SNB Preview (Mar 20): A Final Cut?

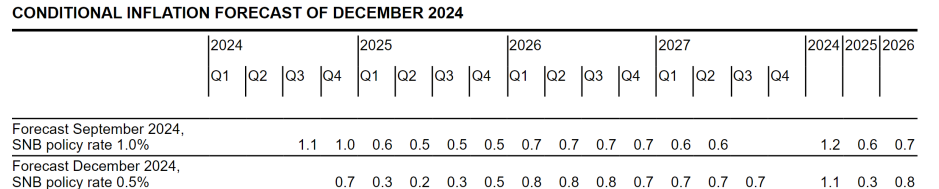

Having very much delivered relatively rapid easing worth some 125 bp in the last year, we see a further SNB rate cut of 25 bp at this month’s quarterly assessment taking the policy rate to 0.25%, the lowest since Sep 2022, ie when the Board moved away from negative rates. A return to negative rates is a risk that the SNB has itself noted but we think that policy will instead be put on hold after the envisaged further cut this month. Admittedly, arguments for more policy aggression can be linked to CPI inflation being so low. But it is still not inconsistent with the ‘below 2%’ SNB target and in any case is now running broadly in line with the projections made three months ago (Figure 1). In addition, the real economy is showing solid signs while there are clear hints of a real estate recovery. Instead, the SNB may wish to preserve conventional policy ammunition but still suggest that ‘will adjust its monetary policy if necessary’.

Figure 1: CPI Inflation Low But Not Undershooting SNB Thinking

Source: SNB

In what seemed then and now to be ever-clearer policy front-loading, the SNB cut its policy rate by 50 bp (to 0.5%) in December, thereby accentuating an easing cycle that had delivered three 25 bp moves in the previous nine months. Possibly, that larger, but far from unexpected, reduction was driven by a fresh assessment that the inflation undershoots (both actual and that projected out to 2027) were increasingly a reflection of weaker underlying price pressures rather than currency induced disinflation. But notably, and despite the marked anticipated inflation undershoot (Figure 1), the SNB was then less explicit bout further cuts, save to repeat its long-standing mantra that it ‘will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term’.

That was a clear shift in its rhetoric and policy guidance. Indeed, back in September, the SNB was then explicit in suggesting that ‘Further cuts in the SNB policy rate may become necessary in the coming quarters’, rhetoric then repeated (end Oct) by SNB President Schlegel.

Perhaps somewhat excessively, much of this inflation weakness has hitherto been attributed (at least by the SNB) to the strong Swiss Franc, but where we have suggested weaker global and domestic demand has been also playing a part. This now seems to be something the SNB is accepting, noting that in regard to weaker price pressures ‘both goods and services contributed to this decline’ as opposed to imported weakness discussed previously.

But the outlook likely to be painted by the SNB this time around may very much highlight continued low if not disinflation. It may highlight only a moderate pace of global growth while uncertainty about the economic outlook may have increased in recent months, not least regarding economic policy in the US and amid possible major shifts in thinking elsewhere in Europe. Even so, the SNB may continue to anticipate below-trend Swiss growth of between 1% and 1.5% for 2025.

New President Martin Schlegel (previous Vice Chair) took over the SNB helm for the last meeting and he may highlight this time around other considerations; there are better signs in terms of property prices, this possibly explain the December omission of the then-familiar warning about vulnerabilities in the mortgage and real estate markets. He may again refuse to rule out a return to negative policy rates and still make clear that the Swiss franc is still an important factor but may be less significantly so.