U.S. June CPI - Very soft, even if a few components look erratic

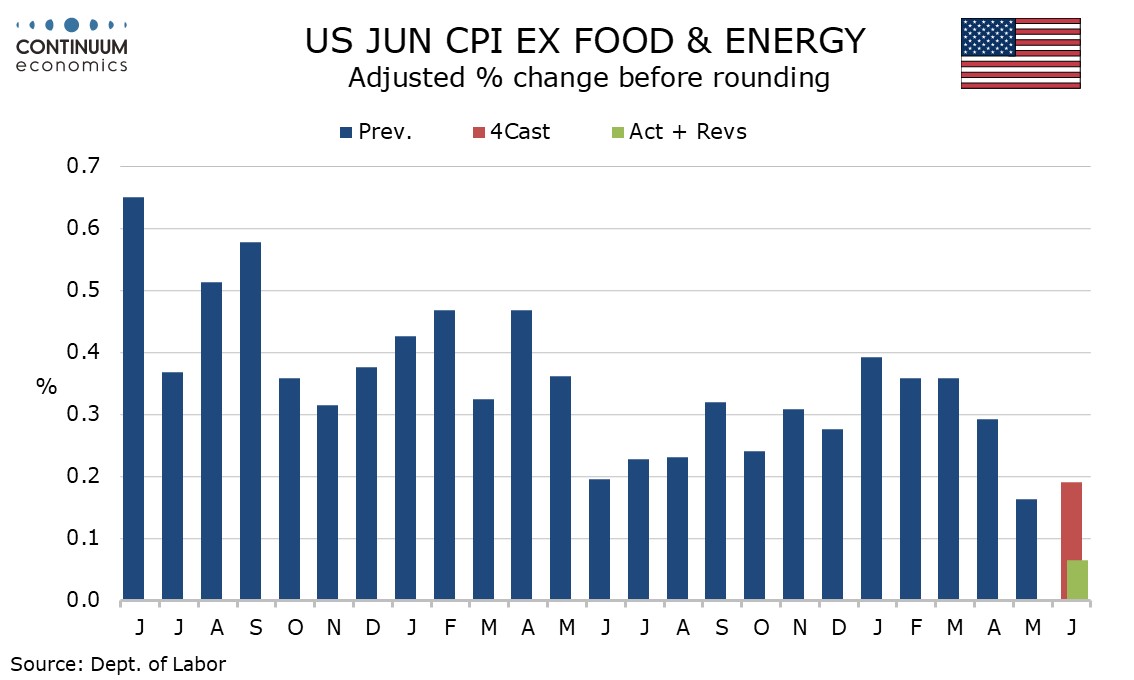

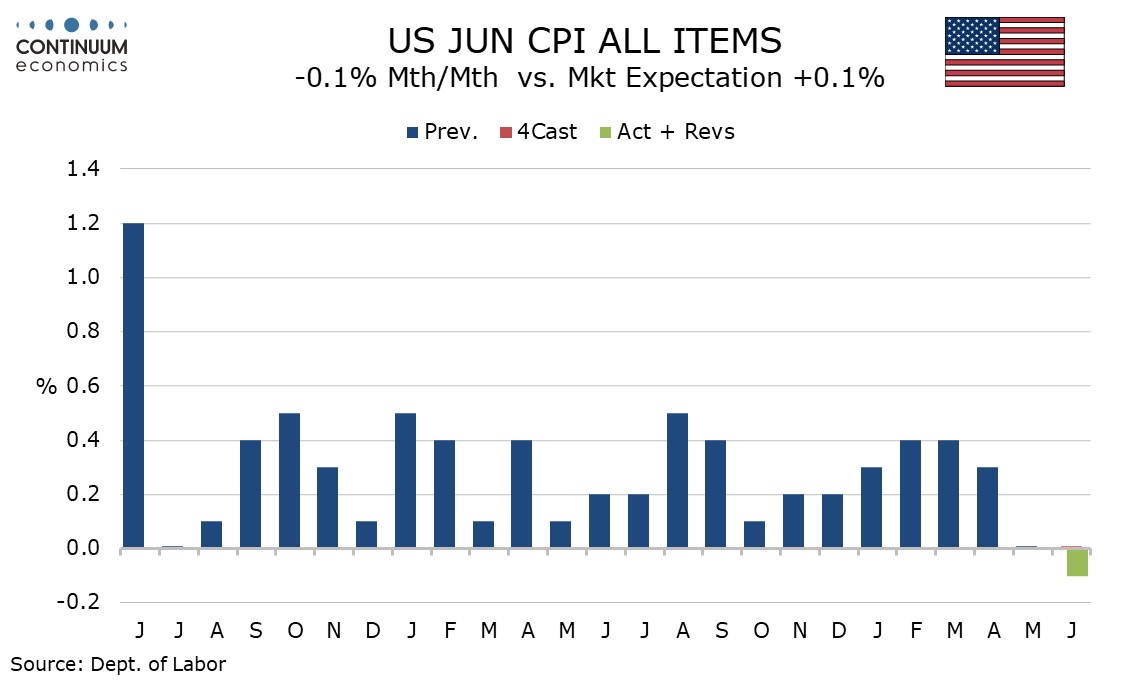

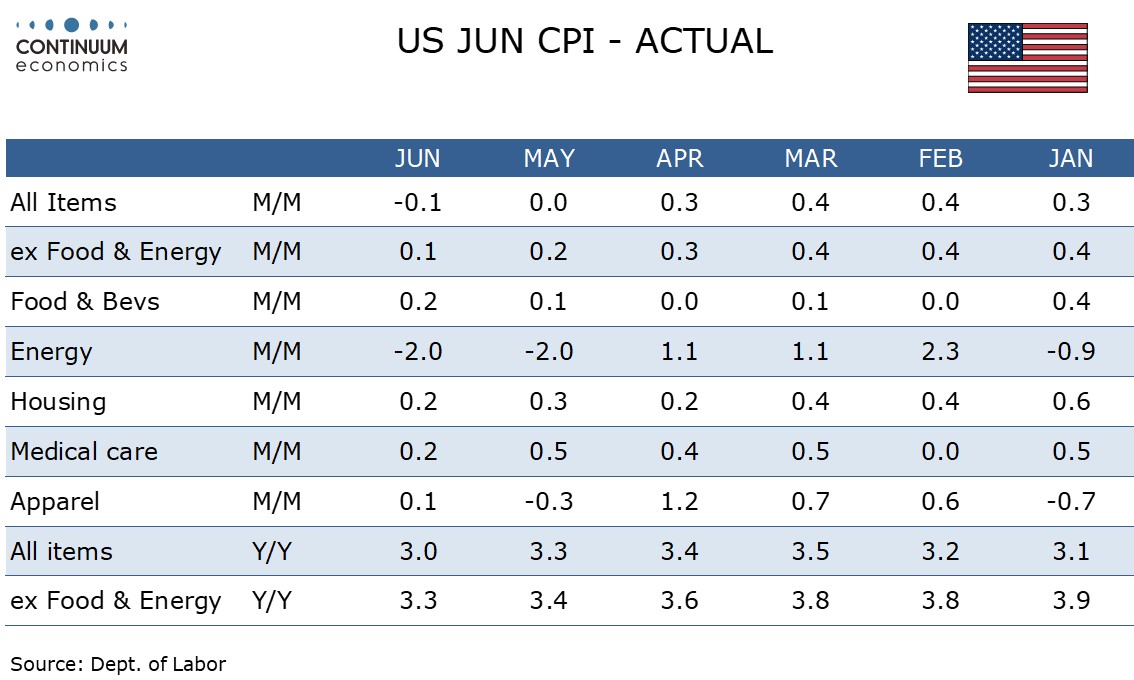

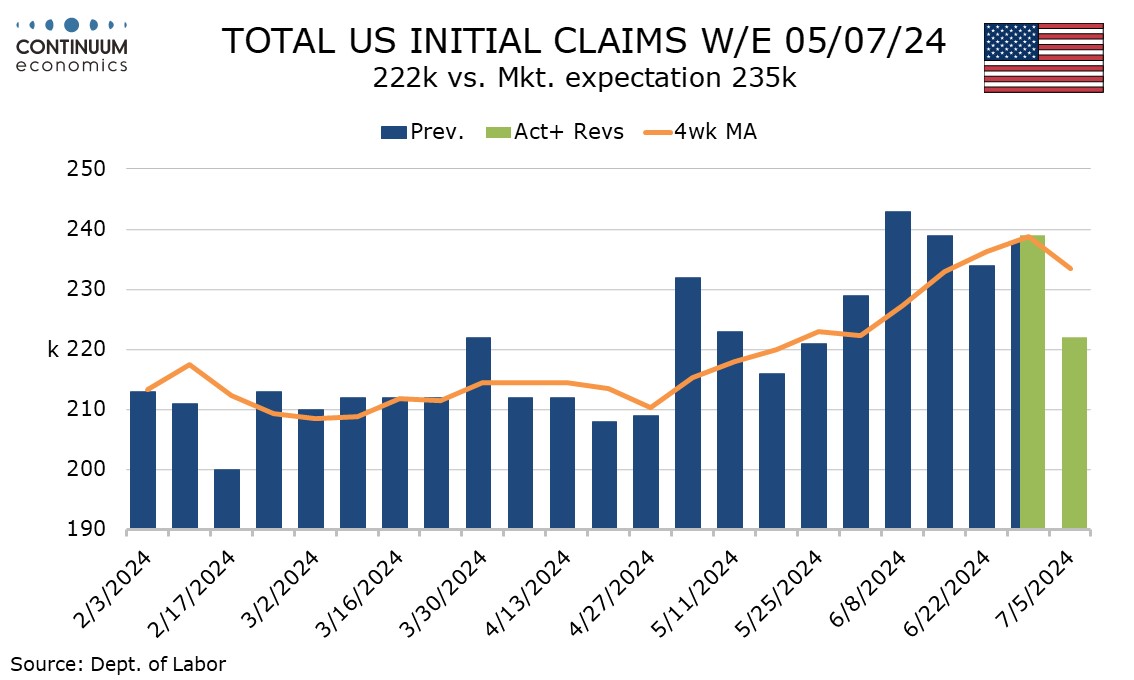

June CPI is even weaker than expected, down by 0.1% overall and up by only 0.1% ex food and energy, with the core increase before rounding only 0.065%, a sign that inflationary pressures have faded significantly since the bounce at the start of the year. Initial claims at 222k from 239k suggest the labor market remains strong, but the 4 July holiday may have flattered the data.

Core CPI was quite strong at the start of 2023 before fading later in the year, so there may be some residual seasonality not fully compensated for by seasonal adjustments. June was the softest month of 2023 for core CPI, though its gain of 0.195% was significantly stronger than the latest month which is the slowest since January 2021.

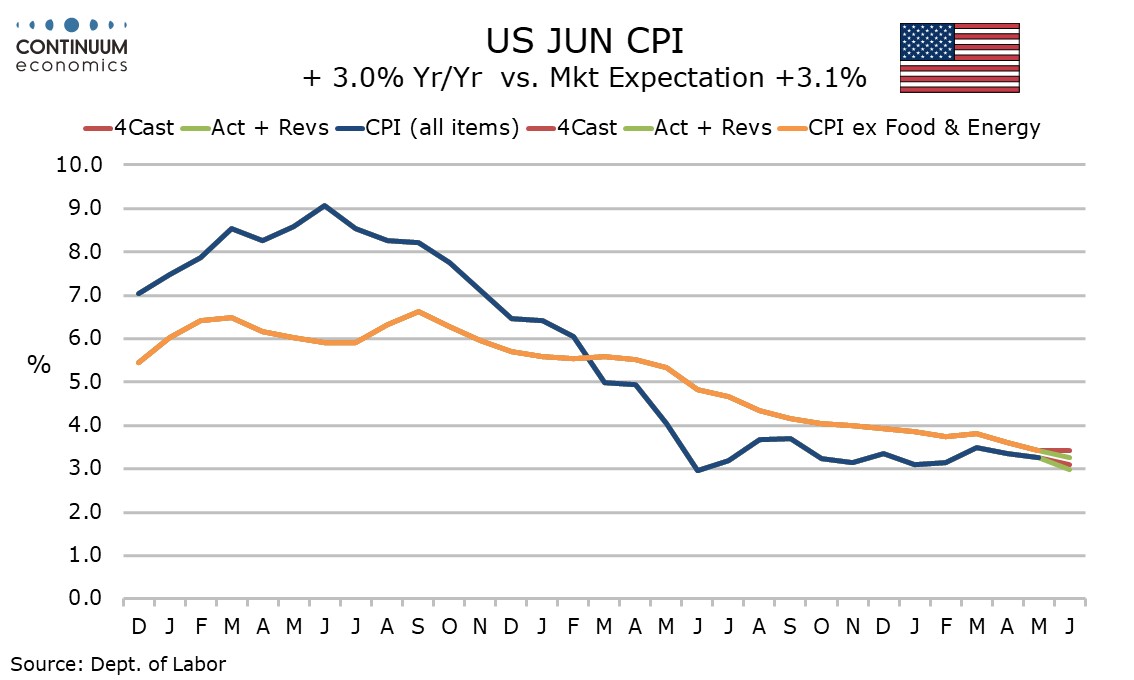

Yr/yr core CPI slowed to 3.3% from 3.4%, to its slowest since March 2021 while overall CPI fell to 3.0% from 3.3%.

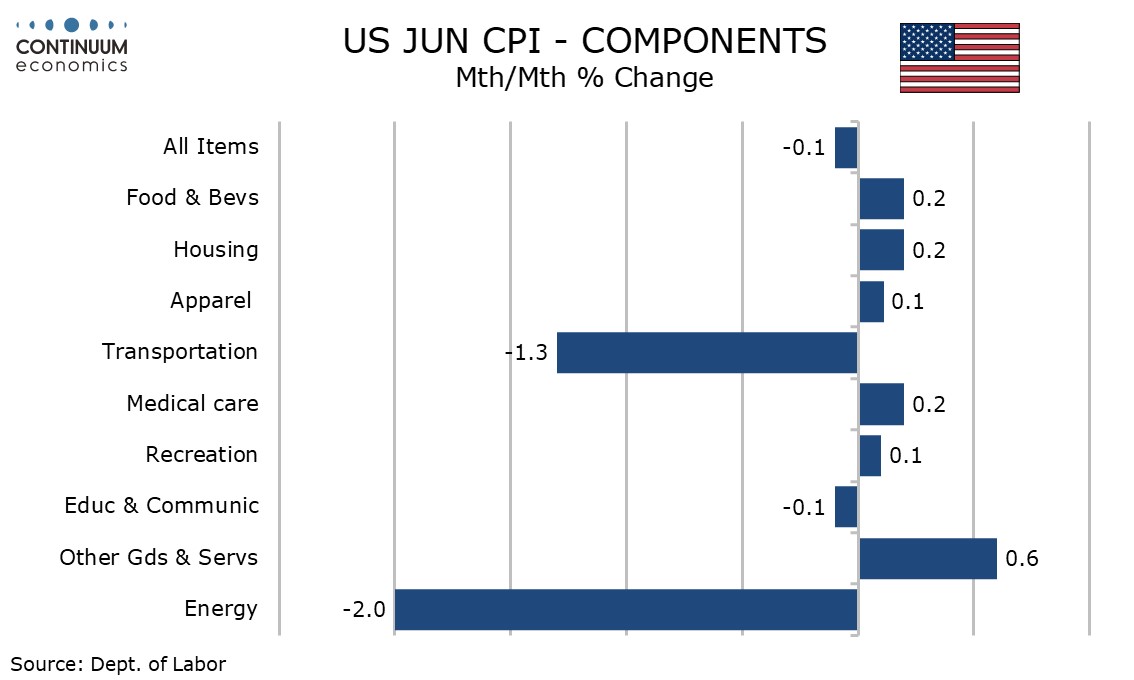

Energy saw a second straight decline of 2.0% led by gasoline while food saw a modest rise of 0.2%. Commodities ex food and energy maintained recent trend with a fall of 0.1%, with used autos patricianly soft at -1.5%.

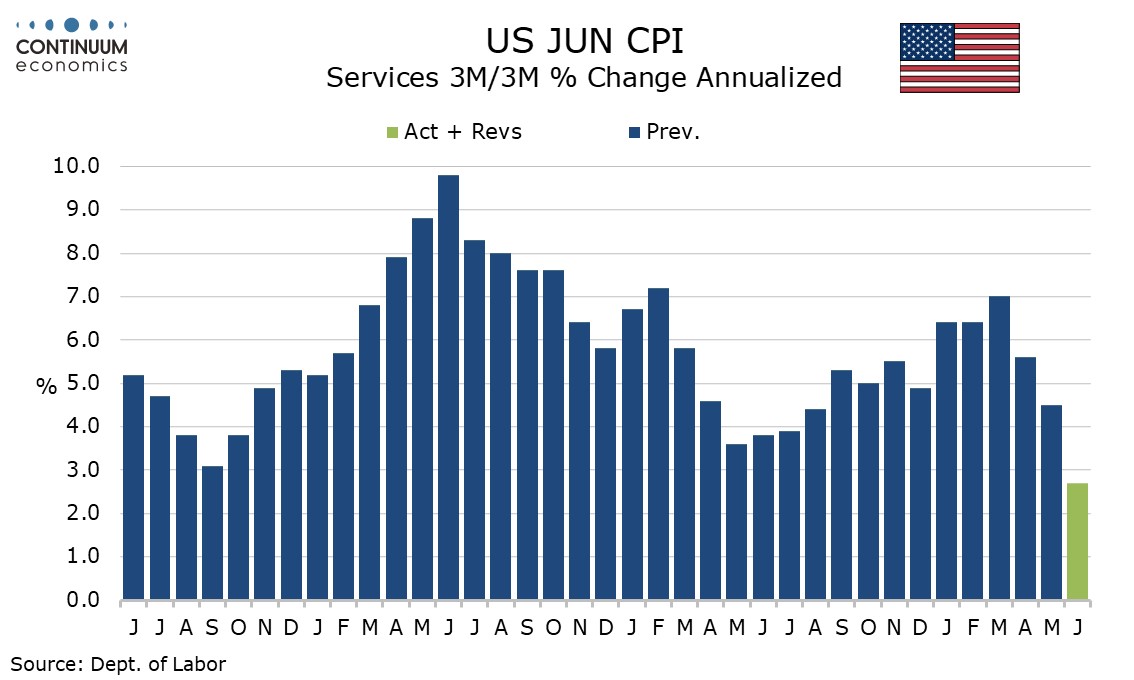

Services less energy, which were strong in the first four months of the year, followed May’s slower 0.2% gain with even slower rise of 0.1%. Transportation services saw a second straight 0.5% decline in a continued reversal of early year strength led by a 5.0% fall in air fares that looks like feed through from lower energy prices.

Shelter rose by only 0.2% with a 2.5% fall in lodging away from home looking a little erratic, though owners’ equivalent rent slowed to 0.3% after four straight months of 0.4% and the heavy weight of this components makes the slowing significant.

While there seem to be a few components that are erratically weak, the data is soft enough to suggest an underlying picture consistent with on target inflation, though the Fed will want to see more soft data before easing. Still, even data slightly less soft than this month would be satisfactory for the Fed.

The lower initial claims data may prove to be erratic, but even if not Powell’s recent assessment that the labor market while strong is not overheating suggests that the data will not be an obstacle to easing if we see further soft CPI data.

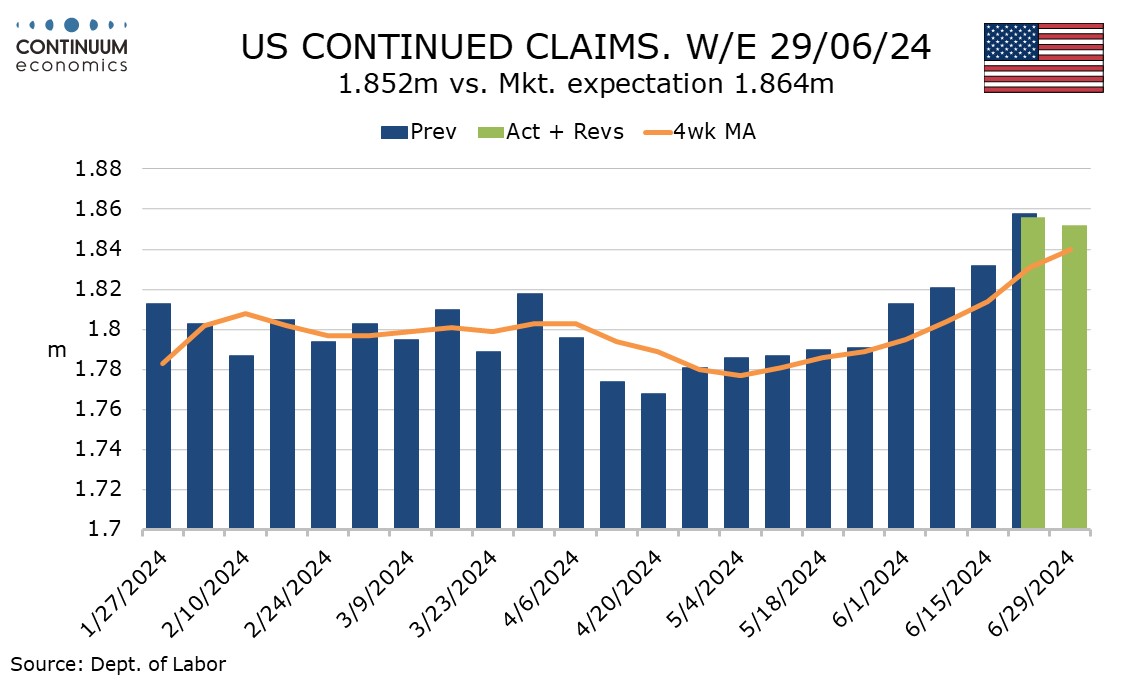

Continued claims at 1852k from 1856k are also softer than expected, seeing a first fall in 10 weeks, but after a 24k rise that was the largest of nine straight gains. Easing in September looks plausible if data allows, even if July is still highly unlikely.