Norges Bank Preview (May 7): A Close Call?

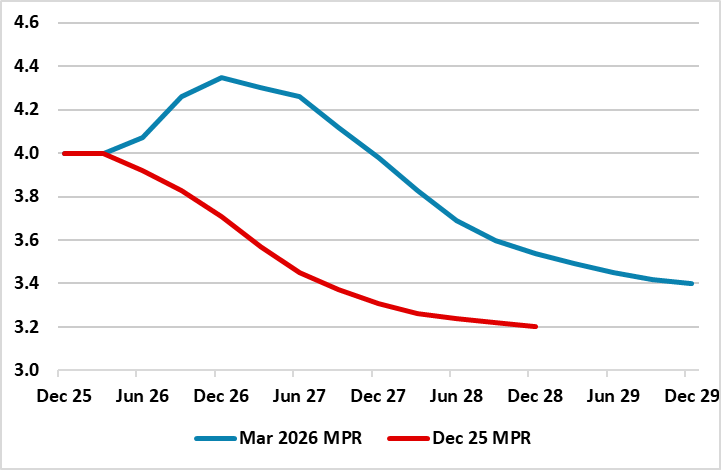

The next Norges Bank decision next Thursday will be a close call, not least after the clear pointer from the Board in March that at least one rate hike looms in the next couple of months. While we acknowledge the hawkish and active manner of the Board we adhere to a stable policy decision outlook for this month, not least given the similar verdicts its neighbouring central banks already offered by then. We think that the inflation persistence argument, that actually prevented faster easing before the Middle East conflict broke out, are overdone (Figure 1) and that even with no hike at all, the current Norges Bank policy stance is very restrictive – even on its own assessment with the current policy rate of 4% some one ppt-plus above neutral. Admittedly, the Norges Bank is suggesting any hike may be short-lived – something we would agree with if its hawkishness turns out to be more than talk!

Figure 1: Revised Norges Bank Policy Outlook

Source: Norges Bank March MPR

While no change in policy was expected from the Norges Bank’s verdict last time around (ie March), the clear shift in rhetoric from the Board was almost inevitable. It dropped its previous repeated assertion that ‘the policy rate will be reduced further in the course of the coming year’ and instead suggested that ‘the policy rate will likely be raised at one of the forthcoming meetings’. Its forecast implied that this would entail one or two 25 bp hikes but that these will be short-lived with the policy rate coming down afresh from early next year (Figure 1), this questioning the need for such a temporary measure other than to underscore hawkish reputation. We would not exclude the Norges Bank from exercising this bias and maybe even as soon as this month even amid what it terms the uncertainty surrounding oil and gas prices is unusually elevated. But we feel the Board is being excessively hawkish and not just on account of the stronger currency seen of late.

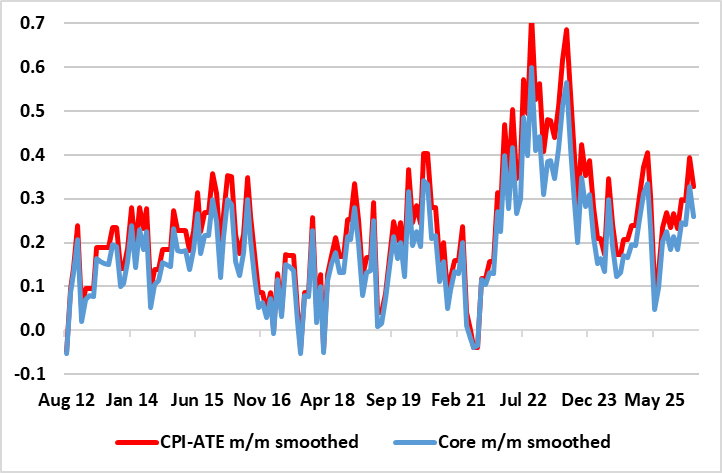

Indeed, this clear warning of hiking is premature to say the least – NB the softening in house prices now emerging is very probably a reaction by households to the reining in of rate cut expectations in recent months, ie prior to the outbreak of the war in Iran, let alone the hiking warning. Moreover, the updated Norges Bank forecasts show an even greater output gap emerging and surely this will have more impact in reining in any inflation surge than one or even two 25 bp hikes. Moreover, we question the extent to which the inflation upgrades are realistic with CPI-ATE now seen averaging 3.3% this year and 2.8% next, some 0.6 ppt and 0.4 ppt higher than envisaged three months ago. Some of the upgrade to this year is due to the apparent fact that CPI data have been higher than expected, but is this an indictment of the Board’s forecasting as despite its assertions to the contrary underlying inflation has been reasonably well behaved.

Figure 2: Underlying CPI Inflation Actually Well Behaved

Source: Stats Norway and CE – Core is ex food and energy, 3-mth % chg m/m, seas adj

Indeed, underlying inflation short-term dynamics are far from unfriendly (Figure 2) especially if food is excluded from the targeted CPI-ATE measure. and with seemingly downside economy risks materialising, we still think that the Norges Bank has already been far too cautious as its updated plans point to keeping policy very restrictive through the projected timeframe out to 2029, ie the policy rate stays well above 3%. For some time, we have argued that Norges Bank’s fixation with apparently resilient inflation was overdone, resulting in overly cautious policy-making, the latter also fixated by the exchange rate.