German Data Review: Services Dip Further Despite Calendar Effects?

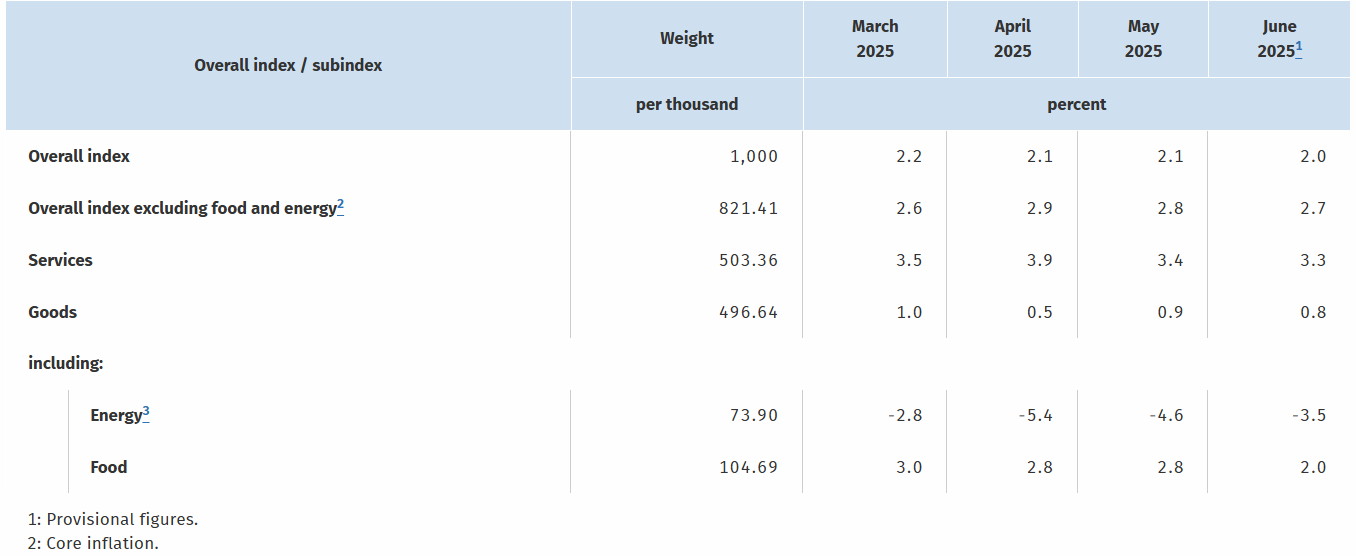

Germany’s disinflation process continues, with the lower-than-expected June preliminary numbers refreshing and reinforcing this pattern, with a 0. Ppt drop to 2.0%, a 10-mth low (Figure 1)! Previously but there have been signs that the downtrend was flattening out and this impression may have been accentuated by the small and lower than expected (ie 0.1 ppt) drop in the headline in May to 2.1%, still an eight-month low). Admittedly, adjusted data also and perhaps still suggest disinflation may have stalled (Figure 2). Regardless what we note is the surprise and marked fall in food price inflation alongside a small further drop in services inflation, this despite the likely upward pressure exerted (temporarily) by a further calendar-induced base effect that both offset an adverse energy base effect]. Thus the June HICP we see, comes with ‘only’ a 0.1 ppt drop in the core to 2.6%, although these preliminary data do not provide a breakdown to reveal the latter.

Figure 1: CPI Inflation Back to Target?

Source: German Federal Stats Office, % chg y/y

As for the EZ HICP due Jul 1), we still see the flash staying at May’s below-consensus, eight-month low and below-target 1.9%. However, similar adverse energy basis effects and a further calendar distortion could pull services and core back up in June (again temporarily), this factor too explaining what looks like fresh price pressures in seasonally adjusted short-term m/m movements.

Back to matter German, Most notable amid a drop caused by lower m/m fuel prices but with adverse energy base effects in y/y terms, was the drop back in May HICP services inflation which fell by a sizeable 0.7 ppt to 3.8% (or 3.4% on the CPI basis in Figure 1). As was the case in 2019, this rise in April and correction back last month was probably caused by the timing of Easter. There was probably a further holiday effect in the June numbers which may have restrained the further fall in services inflation, albeit one that will unwind in July. We see lower food inflation, but this may also be an upside risk.

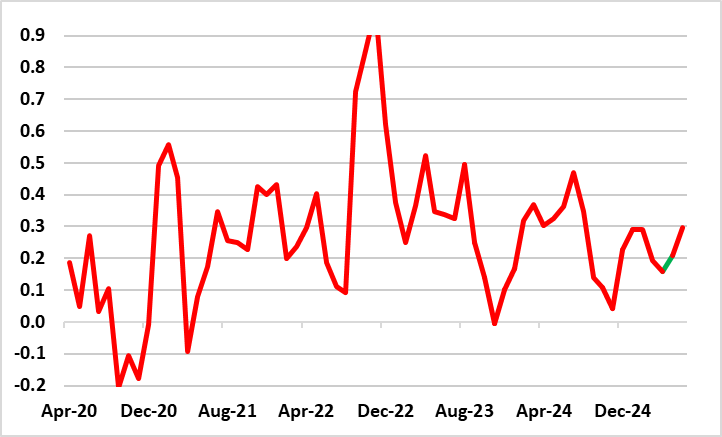

The German June data were bolstered by energy prices – mainly due to fuel prices having dipped more last year than this year – and this was again the case in this time around. Moreover, perhaps clear disinflation news may be evident in adjusted m/m data which have shown some fresh downtick in core rates, although this may not proceed further in the flash June numbers (Figure 2). In fact, adjusted data also suggest disinflation may have stalled (Figure 2), although this may be more a result of recent calendar aberrations than anything underlying.

Figure 2: Adjusted Core Rate Flattening Out?

Source: German Federal Stats Office, CE, % chg m/m adjusted and smoothed

Looking ahead, we had been seeing price gains trending further down and the German headline reading dipping below the 2% mark into the summer amid lower contributions from services and energy, the latter mainly fuel prices. But as suggested above, even though oil price gave backed (and are largely in line with ECB thinking in euro terms), the oil price question may accentuate existing divisions with the ECB Council, something that may be evident in the array of appearances at the ECB Forum on Central Banking this Mon-Wed!