CBR Will Likely Cut the Rate to 14.5% on April 24 Despite Risks

Bottom Line: Following the Central Bank of Russia’s (CBR) 50 bps cut on March 20—driven by the disinflationary trend in Q1—we expect the CBR to continue its easing cycle on April 24 reducing the rate from 15.0% to 14.5% despite inflationary risks. Our year-end key rate forecast is 13% for 2026 as Russia will likely maintain high real yields to support the economy.

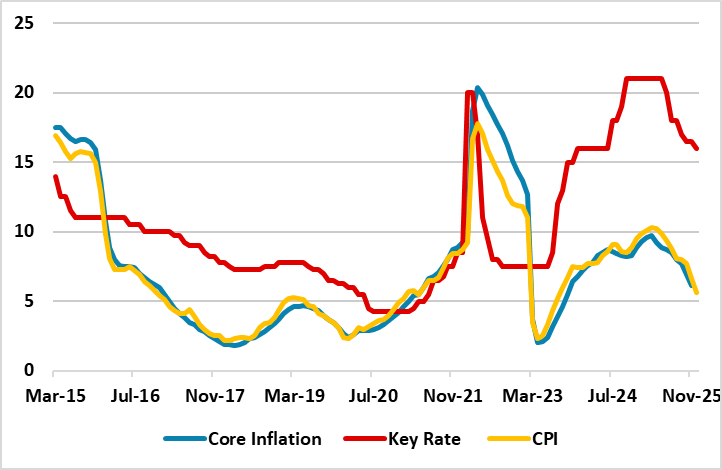

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – March 2026

Source: Continuum Economics

After the Central Bank of Russia (CBR) lowered the key rate to 15% on March 20—driven by accelerating disinflation—we anticipate a further cut to 14.5% on April 24 as inflationary pressures continue to ease. In March, inflation slowed to 5.9%, reflecting the lagged effects of previous tightening, a resilient Ruble, and moderate core inflation.

According to the CBR’s forecast, annual inflation is now projected to decline to 4.5–5.5% in 2026, with a goal of returning to its 4% target in 2027. However, we believe achieving this target band in 2026 will be challenging since the disinflationary process will take longer than the CBR anticipates due to the persistent impact of sanctions, the adverse effects of the Iran war, and sustained military spending will likely prolong disinflation, requiring monetary policy to remain restrictive for the foreseeable future.

We think higher global oil prices in Q2/Q3 and temporary sanctions relief due to the Iran conflict could boost Russia crude exports help relieve fiscal pressures, and stimulate growth. (Note: Higher oil revenues may facilitate expanded military spending, potentially triggering demand-pull inflation. Conversely, they could moderately decelerate inflation via the FX channel, although the impact of sanctions would likely limit this effect. We expect the net result to be a secondary rather than a dominant factor).

We maintain our 2026 average headline inflation forecast at 5.9%. In our view, a peace deal in Ukraine remains the primary catalyst required to ease inflationary pressures and resolve Russia’s persistent supply-demand imbalances. Consequently, we are holding our year-end key rate forecast at 13% for 2026, as the necessity for higher real yields will require the CBR to maintain a restrictive monetary stance.