Preview: Due May 28 - U.S. April Personal Income and Spending - PCE Prices to underperform CPI

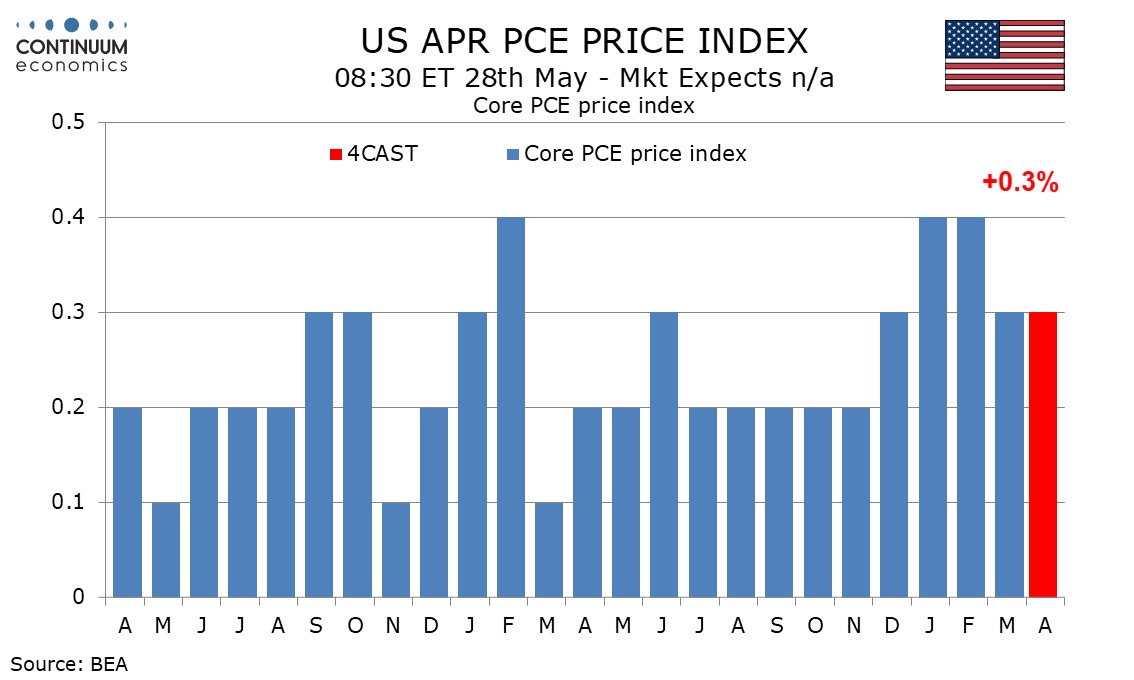

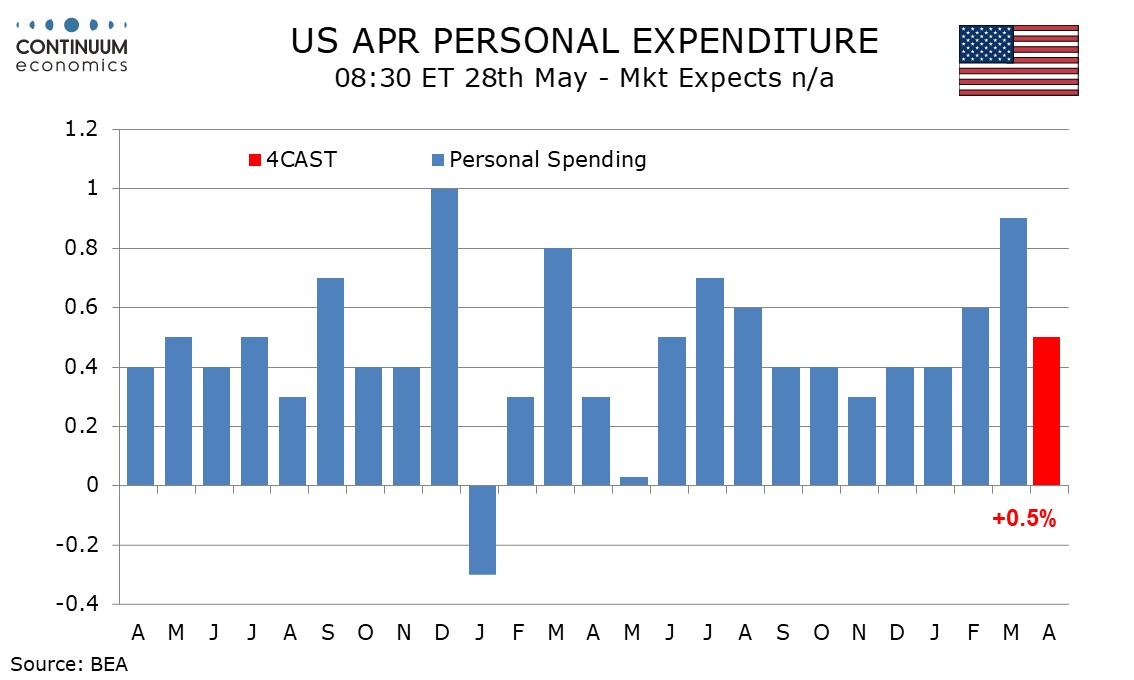

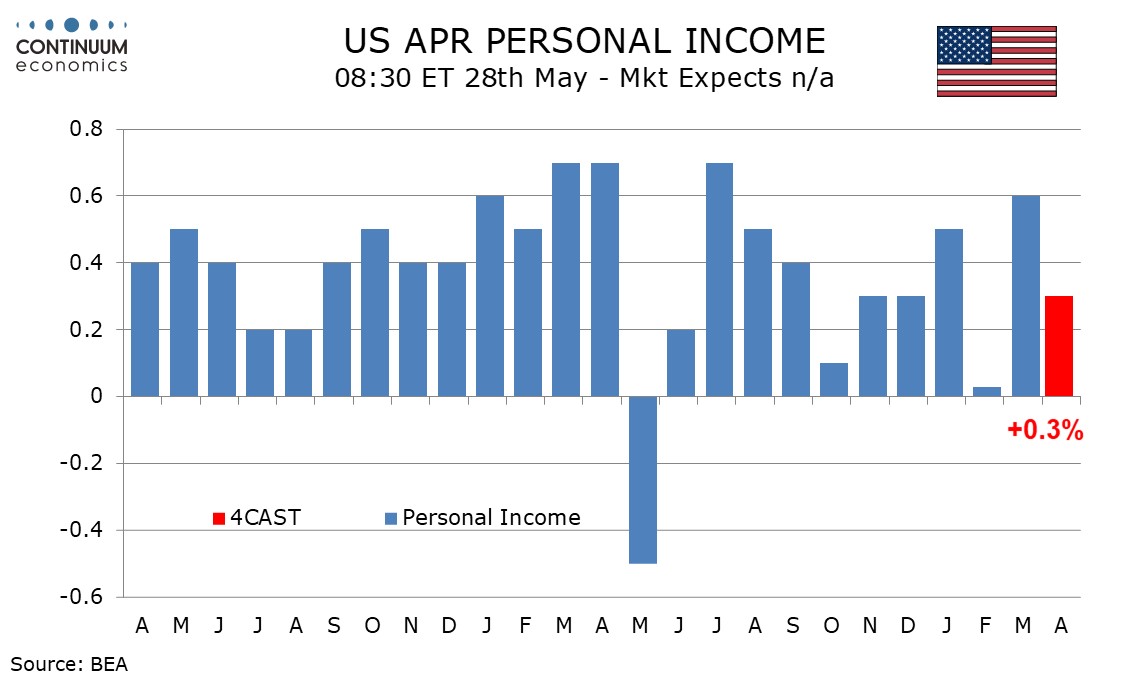

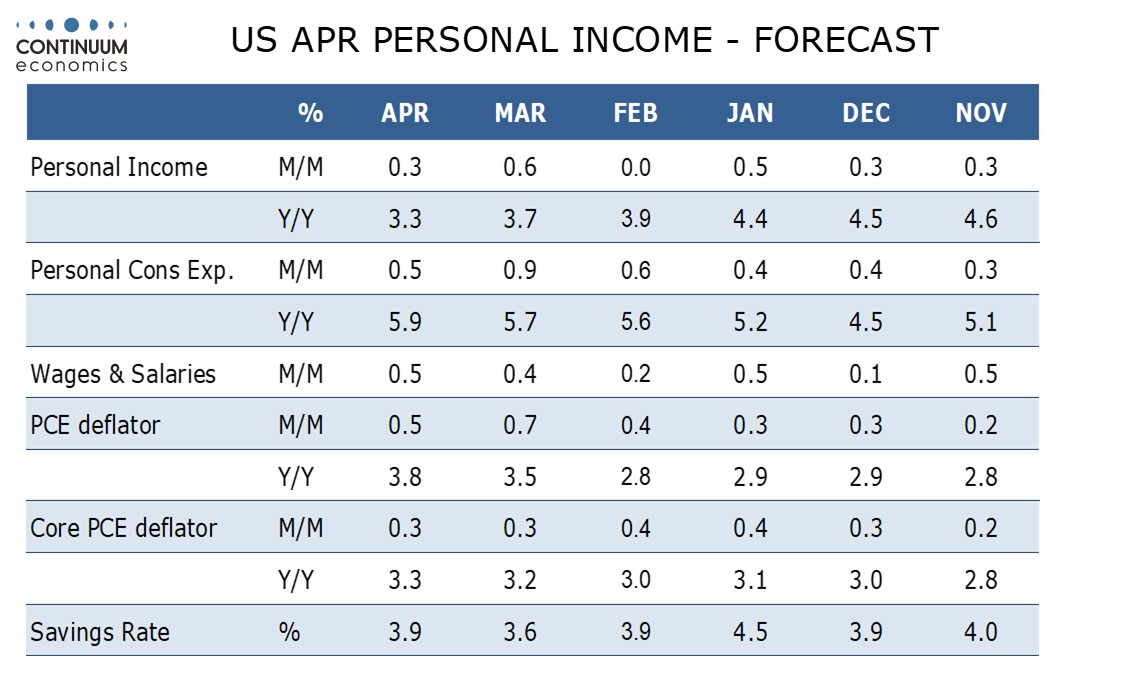

We expect April’s core PCE price index to rise by 0.3%, with overall PCE prices up by 0.5%, both slightly below respective CPI outcomes of 0.4% and 0.6%. We expect a 0.3% rise in personal income to underperform a 0.5% rise in spending, but due to lower taxes disposable personal income may outperform spending.

Core PCE prices rise by 0.38% before rounding but was inflated by a one-time distortion in housing related to the October shutdown missing a 6-monthly update, inflating April’s data through catch-up. This distortion should have less impact in the PCE price data. Overall CPI rose by 0.64% before rounding, but gasoline tends to have less impact in PCE price data than it does in the CPI. Despite a strong April PPI, the components that contribute to PCE prices did not lead the increase.

Overall PCE prices would then rise to 3.8% yr/yr from 3.5% in March, reaching the strongest pace since May 2023. The core rate would edge up to 3.3% yr/yr from 3.2%, reaching its highest since November 2023 and moving further away from the Fed’s 2.0% target.

Retail sales rose by 0.5% in April, and we expect a similar rise in services, though most of that will be explained by higher prices, as will also be the case in retail sales. In real terms we expect consumer spending to be unchanged.

A healthy non-farm payroll breakdown on the workweek and employment, even with slowing in average hourly earnings, suggests a 0.5% rise in wages and salaries. However we expect the other components of personal income to underperform after a March outperformance which owed a lot to a bounce in farm income that is unlikely to be repeated.

April’s budget statement showed income tax revenues down on a yr/yr basis for the first time since October 2024, with larger tax refunds following tax cuts passed in 2025. We expect disposable income to rise by 0.7%, with real disposable income up by 0.2%. This would lift the savings rate to 3.9% from 3.6%, erasing a March decline.