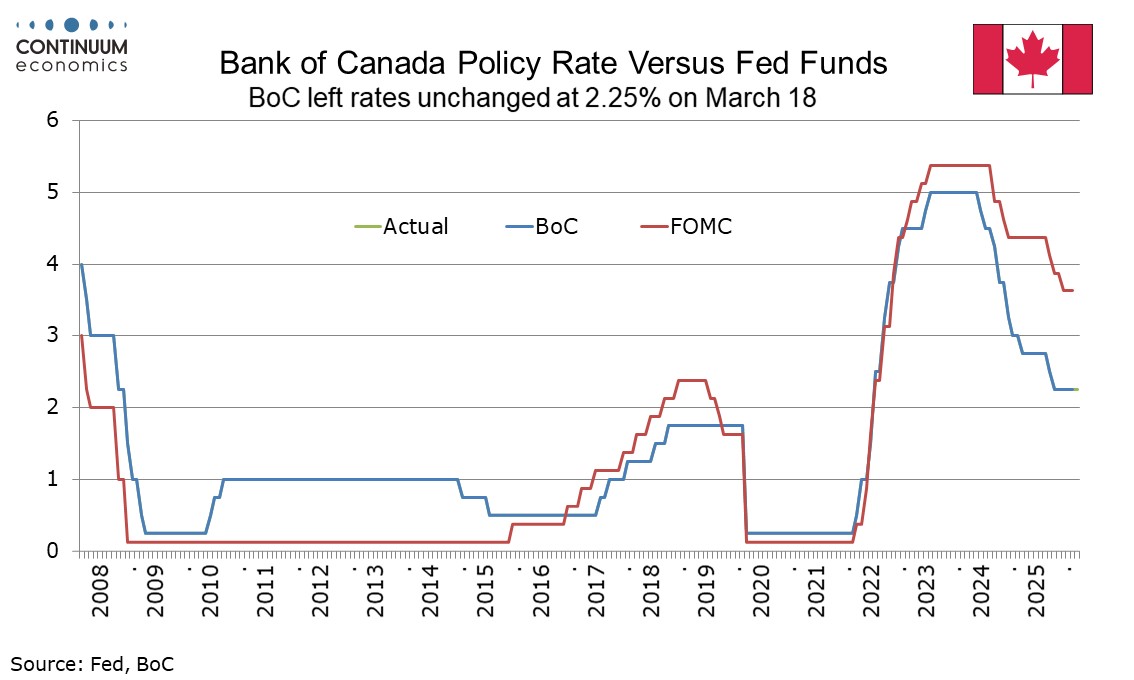

Bank of Canada - Uncertainty Heightened Further but a Dovish Leaning

The Bank of Canada left rates at 2.25% as expected, but with uncertainty heightened still further removed from its statement a reference to the current policy being appropriate provided the economy evolves as expected. Uncertainty on policy has increased too. However, the BoC has taken a more dovish view of the Canadian economy, and we no longer expect the BoC to tighten this year.

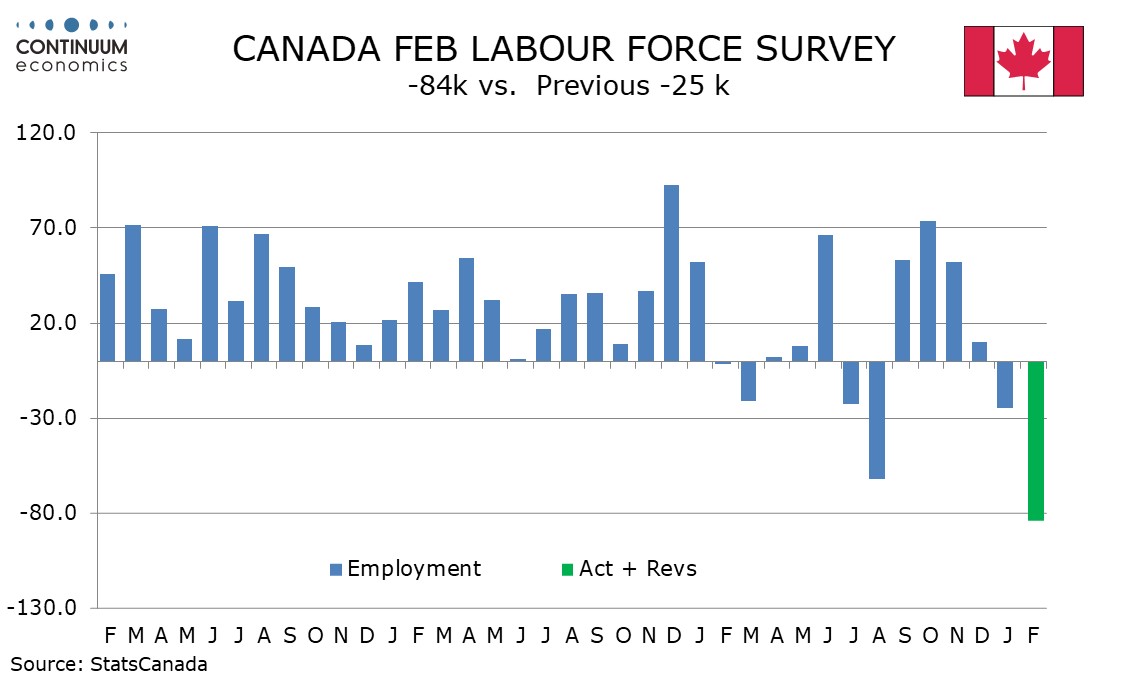

Even in January the BoC stated that uncertainty was heightened, with US trade policy then its main sources. Governor Macklem stated the Iran war has added a new layer of uncertainty, with its breadth and duration seen by the BoC as highly uncertain. The BoC did downplay a weaker than expected 0.6% annualized decline in Q4 GDP, seeing that as largely due to inventory depletion, but added that recent data suggests than near-term growth will be weaker than anticipated in January. With both January and February having delivered significant declines in employment, they noted that the labor market remains soft, showing that the downgrade on the economic view comes from recent data not risks generated by the war.

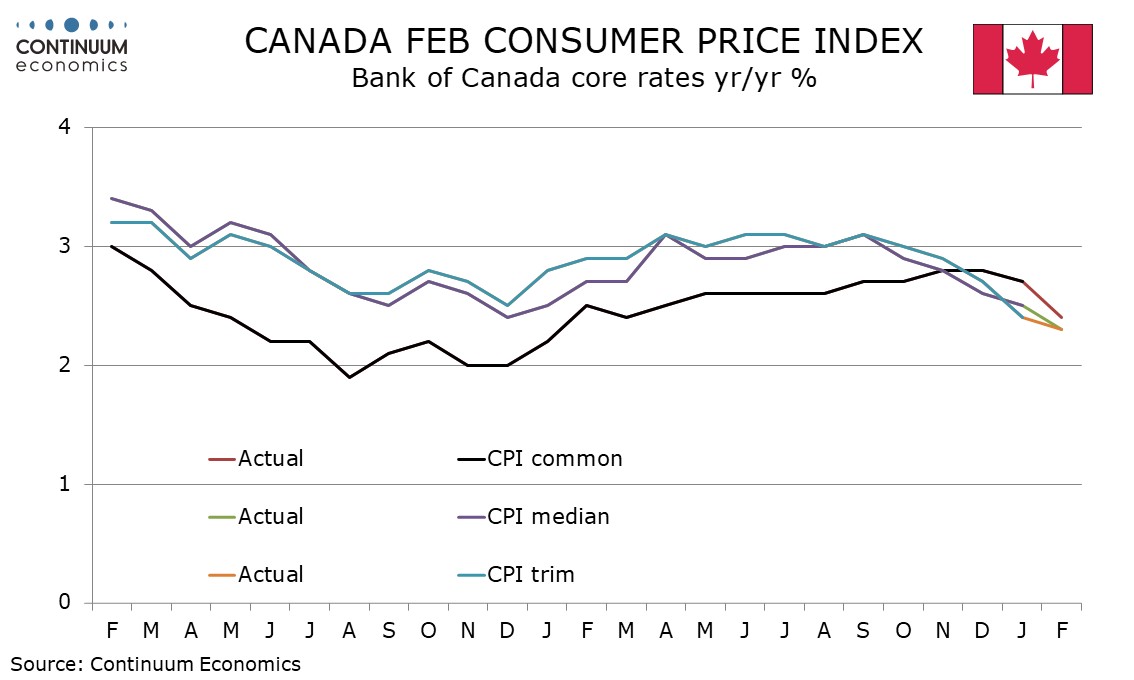

Inflation risks are seen as higher due to energy, but the assessment of recent data is dovish, with core inflation measures all seen near 2%, compared to 2.5% in January’s statement. Macklem stated that the risk that higher energy prices spread quickly to other goods looks contained and the BoC will look through the war’s immediate impact on prices. However he added that the longer the conflict lasts the bigger the risk, and the BoC will not let the impact broaden into persistent inflation.

The BoC stated that as the outlook evolves, they are ready to respond as needed. This suggests significant risk that the BoC could adjust rates lower should the war be resolved within a few weeks, though that would require further weakness in economic data, which we expect would see a modest improvement if uncertainty diminishes. Should the conflict persist the impact on Canada would be less negative than on most economies, though positive effects on Canada would be heavily concentrated in oil-rich Alberta while higher energy prices would weigh on consumers across Canada.

This suggests taking a more dovish view of the BoC outlook. We no longer expect a tightening in October, instead seeing 25bps moves in Q2 and Q3 of 2027 to take the rate to the midpoint of the BoC’s 2.25-3.25% neutral range. We now stand at the floor of that range, and renewed easing this year is not ruled out. Tightening in 2026 would probably require a persistent war and broadening inflationary pressures, as well as the Canadian economy avoiding a move into recession.