UK GDP Preview (May 10): Fragile Sideways-Moving Activity Continues?

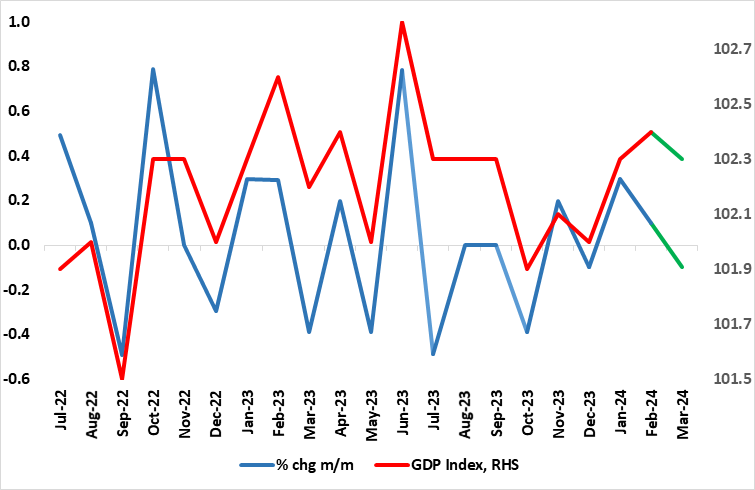

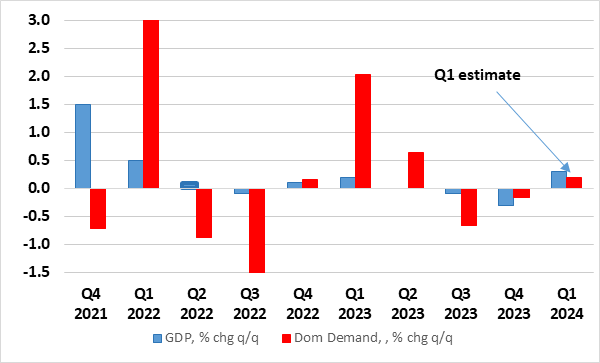

The economy may have been in only mild recession in H2 last year, but the ‘recovery’ now evident is hardly much better with GDP growth only modestly positive. Admittedly, coming in as largely expected, and despite industrial action, GDP rose by 0.1% m/m in February accentuating the upgraded 0.3% bounce in January data, a result that nevertheless is nothing more than a continuation of the monthly swings seen of late, which means that y/y growth is still negative. Admittedly, unseasonable weather may have played a part in hampering February activity, most notably in construction and it is noteworthy that the 3 mth rate tuned positive in February for the first time since last summer. Regardless, the modest added momentum so far in Q1, and despite what we think may be a 0.1% m/m March contraction (Figure 1), suggests that the last quarter may still see GDP growth of 0.3% q/q (Figure 2), higher than BoE thinking and fully reversing the slide and continued mild recession in Q4 last year.

Figure 1: Tentative Recovery – Output Still Moving Sideways?

Source: ONS, CE, green lines are CE estimates

A Mixed March Message?

This, alongside some better business survey readings, may be something that the BoE hawks use as a rationale to argue for no near-term rate cut, even though this may add to effective debt servicing costs facing consumers. However, even if Q1 GDP repairs the Q4 drop and ends the formal but mild recession, any hawkish thinking may be tempered should GDP correct back in March as we think is distinctly possible. Indeed, this would imply a continuation if what has been sideways moves in GDP trend-wise! Retail sales data for March will not support further GDP gains, although the modest recovery in the housing market, most notably emerging signs of a recovery in transactions may do so, even for these looming March GDP numbers. But we think there will be telling slump in vehicle production given what industry data suggests and that this may be accompanied by the wet weather hitting construction. Indeed, the warm weather in March may also negatively affect utility output, and there are reasons to think that public sector activity may continue to slow – it having been a clearly positive factor in supporting GDP in recent months.

More notably, unless there is clearer early-year momentum builds, and after all y/y growth in March may be barely positive, the economy is still likely to grow this year by no more than 0.3%, a result that chimes with existing BoE thinking, which is being shaped more by price and costs developments not real activity.

As for recent details, GDP is estimated to have grown by 0.2% in the three months to February 2024, compared with the three months to November 2023. Services output was the main contributor, with a growth of 0.2% in this period, while production output rose by 0.7% and construction fell by 1.0%. Perhaps the most striking feature was the large and broad based rise in manufacturing, this clashing with business survey messages. Electricity, gas steam and air conditioning supply also contributed positively, with a 1.2% growth in this period, these probably having been hampered through the month by the very mild and wet weather; the warmest February on recent record in England.

Figure 2: Recession Ends as Domestic Demand Bounces?

Source: ONS, CE

Overall, even with the small March fall we see, GDP is likely to have seen a 0.3% q/q rise, albeit this subject to what extent revision materialize. Within this consumer spending may show its forts rise in three quarters and domestic demand may also recover (Figure 2).