likely view of limited further fighting we see oil and gas prices largely falling back to the pre-war levels within a year. This will still lead to a clear and fresh rise in inflation, mainly via the direct effects of the HICP measure having a 10% energy weighting but with some second round effects that will affect rates into 2027 (though where actual inflation at the end of next year may be lower than previously thought). This will be on account of the likely real economy damage from the conflict but also reflects our long-standing view that the Council has been complacent, downplaying what we regard are downside risks which may be materialising.

The Bank of Canada meets on March 18 and looks highly likely to leave rates unchanged at 2.25%. The statement is likely to reiterate the message given at the last meeting on January 28, that the policy rate is appropriate conditional on the economy evolving in line with expectations, but uncertainty is heightened and if the outlook changes the BoC is prepared to respond. This meeting will not see a quarterly Monetary Policy Report so the forecasts made with the last MPR on January 28 will not be updated. Since the last meeting Q4 Canadian GDP came in weaker than expected at -0.6% annualized, but with domestic demand up by 2.4%, albeit with significant support from government stimulus, the data is unlikely to change the BoC outlook significantly. Underlying inflation appears to be slowing though strength in oil prices is likely to mean Q1 CPI comes in a little stronger than the 2.0% projected by the BoC in January.

Canada’s economy will be more resilient overall than most to any sustained boost to oil prices, though outside the oil-rich province of Alberta the economy would be likely to weaken. The extra near term inflationary risk reduces what were already quite slim chances of a BoC easing, while tightening still looks some way off. Minutes from the last meeting show that Iran was one of a number of risks discussed, including Venezuela and Greenland, where risks have faded since January. Other risks discussed were threats to the independence of the Federal Reserve, and the upcoming review of the Canada-US-Mexico trade agreement, which persist. The US Supreme Court ruling against some of Trump’s tariffs is a positive development, but uncertainty overall has increased since January, due to the Middle East situation.

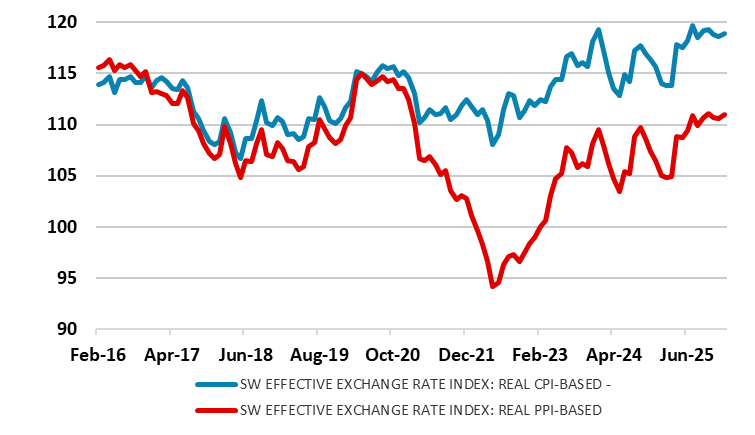

Once again and in line with consensus thinking we see SNB policy being unchanged when it gives its next quarterly assessment with little shift in the forecast for either growth or inflation. Admittedly, the tone of the economic outlook will be more guarded but where it will be underscored that it is too soon to make material changes to the outlook given current heightened uncertainties. The strong Swiss Franc will be mentioned but its current strength needs context (Figure). Indeed, it will adhere to a medium-term inflation at 0.6% and a gloomy 2026 activity picture with projected GDP growth of around 1% masking the fact that the underlying picture is more sobering given the circa-0.25 ppt boost sports events will provide this year. But with inflation forecast to be within the confines of its target range of less than 2%, this will be enough to justify stable policy. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur.

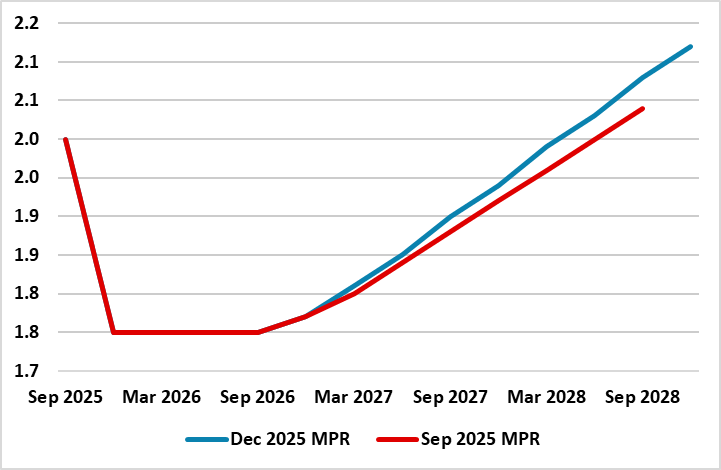

Figure: Riksbank Policy Outlook

It is highly likely that the Riksbank will (again) keep policy on hold with the key rate left at 1.75% when it gives its next verdict. However, what will be more important is what the Board says; explicitly in terms of the recent (less pleasing to it) data flow and, implicitly in terms of updated forecasts in the Monetary Policy Report (MPR). The latter may try and assess the impact of Middle East conflict, but tentatively. But the GDP and CPI outlooks may need to be pruned back after what have been unexpected weak readings for both of late, some of which may be attributable to the recent appreciation of the Krona. The inflation undershoot is modest but as we have suggested repeatedly, the 2.6% Riksbank GDP projection for the year is overly optimistic, possibly by a factor of two. As a result, the Board promise of no change for some time to come is likely to be repeated but with more discernible risks attached in both directions. Regardless, we still do not see any looming policy reversal, as we see this current policy rate (1.75%) staying in place through 2027, ie a little longer than the Riksbank.

For the week ahead

USA

The FOMC meets on Wednesday and is likely to leave rates unchanged, at 3.5-3.75%. In the current uncertainty they are unlikely to leave the assessment of the economy similar to January’s, while recognizing heightened risks. We expect the dots to be unchanged from December, looking for one 25bps easing in each of 2026 and 2027. We expect two dissenting dovish dissents, from Miran and Waller, as was the case in January.On Monday we expect February industrial production to be unchanged with a 0.1% increase in manufacturing. March’s Empire State manufacturing and NAHB homebuilders’ surveys are also due. Tuesday sees pending home sales and leading indicators data for February. On Wednesday we expect a 0.3% increase in February’s PPI, 0.2% ex food and energy. January factory orders are also due. Thursday’s initial claims will cover the survey week for March’s non-farm payroll. March’s Philly Fed manufacturing survey and January wholesale sales are also due, while we expect January new home sales to fall to 740k from 745k. Friday’s data calendar is quiet.

CANADA

On Monday we expect February CPI to fall to 2.0% yr/yr from 2.3% in part because of the ending of a year ago sales tax holiday, though the Bank of Canada’s core rates are likely to be on balance softer. February housing starts are also due on Monday with February existing home sales following on Tuesday. The Bank of Canada meets on Wednesday and is likely to leave rates unchanged at 2.25% and reiterate that the level is appropriate if data evolves as expected, while noting heightened uncertainty and a willingness to respond if the outlook changes. Friday sees IPPI/PMPI data for February, and January retail sales, for which a preliminary estimate was for a 1.5% increase. UK

The coming week sees several important economic updates looming, most notably ever-more important labor market numbers. Apparent wage resilience has perturbed some MPC members but where even the hawks are starting to re-think. But this data release, now encompassing updates not just from the long-standing ONS but also real time figures from the HMRC (which we suggest are more authoritative data and are now officially accredited) is likely to see little further drops in the official earnings data, at least for private sector regular earnings Otherwise, the HMRC numbers are likely to show that employment is continuing to contract and maybe more broadly so as far as the private sector is concerned, while its pay data already suggest a slowing to under 3% has occurred. Friday sees monthly public borrowing numbers which are running below year-before levels. Friday also sees CBI industry survey numbers (Thu).

But the man event is Thursday’s BoE verdict. The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a whole will not have to reveal too much about any shift in policy bias given that it does not have to provide updated forecasts until its May meeting, the individual member views will show continued divides.

Eurozone

Given it relative topicality, there may be more eyes on the German ZEW survey (Tue) and less on what my still be weak EZ industrial production figures (Mon) and construction figures (Thu). Final HICP data (Wed) arrive before trade numbers (Fri). Labor costs data may get some attention but also on Thursday, the main event is the ECB decision. With no change in policy expected, what the ECB says is the most important aspect of the Council meeting, both explicitly and implicitly via its updated forecasts (Figure 1). Both are likely to underscore that rate hikes are certainly possible if the almost inevitable inflation rise proves to be either/both significant and/or persistent. But no time frames will be suggested, this papering over what are long-standing splits within the Council regrading policy.

Rest of Western Europe

There are a key events in Sweden, most notably the Riksbank decision on Thursday. It is highly likely that the Riksbank will (again) keep policy on hold with the key rate left at 1.75%. However, what will be more important is what the Board says; explicitly in terms of the recent (less pleasing to it) data flow and, implicitly in terms of updated forecasts in the Monetary Policy Report. Switzerland also has a central bank meeting (Thu) and where once again and in line with consensus thinking we see SNB policy being unchanged with little shift in the forecast for either growth or inflation. Admittedly, the tone of the economic outlook will be more guarded but where it will be underscored that it is too soon to make material changes to the outlook given current heightened uncertainties. The strong Swiss Franc will be mentioned but its current strength needs context. Otherwise Thursday also sees the Norges Bank release it regional survey.

JP

The BoJ Interest rate decision is on next Thursday where we expect no change to the current rate, given the ongoing spring wage negotiation. Market expectation is for an earliest April/May hike. Which has likely been delayed by U.S.-Iran military operation. Else, we also have trade balance on Wednesday.

AU

RBA interest rate decision in on Tuesday. Some hawks are speculating an imminent hike to address the rising energy cost but we think it may be a step too soon for the RBA only see two more hikes in 2026. It will be a hawkish surprise if we see one. Labor data will be released on Thursday but likely seizing less attention.

NZ

Business PSI on Monday and trade balance on Friday.

Recap for the week

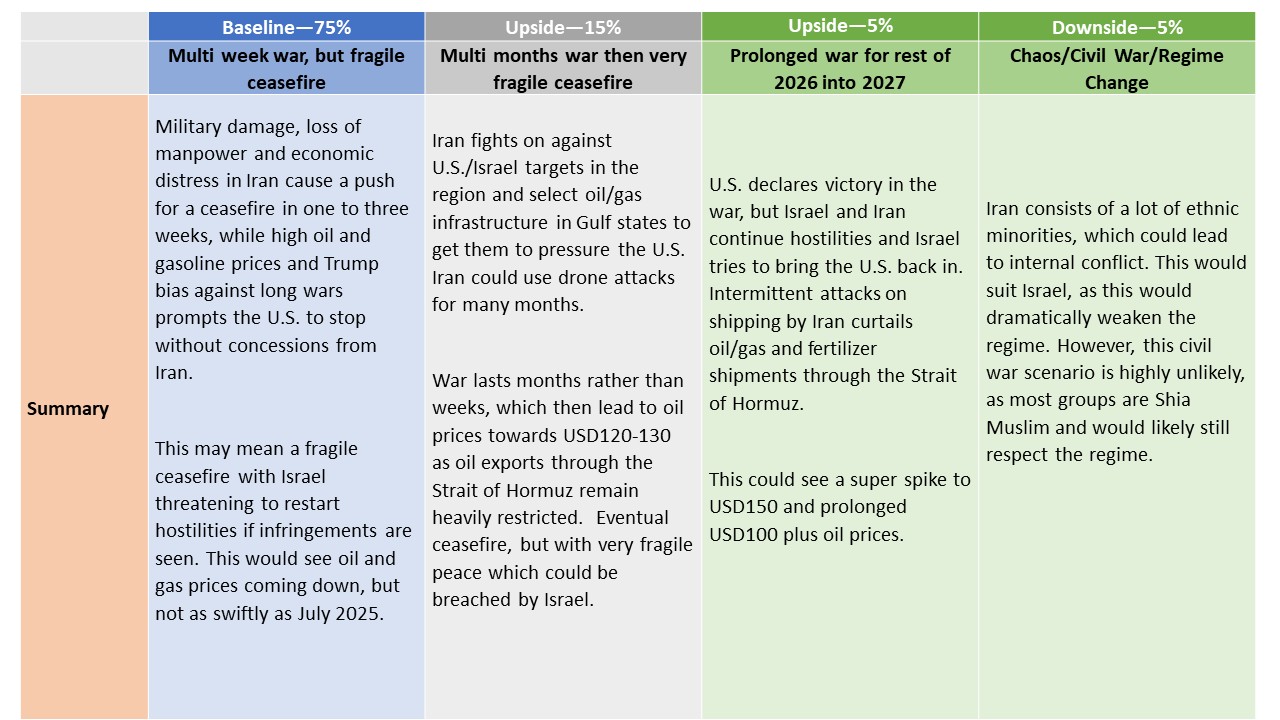

Iran War Scenarios

U.S. February Core CPI has slowed, but inflation not yet defeated

UK GDP More Gloom

DXY Fresh year highs

USD/JPY At intervention Level

Our central scenario (75%) remains a multi-week war in Iran. Trump loathing of long wars and high gasoline prices prompts U.S. to declare victory before end of March. Israel and Iran would most likely agree an effective ceasefire. The ceasefire would be fragile, however, as it would likely not involve concessions from Iran’s new hard-line leader, while potential Israeli hostilities could breach the ceasefire. We would see WTI at USD80-85 by April and USD70-75 by June. The main alternative scenario is a multi-month war (15%), which could squeeze oil prices up to USD120-130.

With war in an intense phase, a lot of uncertainty exists over likely outcomes. However, in one to two more weeks, the damage to Iran’s missile and offensive capabilities will likely mean that initial military objectives could be partially or fully achieved. We highlight below a number of scenarios that could occur, with some broad estimate of probability – with the understanding that these will likely change based on decisions in Iran/U.S. and Israel.

February CPI is in line with expectations at 0.3% overall, 0.2% ex food and energy, with the respective gains before rounding being 0.267% and a reasonably subdued 0.216%. Yr/yr rates are unchanged at 2.4% overall and 2.5% ex food and energy. The data is not alarming but inflationary pressures remained above target even before the latest oil price spike. Energy rose by 0.8% with gasoline up by 0.6% with a strong rise looking assured in March. Within the energy detail there was also a surge of 11.1% in fuel oil after a 5.7% January decline. Food was on the firm side of trend, rising by 0.4%.

Commodities less food and energy rose by 0.1% after two flat months. Used autos remain a restraint but less so, falling by 0.4% after declines of 1.8% in January and 0.9% in December. Apparel saw a strong month at 1.3% but information technology commodities fell by 3.1%.

Figure: GDP Growth Hardly Strong and With Increasing Downside Risks?

Fresh downside surprises were the story from the January GDP numbers. Expectations that the economy would enjoy a further successive rise, thereby providing the best three-month showing in two years were dashed as GDP instead stagnated. Weakness was broad-based but most evident in private services and in spite of a bunce in retailing. But as is familiar with recent UK real economy data, it now looks more likely that growth this quarter will be no better than the 0.1% q/q seen in Q4, less than consensus and BoE thinking for this quarter. Moreover, there may be downside risks as activity and sentiment will, of course, be hit by events in the Middle East. Even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture of 0.8% which now has even greater downside risks attached.

Minor consolidation around 99.75 has given way to anticipated gains, with the break above 100.00 posting fresh 2026 year highs just beneath critical resistance at the 100.40 monthly high of 21 November. Daily readings continue to rise and broader weekly charts are positive, highlighting room for still further strength in the coming sessions. A close above 100.40 will confirm a significant low in place at the 95.55 current year low of 27 January, and extend late-January gains towards resistance at congestion around 101.00 and the 101.15 multi-month Fibonacci retracement. Already overbought daily stochastics could limit any initial tests of this range in profit-taking/consolidation. Meanwhile, a close back below 100.00 would help to stabilise sentiment and prompt consolidation above congestion around 99.50.

USD/JPY continue its rally on stronger USD amid geopolitical uncertainty. As the pair quickly approaches 160 figure, verbal intervention surfaces expectedly. Japan Finance Minister Katayama signaled readiness to act in foreign exchange markets if necessary, a classic rhetoric of jawboning.

Break above the 158.90 high of Monday has seen gains to retest 159.45, January current year high. Positive daily and weekly studies keeps pressure on the upside and suggest scope for break here to further extend gains within the bullish channel from the April low. Clearance will see scope to target the 160.00 figure where reaction can be expected. Meanwhile, support is raised to the 158.00/157.65 area which should underpin. Would take break here to fade the upside pressure and retrace gains from the 152.27/152.10 February/January lows.