FX Daily Strategy: N America, May 7th

ECB speakers may be mildly EUR supportive

NOK rallies as Norges bank hike

GBP vulnerable on local elections

Risk of reversal of recent risk positive trading if US/Iran deal is not completed

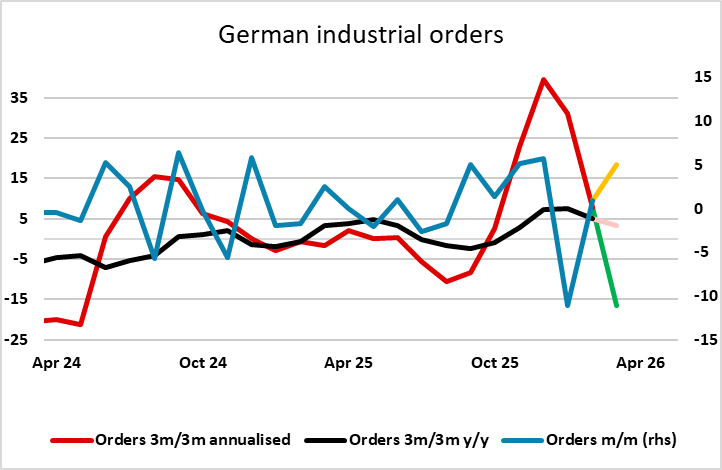

Thursday sees mostly second tier data, with the usual US jobless claims numbers, German factory orders and UK construction PMI. There is also a Norges Bank monetary policy meeting, and speeches from several ECB council members, notably chief economist Lane, as well as Elderson and Schnabel. We also have local elections in the UK.

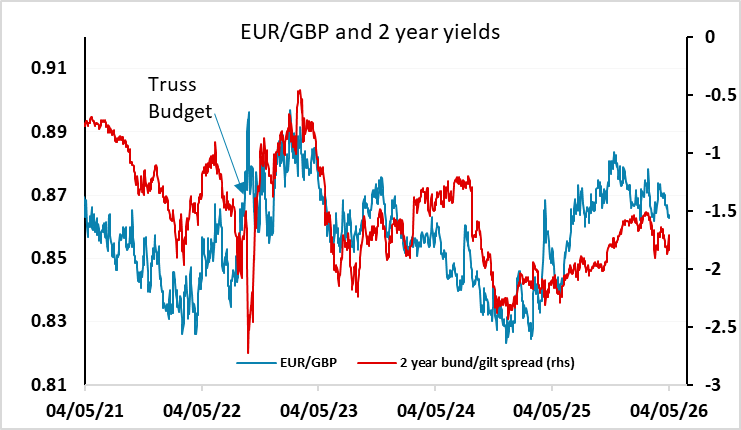

While it’s still quite a long time until the next ECB meeting on June 11, the noises from the ECB have been suggesting a willingness to hike, and the market is pricing in a hike as around a 70% chance. But given the volatility in the Middle East situation and the oil price, it’s hard to see how the market can price in a lot more than this more than a month away from the meeting. Nevertheless, we would expect the tone to be on the hawkish side and favour EUR gains, albeit modest. We would continue to favour gains against GBP more than other currencies, as EUR/GBP remains close to the bottom of its range for the year, and we would expect a more hawkish tone from the ECB than the BoE. The UK local elections are also likely to deliver substantial losses for the governing Labour party, and trigger renewed calls for a change of leadership. This still looks unlikely to happen anytime soon, but political uncertainty could add to downward pressure on the pound.

The NOK has rallied as Norges Bank hikes the policy rate to 4.25% from 4.0%. The move was around 60% priced in ahead of the decision, but the majority of forecasters were looking for no change. So far the FX response has been quite modest, with EUR/NOK dropping 7 figures to 10.87, but still only losing half of the gains seen yesterday on the back of the oil price decline. The Norges Bank statement referenced the statement in March, which indicated that inflation was too high and rate hikes would be necessary, saying the situation had not materially changed since then.

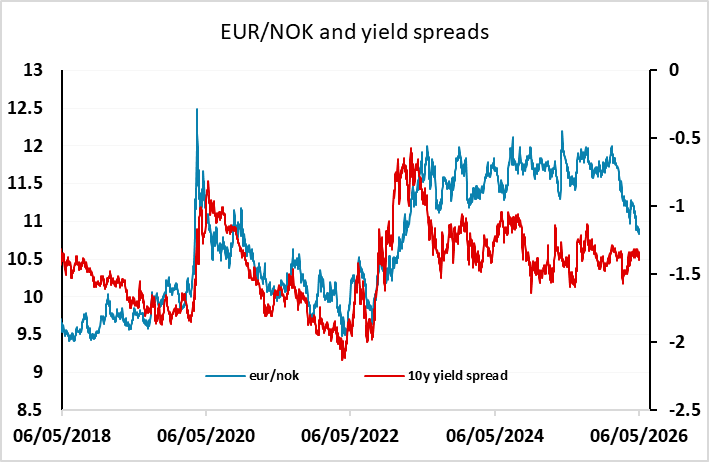

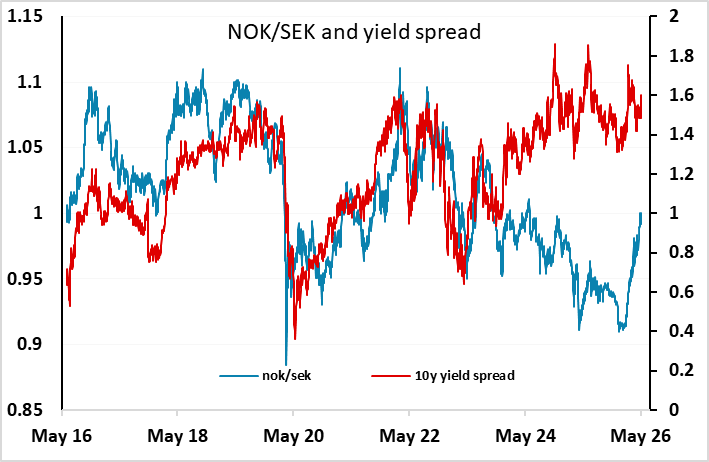

The NOK still looks good value from a long term perspective, even if the oil price continues to fall. Yield spreads are attractive, particularly against other European currencies, notably the CHF, SEK and EUR, and the underperformance in recent years means there is plenty of scope for further recovery.

Of course, the fate of the NOK and most other currencies will depend as much on any news on the US/Iran talks as any monetary policy decisions. The last two days of strong risk sentiment on the back of optimism over a deal make the market look a little vulnerable to a sentiment shift. If that does occur, the JPY may benefit on the crosses, with apparent BoJ intervention on Wednesday underlining the lack of JPY downside from current levels. Riskier currencies like the AUD and GBP may have the most downside against the JPY if we do see any turn in sentiment.

Datawise, German orders have been volatile in the last few months, so we doubt the market can glean much from this month's sharp rise. while the US jobless claims data has continued to suggest a solid labour market, and it would take more than one poor number to affect that view, especially in a US employment report week, so the data seems unlikely to have much effect.