Sweden Riksbank Preview (Mar 19): On Hold and Still For Some Time Ahead?

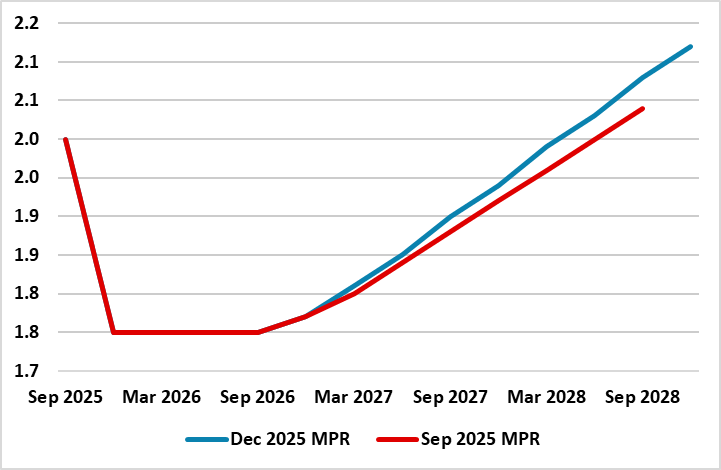

It is highly likely that the Riksbank will (again) keep policy on hold with the key rate left at 1.75% when it gives its next verdict. However, what will be more important is what the Board says; explicitly in terms of the recent (less pleasing to it) data flow and, implicitly in terms of updated forecasts in the Monetary Policy Report (MPR). The latter may try and assess the impact of Middle East conflict, but tentatively. But the GDP and CPI outlooks may need to be pruned back after what have been unexpected weak readings for both of late, some of which may be attributable to the recent appreciation of the Krona. The inflation undershoot is modest but as we have suggested repeatedly, the 2.6% Riksbank GDP projection for the year is overly optimistic, possibly by a factor of two. As a result, the Board promise of no change for some time to come is likely to be repeated but with more discernible risks attached in both directions. Regardless, we still do not see any looming policy reversal, as we see this current policy rate (1.75%) staying in place through 2027, ie a little longer than the Riksbank.

Figure 1: Riksbank Policy Outlook

Source; Riksbank Monetary Policy Report

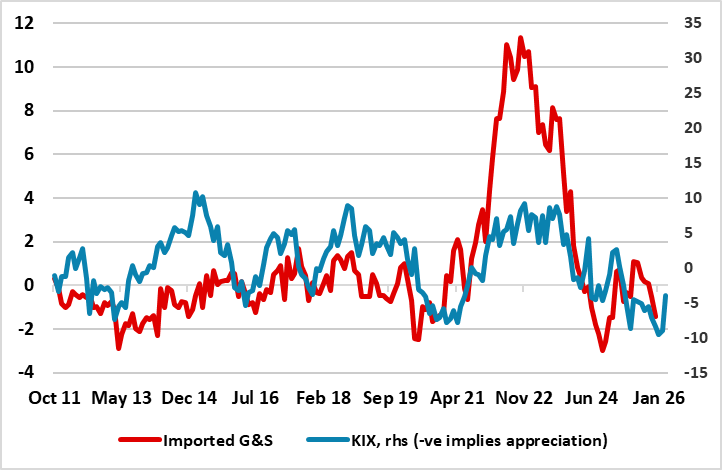

There is a saying that one should be careful about what you wish for. In this regard, the Riksbank aspiration of a strong(er) currency and low inflation is being more than met. The currency has risen strongly and is certainly a key factor in the current on-going disinflation, with imported consumer goods actually negative in y/y terms (Figure 1). Regardless, the underlying picture is still very soft as smoothed adjusted m/m figures (not as prone to volatility via base effects) show most measures of core inflation are consistent with the inflation target or below. Even so, the inflation undershoot (relative to Riksbank thinking rather than the 2% target) is modest, with CPI-ATE ex energy at 1.4% in February, 0.3 ppt below the December Board projections.

But the real economy backdrop is still puzzling and meriting more of a reassessment for the Board. Despite an apparent 2%-plus GDP jump in the last three quarters if 2005 (twice Riksbank thinking), the economy still looks soggy, not least in the labor market and perhaps increasingly so. Moreover, business surveys are mixed to soft while the Riksbank will note the results of its own survey, which underscores that Swedish companies describe the economic situation as a long and protracted slump that has not improved since the spring and where industrial activity has weakened. In addition, many respondents wonder whether households will continue to be cautious about consumption for a longer period.

Figure 2: Krona Accentuating Disinflation?

Source; Stats Sweden, % chg y/y - KIX is trade weighted Krona

It is against this background where we see a GDP growth outcome nearer 1.5% for this year, this also being similar to the forecasts we envisage for next year. This is well below the Riksbank’s thinking of 2.6% and 2.2% respectively for the coming two years, but where even these still suggest a negative output gap, at least until 2027. Not least to discourage the tightening speculation markets have started to factor in for H2 next year, we think the Board will be reluctant in coming months to make materially negative changes to its policy outlook; this currently envisages a tightening cycle beginning into early 2027 but even then little more than 25 bp hike though into 2028.