Norges Bank Preview (Aug 15): Less Hawkish?

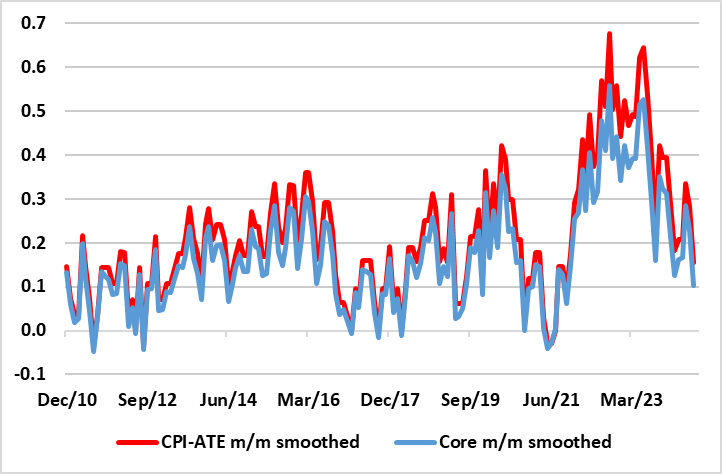

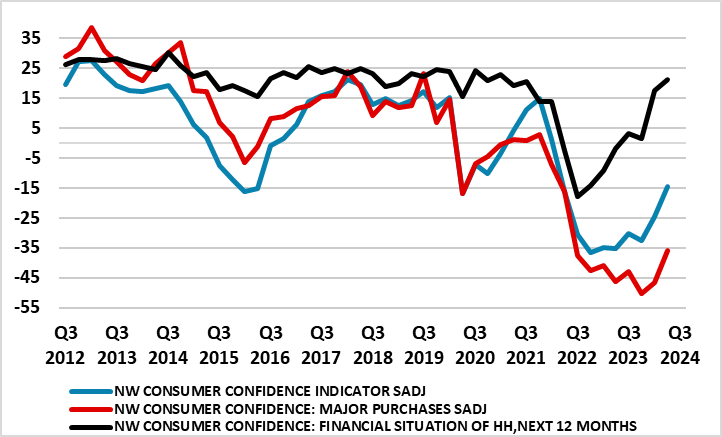

Given its recent rhetoric and currency concerns, and in spite of current stock market gyrations, the Norges Bank is very likely to leave its policy rate at 4.5% for a fifth successive meeting next Thursday, the last hike to the current 4.5% policy rate occurring last December. But amid what have been softer than (Norges Bank) expectations for CPI data of late, the question is whether the Board will tone down its hawkish leanings and perhaps depart from its recent stress of ‘policy to stay on hold for some time ahead’. Last time (in June) this was backed up formally with an updated policy outlook that foresaw no rate cut until early-2025, some three months later than considered previously. With no formal projections due until the September Board meeting, any such change in thinking this month may be more implicit than explicit, but would take account of CPI data that suggest adjusted m/m core readings are now consistent with clearly-below target inflation (Figure 1) as well as still fragile consumer thinking (Figure 2). We still think continued inflation weakness in coming months as weaker profit margins offset labor costs issues will deliver at least one cut by end-year and maybe over 100 bp in 2025!

Figure 1: Core Adjusted Inflation Below Target

Source: Stats Norway, CE, smoothed is 3-mth mov avg

The Norges Bank decision will be the first DM central bank meeting since the onset of last week’s stock market correction. It will be interesting to a) see how the Board regards this in terms of any repercussions for Norge Bank policy and b) whether the Board details if and how much conversation this has triggered with other central banks.

Otherwise, existing Board projections see a slightly softer rate at the end of the forecast horizon, the question being whether this (at around 2.7%) is seen being a terminal or even neutral rate. Regardless, against a backdrop of continued currency weakness, and a recovery in house prices, the Norges Bank Board has almost disregarded the size and cause of the recent inflation undershoot, instead preferring to focus on what it says is a perkier real economy, possibly in the hope that this may bolster sentiment in the FX market regarding the currency. Indeed, in June it revised the GDP picture markedly for this year but made modest changes from 2025 onwards, still largely preserving a negative output gap. As for the currency, the Board may start to be less concerned given that the CPI drop actually reflects a marked easing in imported inflation, this having dropped five full ppt to 1.5%.

Indeed, as for inflation, we think the Board has underestimated the extent to which it has retreated of late on an underlying basis, this very much evident in seasonally adjusted data, for various core measures; we have computed a core measure in which food is excluded from the familiar CPI_ATE figure. Both this core and the CPI-ATE measures show recent seasonally adjusted m/m dynamics now to be running at pace nearer 0.1% per month, ie consistent with the 2% target being undershot (Figure 1). And this is in spite of the impact of rental inflation (around 17% of the CPI) running still at over 4% y/y, implying headline inflation ex rents now at 2.5%. This begs the question whether Norges Bank policy is actually buttressing inflation as higher interest rates therefore mean higher inflation as rents are largely being driven by (high) mortgage rates. Moreover, the resilience in rents may help explain the puzzling manner in which consumer confidence has developed of late, ie where households perceive a better financial position but are not willing to consider spending more (Figure 2)

Figure 2: Consumer Caution Continues

Source: Stats Norway, % balance

Even so, a weaker currency, slightly stronger growth, a recovering housing market and more generous pay settlements than expected are all factors that will be playing on the minds of the ever-cautious Norges Bank, clouding any assessment that even y/y inflation had been slightly lower than officially expected. Indeed, the Board may be swayed by its latest regional survey where the contacts concerned reported that full capacity utilization has increased and contacts also revised up their wage growth estimates for 2024 and 2025 to 5.2% and 4.3%, respectively

We are wary about the apparent recovery in activity, not least given the impact of what has been unseasonable weather patterns amid monthly GDP data that have been suspended and thus leave something of a hole in assessing the economy. Regardless, amid an economy with a tight labour market and rapidly rising wages but low productivity growth, the Board may very well worry about inflation persistence, certainly on the costs push side. With this in mind, the Norges Bank was the first DM central bank to start hiking; it clearly has not wanted to be the first to start easing and it may instead be among the last as it confronts what is sees is the ‘last mile’ problem!