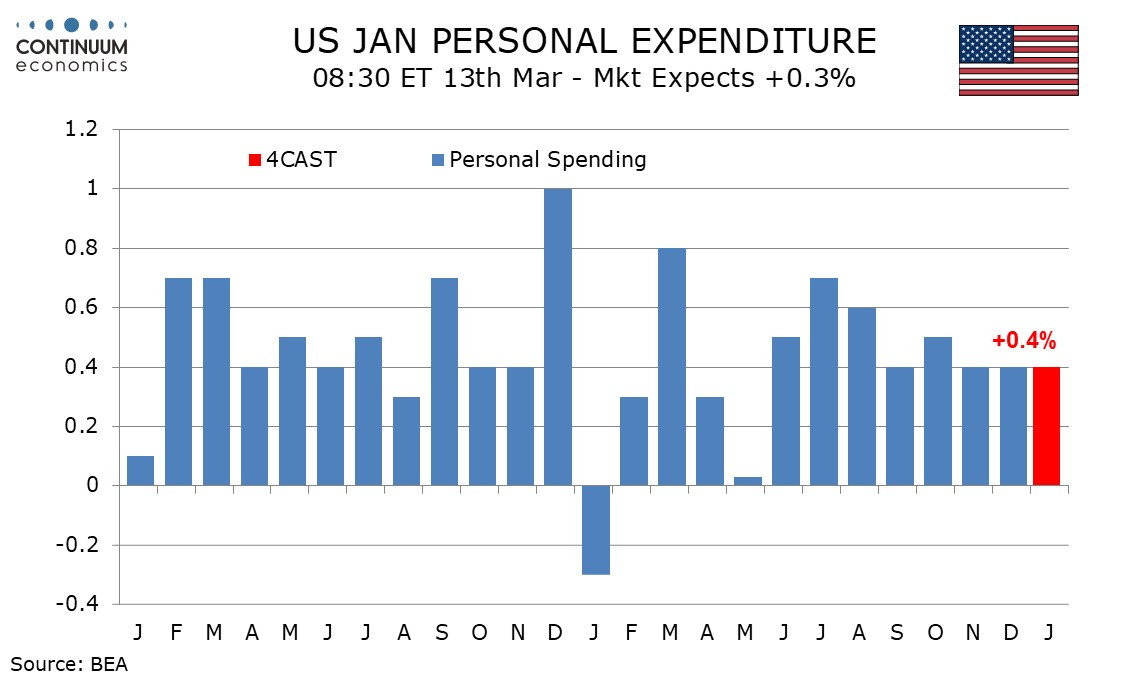

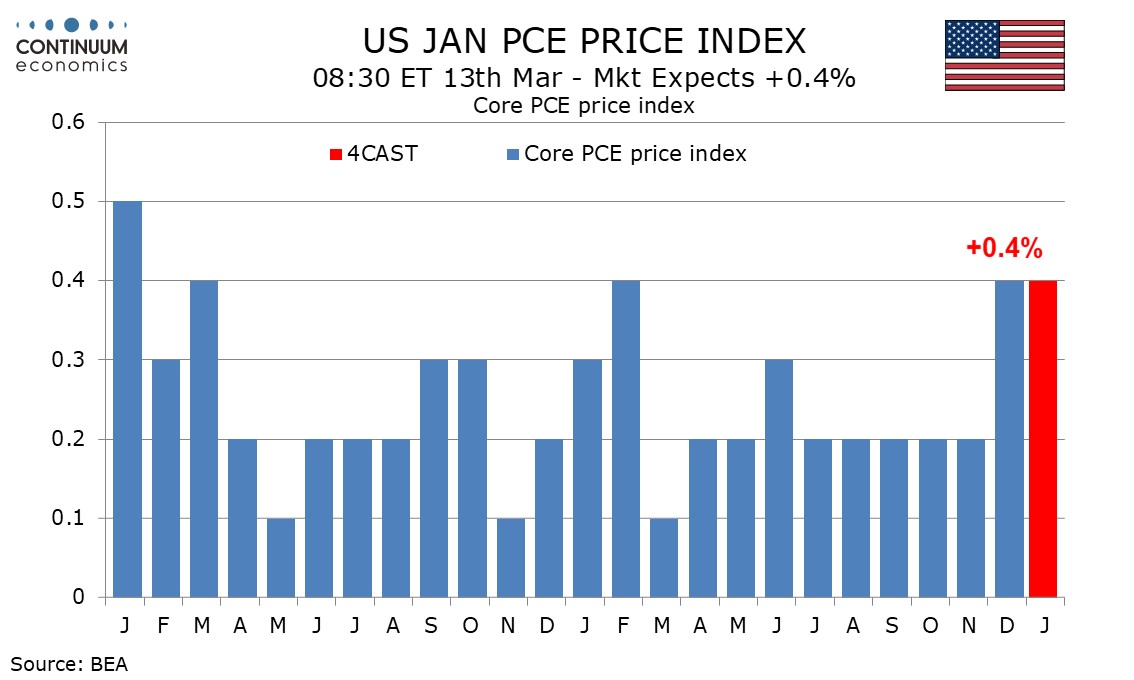

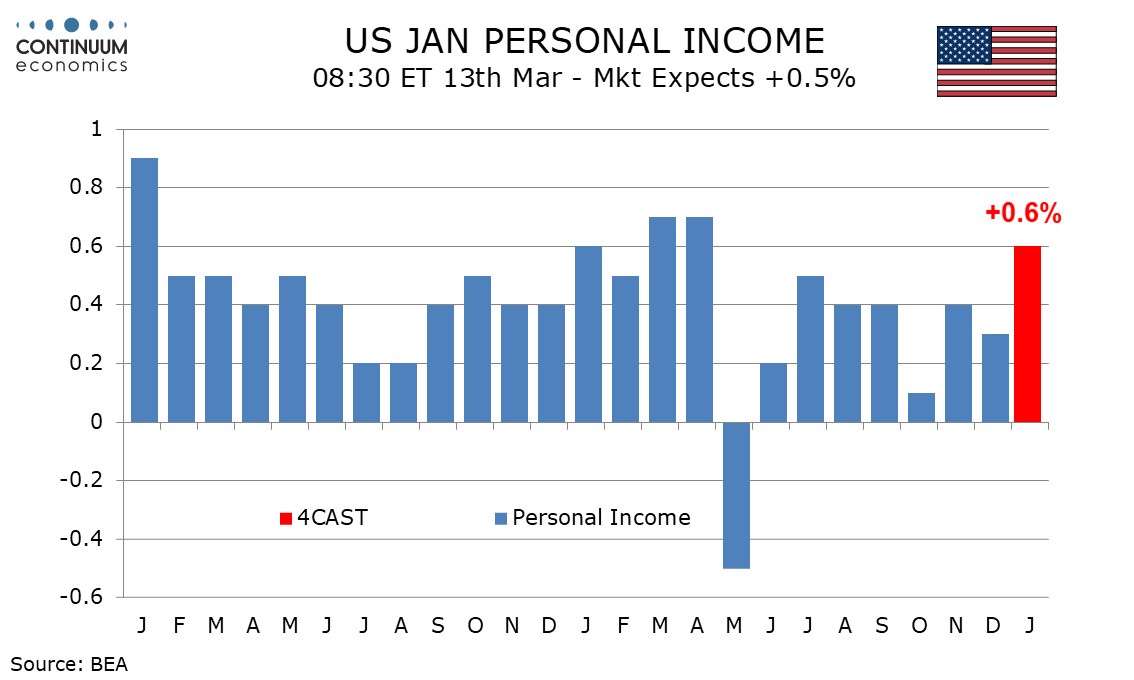

Preview: Due March 13 - U.S. January Personal Income and Spending - Core PCE Prices to outperform CPI

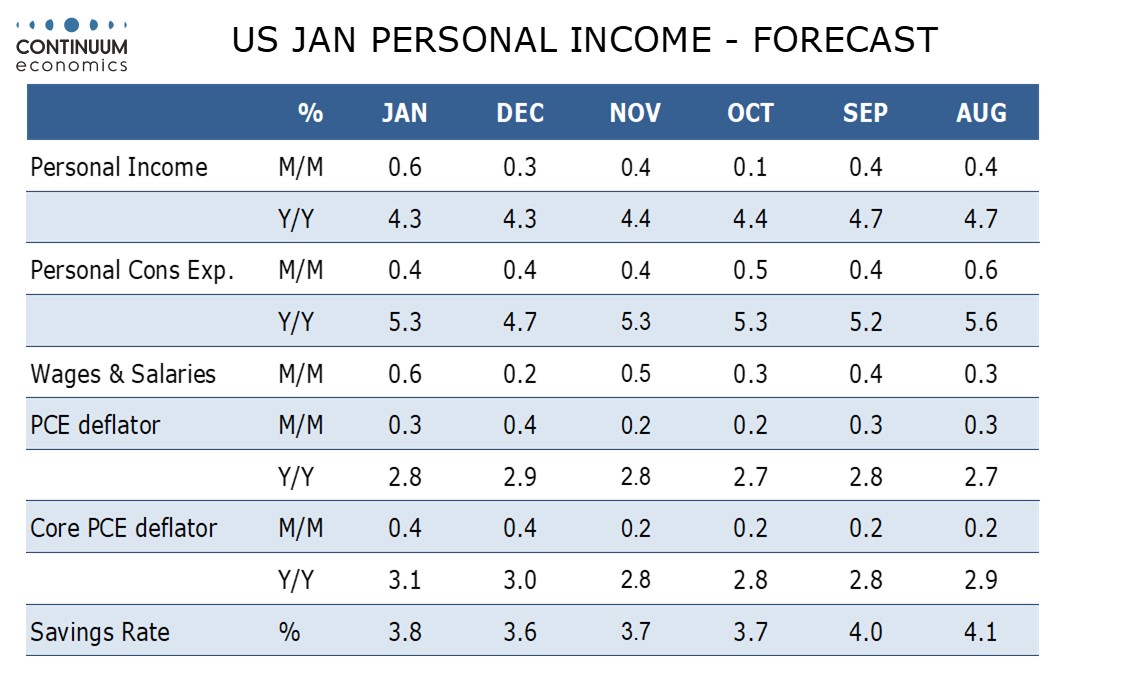

We expect January to see a strong core PCE price index increase of 0.4%, matching the rise seen in December. We expect personal income to increase by 0.6%, unusually outpacing personal spending, which we expect to rise by 0.4% for a third straight month.

CPI increased by 0.2% in January with a 0.3% increase ex food and energy. However given that the PCE price components of the PPI were strong in January, we expect the PCE price index to outperform the CPI, rising by 0.3% overall, and 0.4% ex food and energy.

This would see the yr/yr pace for overall PCE prices slip to 2.8% from 2.9% though the core rate would increase to 3.1% from 3.0%, reaching its highest pace since March 2024.

A healthy January non-farm payroll (though February’s was weaker) suggests a 0.6% increase in wages and salaries. The other components of personal income are also likely to be firm as Social Security benefits get a lift from the annual cost of living adjustment.

Retail sales slipped by 0.2% in January but we expect services to lift overall consumer spending to a 0.4% increase, though most of the increase in services spending will come from price gains. Spending outperformed income in Q3 and Q4 and is vulnerable to some slowing.