FX Daily Strategy: N America, Oct 8

RBNZ Surprise with a 50bps Cut

JPY weakness remains extreme but lacks a fundamental basis

RBNZ Surprise with a 50bps Cut

JPY weakness remains extreme but lacks a fundamental basis

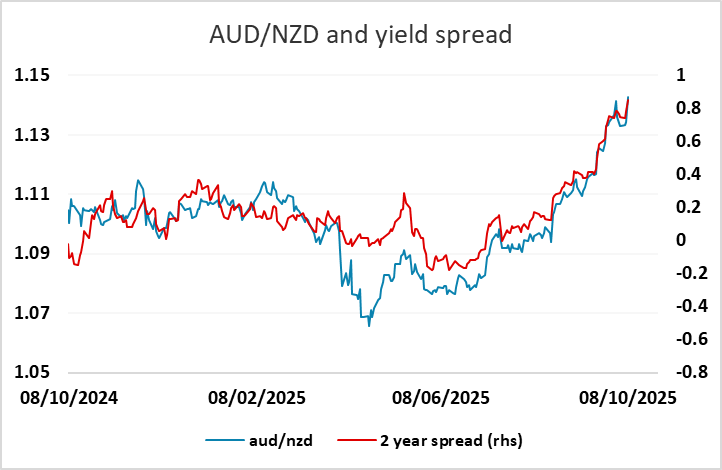

The RBNZ meeting looks like the main event for Wednesday. All forecasters expected a rate cut, but were split on the likely size, with 15 of 26 in the Reuters survey going for a 25bp cut and 11 looking for 50bps. Market pricing suggests it was close to a 50-50 call between 50 and 25. The actual 50 bp was therefore NZD negative. There was no official revision to the OCR forecast from August. But unlike the August cut, the 50bps cut in October is a consensus cut, which means all members agree that short term CPI may be volatile but the long time economic condition needs more accommodation. In the forward guidance, the RBNZ is consistent with their August forecast which points towards at least one more cut in the November meeting. AUD/NZD continues to follow the 2 year yield spread higher, but may pause below 1.15.

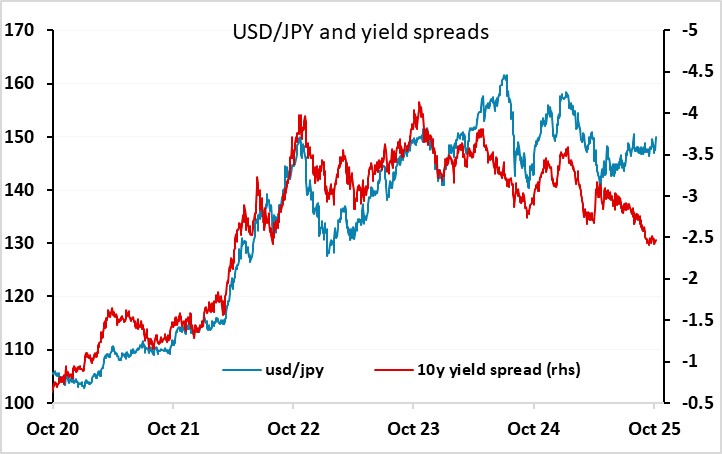

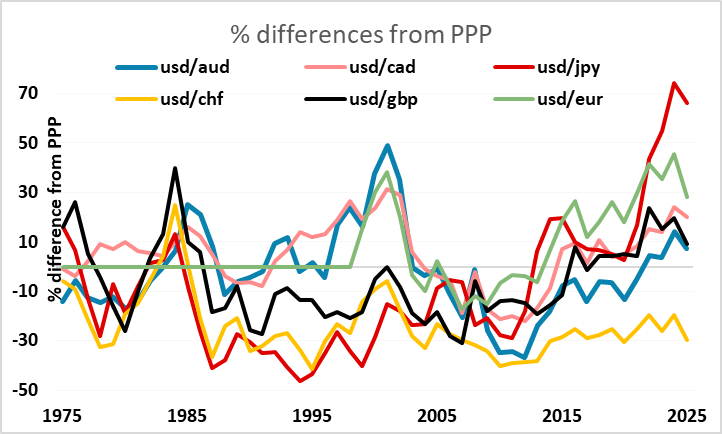

The JPY continued to be the biggest mover on Tuesday, with USD/JPY continuing the uptrend seen since the election of Takaichi as the new LDP leader and PM. The moves looked to be essentially technical, as there has been no policy announcement and no significant further moves in Japanese yields, with 10 year yields still close to 17 year highs and 2 year yields only around 5bps off the 17 year high seen last week. With USD/JPY starting from an already extremely undervalued level, both from a long term fundamental perspective and relative to the usual yield spread correlation, there is clearly no yield based justification for the JPY decline.

Nor is JPY weakness on the crosses consistent with the moves in equity risk premia that have been highly correlated with most JPY crosses in recent years. The JPY weakness consequently looks more sentiment driven than anything else. It is very doubtful that the new PM will seek an even weaker JPY, and we would also doubt that she will attempt to interfere with BoJ independence by looking for easier monetary policy. Indeed, easier fiscal policies that she is expected to follow are likely, in the end, to lead to higher Japanese yields, but may be seen to increase the risk premium applied to JGBs.

So JPY weakness looks mainly sentiment or technically driven. There retracement level at 151.62 in USD/JPY was an initial target for the JPY bears but broke easily overnight. It is possible that the Japanese MoF could be considering intervention in support of the JPY near current levels. While USD/JPY is short of the highs, the real effective JPY is now close to all time lows. While intervention is not normally effective if the move is fundamentally driven, in current circumstances it would likely be effective as a signal of government preference for a stronger currency, negating some of the current sentiment.