FX Daily Strategy: N America, October 11th

EUR/GBP little chnaged after UK GDP data

Weaker USD after higher CPI may reflect higher jobless claims, but these may be hurricane related

Little reason to see a sustained weakening in risk sentiment

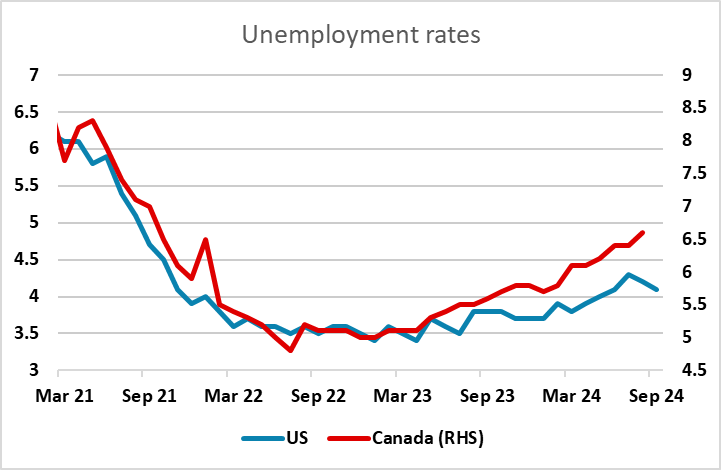

CAD vulnerable as unemployment rate rises

EUR/GBP little chnaged after UK GDP data

Weaker USD after higher CPI may reflect higher jobless claims, but these may be hurricane related

Little reason to see a sustained weakening in risk sentiment

CAD vulnerable as unemployment rate rises

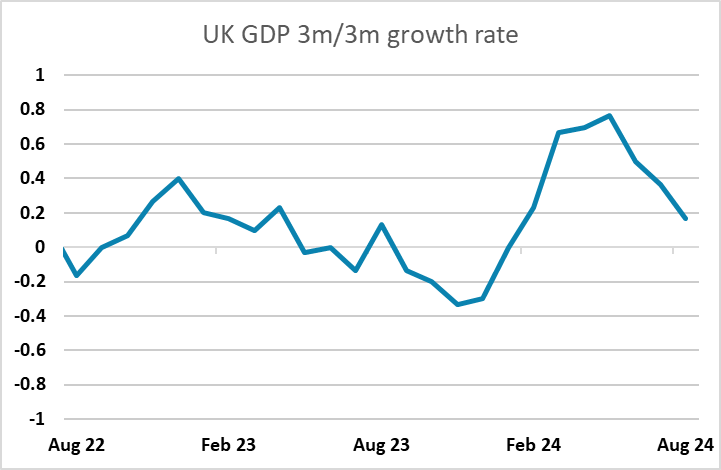

UK August GDP data has come in in line with expectations at 0.2% m/m, and there has been no significant impact on GBP. The August rise follows two flat months, and it does seem that the strength of H1, which saw growth pick up unexpectedly, is waning, with the 3m/3m growth rate running at 0.2%.

It is also notable that in spite of the sharp rise we have seen in then UK manufacturing PMI this year, manufacturing output remains weak in the official data. While there has been little impact on GBP from the numbers, the strength of then pound this year has been based to some extent on UK growth outperformance, and if this is waning the high level of GBP is hard to justify, especially if the BoE are about to start easing more aggressively, as the recent comments from governor Bailey suggest. EUR/GBP remain at levels that are close to the highs seen since the Brexit referendum in real terms, and as UK growth slows and rates are cut we would expect EUR/GBP to start to move up above 0.84.

The USD reaction to the US data on Thursday was a little surprising, with the USD falling, mainly against the JPY, despite the stronger than expected CPI data. It may be that the market was reacting to the much higher than expected jobless claims numbers, but there is a strong possibility that the claims data were affected by Hurricane Helene. Even so, with future data potentially impacted by Hurricane Milton, we could see some more weak data in coming weeks, and similar weakness may be seen in the October employment report when it comes out. Even if distorted, weaker employment data is seen as significant. From a yield spread perspective, there is much more potential for the USD to correct lower against the JPY than the EUR, with US yields at the short end still high enough to suggest EUR/USD can test below 1.09.

There was a generally more risk negative tone to the markets after the US data, with commodity currencies falling back and the CHF and JPY gaining ground. But equities were only slightly lower, and we don’t see a strong case for a significant move lower in sentiment at this stage. Markets still expect two more Fed cuts by year end, and only if inflation problems are seen as a barrier to Fed easing is there likely to be any real concern in the equity market.

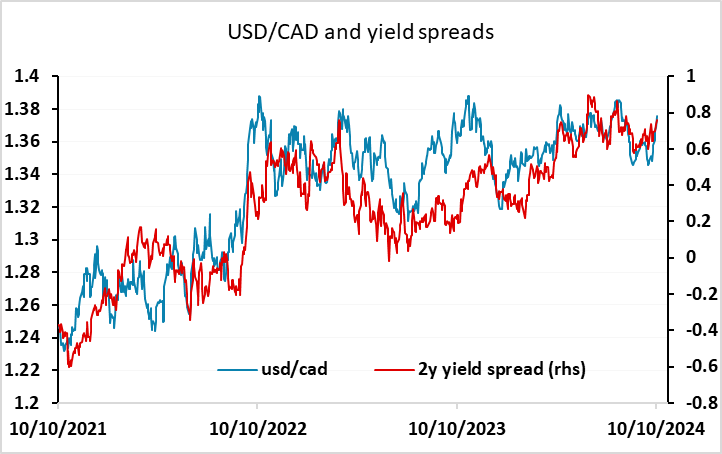

Friday also sees Canadian employment data. The market consensus anticipates another solid rise in employment in the region of 30k, but a rise in the unemployment rate to 6.7% from 6.6%. The recent trends in the US and Canadian unemployment are showing a significant difference, with the Canadian rate rising significantly faster, and numbers in line with consensus may well keep the CAD on the back foot. USD/CAD has been edging higher with spreads, and could well continue on that path.