Norges Bank Preview (Jan 23): A Message to Markets?

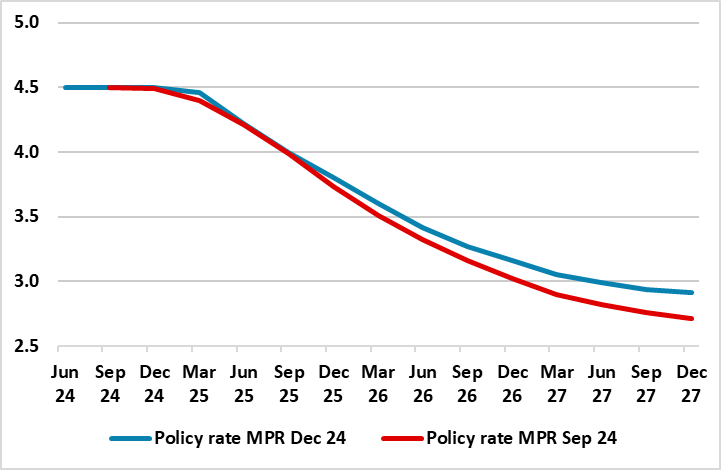

In its first meeting of the year, the Norges Bank is expected to keep rates on hold next Thursday. But it does have the choice of cutting rates, having flagged a move more likely at the meeting due in March, and could do this both to reflect weaker price pressures (especially excluding what are pro-cyclical rises in rents) and then signal to markets that the recent repricing of policy ahead and inter-related rise in bond yields is very much unjustified. But this would be inconsistent with the overly cautious Norges Bank Board which instead is fixated on the weaker currency despite the latter still seeing falling imported inflation. Thus, another (ie a ninth successive) widely expected stable policy decision so that the policy rate at 4.5% will then have been in place for over a year. But it is possible that the Board may be more vocal about the scale and timing of easing ahead being largely unchanged from the projections made last month (Figure 1), albeit having to resort to rhetoric as new forecasts will not be published until March.

Figure 1: Existing Policy Outlook to be Kept Intact?

Source: Norges Bank December Monetary Policy Report

The December meeting unchanged policy decision surprised no-one, and neither was the accompanying statement and forecasts, both more open about policy easing looming but only after two more meetings, so that the first cut will come in March rather than this month. The revised forecasts saw higher growth numbers but where the inflation outlook shaved back somewhat amid what was termed inflation pressures that appear to have been slightly more subdued than previously assumed. But the worry about business costs actually saw the policy outlook raised slightly (Figure 1), but with two-sided risks around it, encompassing the risk of an increase in international trade barriers but with less overt concern about the weak currency this time around. Higher tariffs will likely dampen global growth, but the implications for price prospects in Norway are uncertain. The Board is likely to underscore that this outlook remains intact despite market moves of the last month which have seen some 50-75 bp of anticipated rate cuts unwound. We still see rates falling faster and more sizably with some 150 bp of rate cuts in 2025 – 50 bp-plus more than the Norges Bank is advertising!

Nonetheless, and as Figure 1 also shows the Board anticipates that policy will continue easing all the way out to 2027, albeit basically settling at just under 3%. It is under if this is regarded as a neutral or terminal rate. How this policy outlook arises is unclear as targeted inflation (CPI-ATE) is seen staying above target through the forecast horizon, ie around 2.4% in 2027.

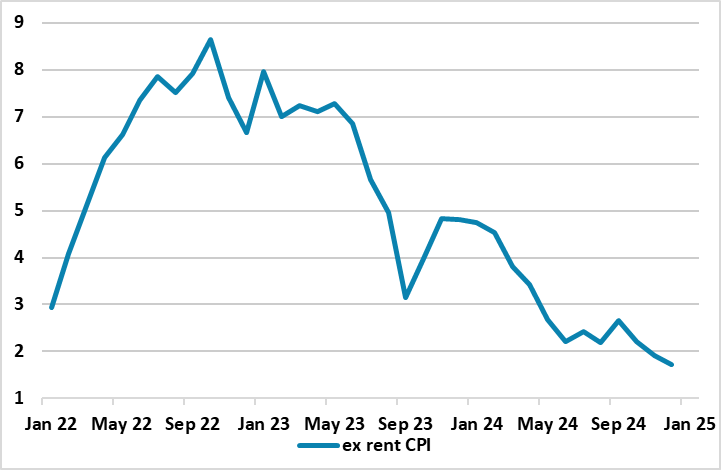

To us this is overly pessimistic. Admittedly, recent price dynamics have stated to suggest that disinflation may have started to fallen out. But this is only against a backdrop where monthly adjusted core readings are largely consistent with the 2% target already being met with m/m CPI-ATE and core outcomes of around 0.2%. And this is in spite of the impact of rental inflation (around 17% of the CPI) running still at well over 4% y/y, implying headline inflation ex-rents now at around 1.7%% (Figure 2). This begs the question whether Norges Bank policy is actually buttressing inflation as higher interest rates therefore mean higher inflation as rents are largely being driven by landlords facing (high) mortgage rates and increased demand for rental accommodation. Moreover, the resilience in rents may help explain the puzzling manner in which consumer confidence has developed of late, ie where households perceive a better financial position but are not willing to consider spending more.

Figure 2: Ex Rent Inflation Already Below Target

Source: Stats Norway, CE

The Norges Bank still sees policy risks being balanced, this view buttressed by a firmer than expected mainland real economy backdrop, the question being the extent to which the latter may as much reflect improved supply side developments related to productivity. But this did not feature (via a reassessment of the output gap) in the updated economic projections which still look too optimistic to us, not least given that they are based around a EZ picture for next year which sees 1.1% GDP growth almost twice what we envisage.