Preview: Due April 30 - U.S. March Personal Income and Spending - Core PCE Prices to outperform core CPI

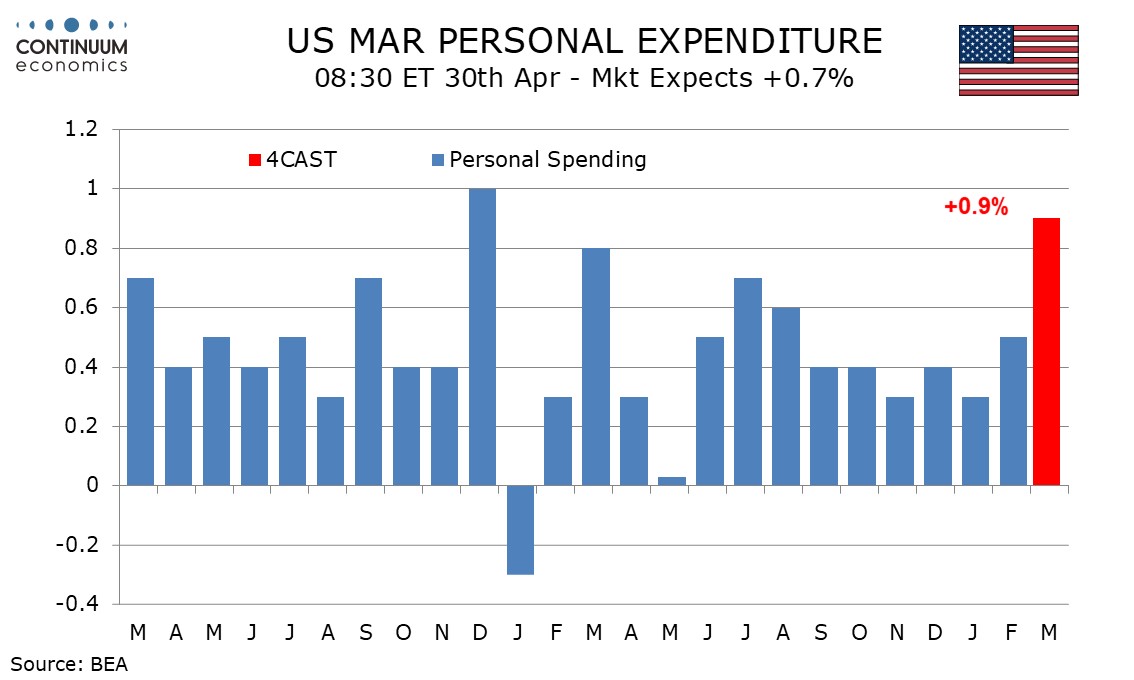

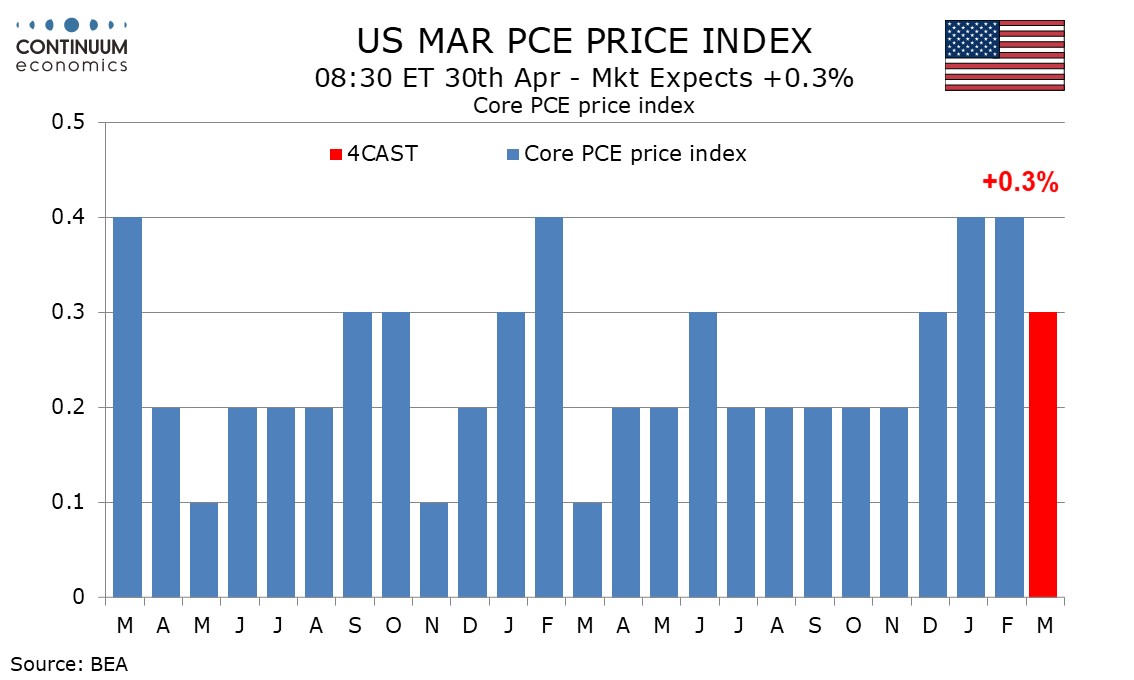

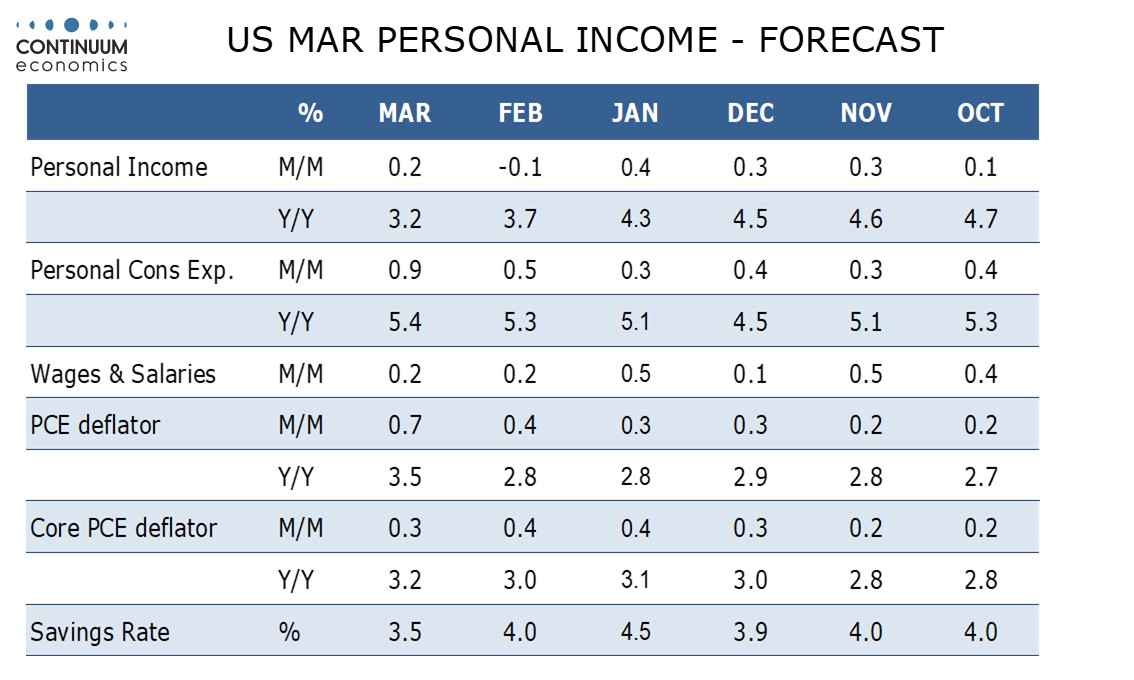

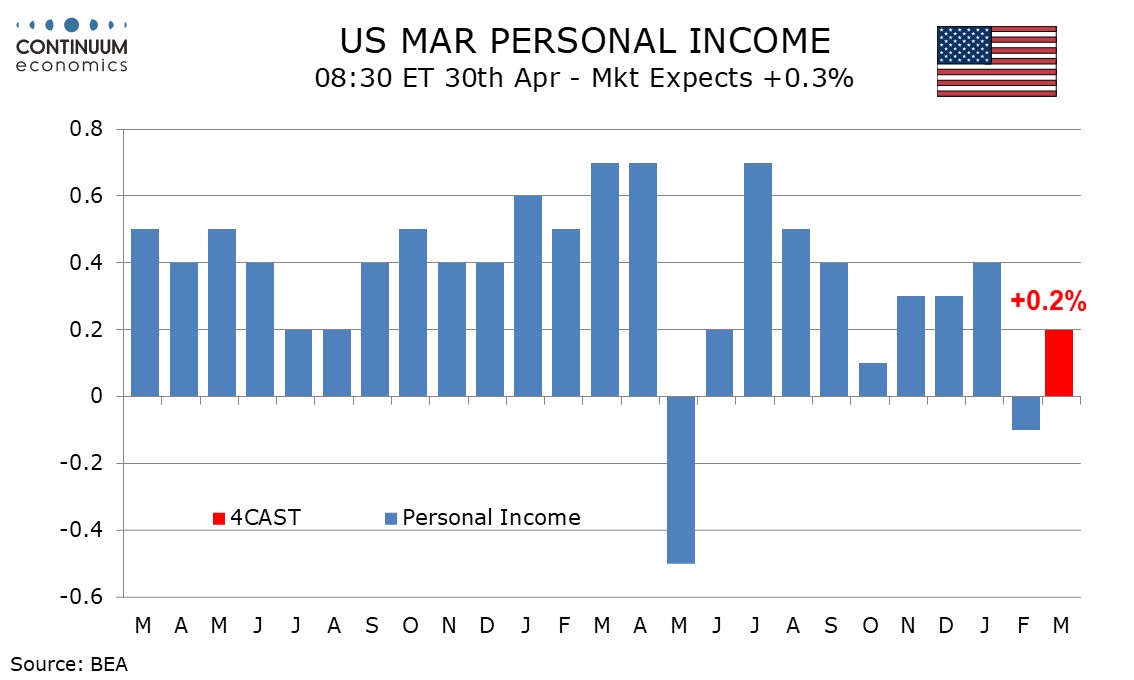

March’s personal income and spending data may be overshadowed by the Q1 GDP report due at the same time and to which it will contribute. We expect a 0.9% rise in personal spending, to exceed both a 0.2% rise in personal income and a 0.7% rise in PCE prices. For core PCE prices, we expect an increase of 0.3%.

CPI increased by 0.9% in March with core CPI up a moderate 0.2%. A 0.7% rise in PCE prices would be consistent with the fact CPI is more sensitive to gasoline prices than PCE prices. We expect core PCE prices to rise by 0.3%, exceeding the core CPI. While March’s core PPI was subdued, its components that contribute to core PCE prices were firm.

This would see yr/yr growth in overall PCE prices rising to 3.5% from 2.8%, reaching their highest since May 2024, while core PCE prices rise to 3.2% yr/yr from 3.0%, this the highest since January 2024.

While March saw a healthy non-farm payroll increase, subdued average hourly earnings and a dip in the workweek suggest a modest 0.2% rise in wages and salaries. We expect the other components of personal income to match wages and salaries, correcting from a February dip caused by reduced health care benefits. We expect disposable income to rise by 0.3% in March, supported by lower taxes, but this would still be a 0.4% decline in real terms.

We expect personal spending to rise by 0.9%, or 0.2% in real terms. Retail sales rose by 1.7%, led by surging gasoline prices, but with a solid 0.6% rise ex auto and gasoline. We expect a 0.4% rise in services, slightly stronger than February’s 0.3% but slower than in December and January. This would see the savings ratio dip to 3.5% from 4.0%, reaching its lowest level since October 2022.