FX Daily Strategy: Asia, February 27th

Will Tokyo CPI Dip Further

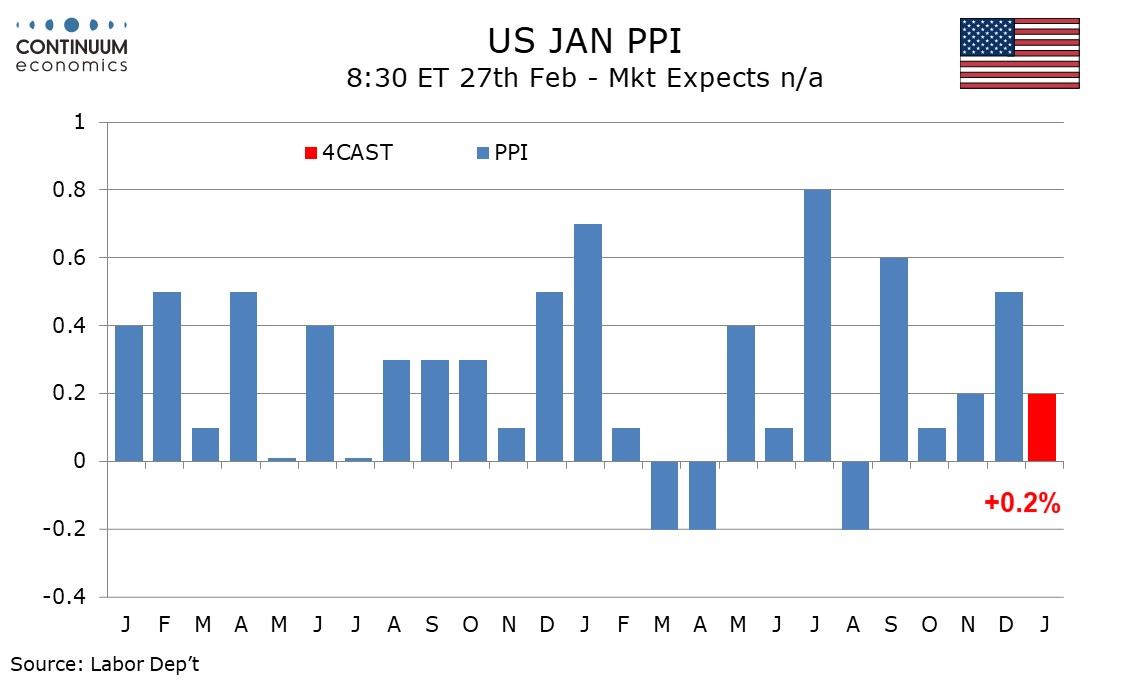

U.S. January PPI Slower than a strong December

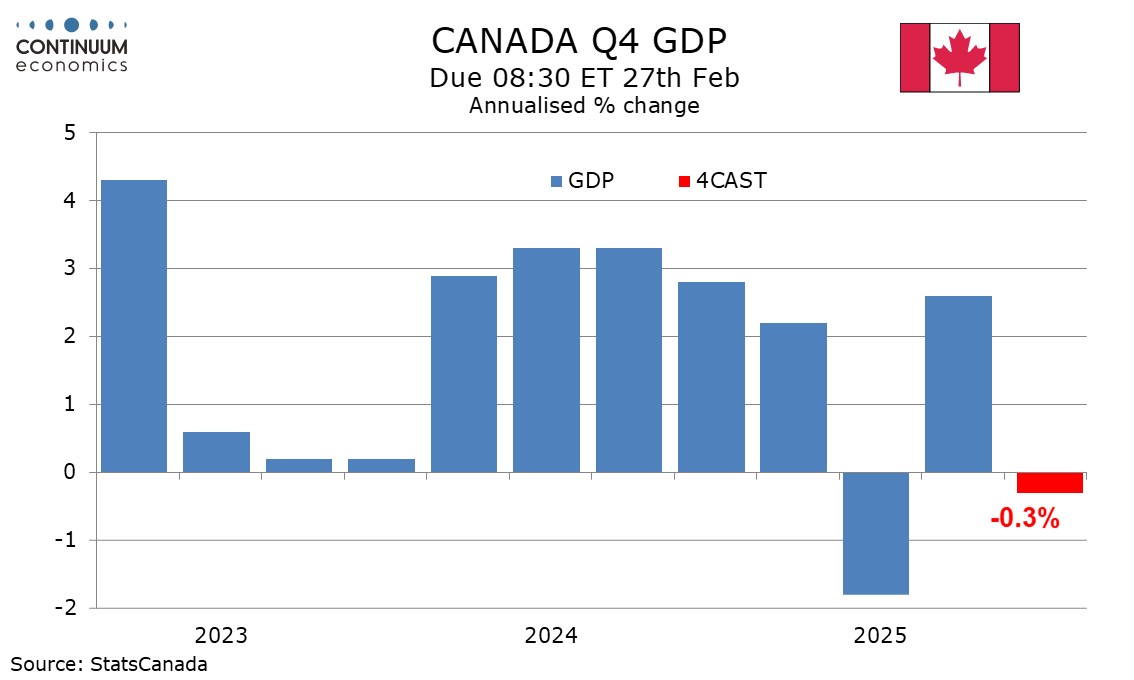

Canada Q4 GDP A modest correction

The February Tokyo CPI will be closely watched, especially when the January low read in National CPI, to see whether the inflationary pressure is easing sustainably. We believe any low read is more of base effect and latest round of energy rebates, rather than the easing of underlying inflationary pressure. However, if we do not see a steady wage growth or early signs of spring wage negotiation wanes, it may begin to sway market sentiment.

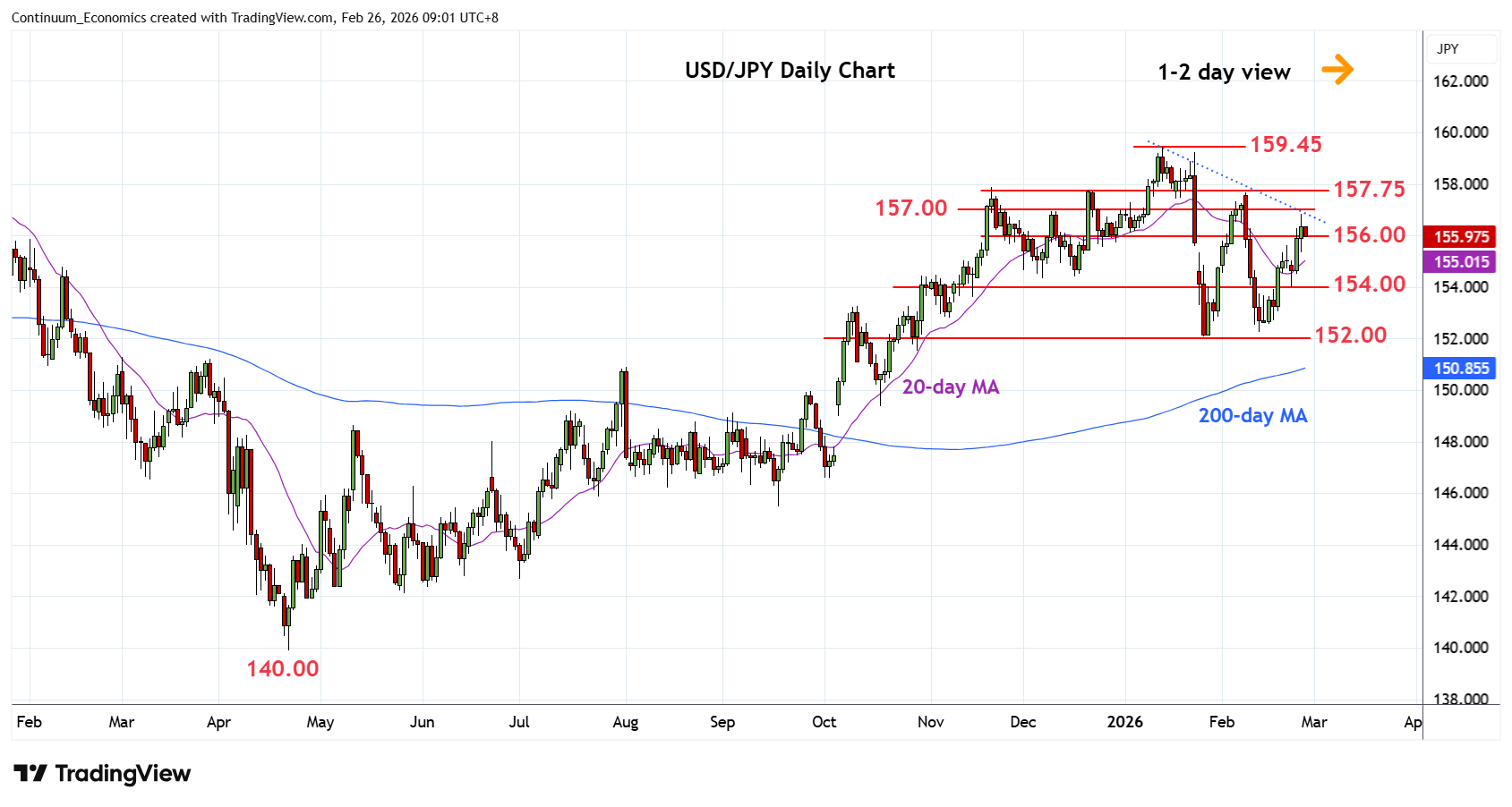

On the chart, the pair is extending bounce from the 152.27 low as prices retrace sharp losses from the 157.66 high of last week. Gains are seen corrective with resistance at the 155.50/156.00 congestion area expected to cap. Break here, if seen, will open up room for extension to 157.00 level and strong resistance at the 157.75/90 area. Corrective bounce expected to give way to fresh selling pressure later with support raised to the 154.00/153.00 congestion. Break here will return focus to the downside for retest of the 152.27 and 152.10 lows.

We expect PPI to rise by a slower 0.2% in January both overall and ex food and energy, after strong respective gains of 0.5% and 0.7% in December. The slowing will be largely in trade, though ex food, energy and trade we expect a rise of 0.3%, slightly slower than December’s 0.4%. We expect gains of 0.3% in food and 0.5% in energy after both declined in December, but these gains will not be quite enough to lift the headline above the 0.2% ex food and energy rate.

We expect goods PPI ex food and energy to rise by 0.3% after a 0.4% increase in December. Trend has been accelerating modestly, with the last six months having seen four gains of 0.4% or above and two at 0.2%, while the first six months of 2025 saw four gains of 0.3% and two of 0.2%, while trend in 2024 was slightly below 0.2% per month. The acceleration is likely due to tariffs, and there may be more to come, though trend still appears to be fairly close to 0.3% per month. Services rose by 0.7% in December lifted by a 1.7% increase in trade which followed losses of 0.6% in November and 0.8% in October. Trade is volatile and is likely to slip back a little in January, restraining overall services PPI to a 0.2% increase, but underlying trend in services also seems to be running around 0.3% per month, signs of a slowing in mid-2025 having faded. This is a cause for concern with services less sensitive to tariffs, meaning early 2026 data should be watched closely.

We expect Q4 Canadian GDP to decline by 0.3% annualized, marginally softer than an unchanged estimate made by the Bank of Canada with January’s Monetary Policy report. This would be consistent with December GDP rising by 0.1% as projected with November’s data. The GDP decline would be a modest correction from a 2.6% Q3 increase that significantly exceeded expectations, though we expect Q4 to see a modest 0.4% increase in domestic demand after a 0.1% decline in Q3.

We expect household consumption to look similar to Q3 with a 0.4% decline but gross fixed capital formation to rise by 0.9%. While the latter would be a slowing from Q3 we expect Q4’s increase to come from the private sector, while Q3’s gain came mostly in government. We expect government investment to correct from the strong Q3 but government consumption to see a modest increase after a Q3 decline, though overall consumption will still be marginally negative.