FX Daily Strategy: Asia, April 3rd

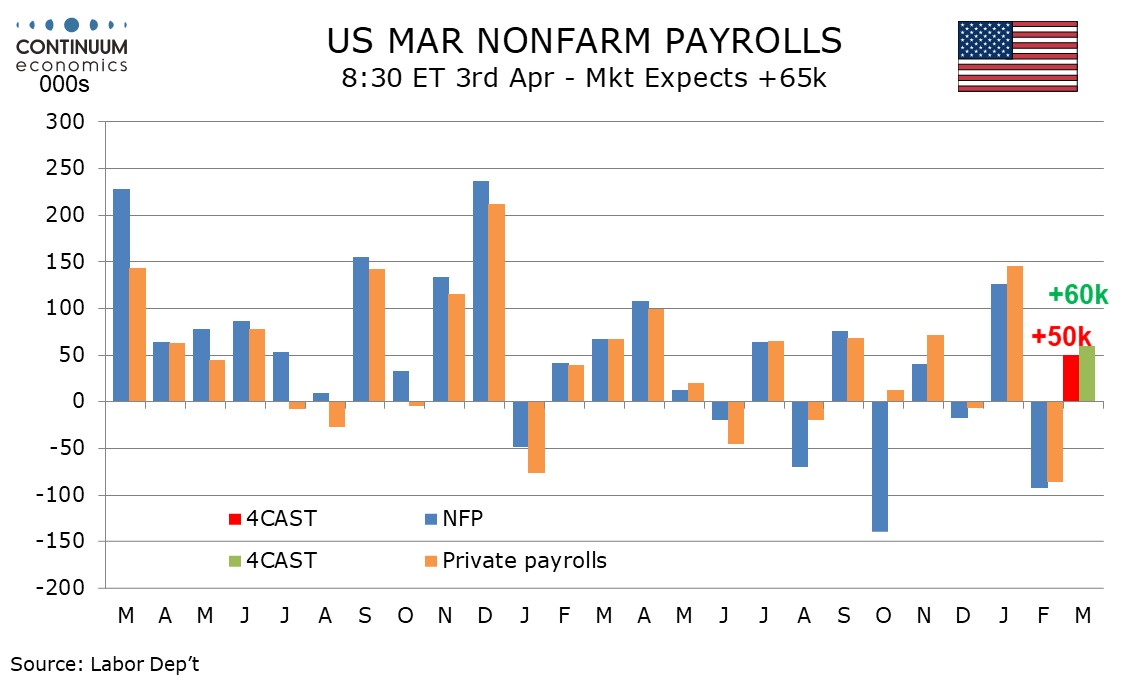

U.S. March Non-Farm Payrolls Forecast revised up on returning strikers

DXY Lower in profit-taking

We now expect March’s non-farm payroll to rise by 50k overall and by 60k in the private sector, both revised up by 30k due to the ending of strikes, largely in health, as shown in Friday’s strike report. This is still consistent with a subdued labor market picture, which a rise in unemployment to 4.5% from 4.4% and a slower 0.3% increase in average hourly earnings would also imply.

The average of January’s 126k increase and February’s 92k decline is 17k, while for the private sector a 146k January increase and a fall of 86k in February leaves an average of 30k. In December the three month private sector average was 32k and that for overall payrolls negative at -7k, depressed by particularly heavy public sector layoffs in October, as DOGE layoffs came through.

On the chart, consolidation beneath the 100.64 current year high of 31 March is giving way to a deeper pullback, as profit-taking pressure increases, with prices currently consolidating the test of congestion support at 99.50. Daily readings have turned down and overbought weekly stochastics are unwinding, highlighting room for a later break beneath here towards further congestion around 99.00. The positive weekly Tension Indicator and rising longer-term charts could limit any initial tests of here in fresh consolidation. Meanwhile, resistance is lowered to congestion around 100.00. A close above here would help to stabilise price action. But a further close above 100.64 is needed to turn sentiment positive and confirm continuation of late-January gains.